Does Uber Make Masa a Savvy Investor or a Shopaholic?

(Bloomberg Opinion) -- Nothing cements a venture capital firm’s reputation like a good exit.

After a long dry spell, Masayoshi Son is finally catching a break: The listing of Uber Technologies Inc. made his Vision Fund one of the rare investors to book a capital gain from its stake, amounting to 418 billion yen ($3.81 billion) in the March quarter. While Uber shares have slumped since they started trading Friday, that’s a big win for the SoftBank Group Corp. founder, who likes to sell himself as a tech visionary.

That extra cash could come in handy. Last December, Moody’s Investors Service re-classified SoftBank as an investment holding company after Son pulled off the world’s second-largest IPO, raising $23.6 billion from his Japanese telecom operator. Yet international ratings firms still rank the company one notch below investment grade, dangling their stamp of approval right before Son’s eyes.

Make no mistake: Son covets a good rating. While his billion-dollar checks grab headlines, the inconvenient truth is that SoftBank is strapped for cash. His years-long acquisition spree has left the company with roughly $100 billion of net debt, which forced it to shell out $5.7 billion in interest expenses in the past year alone. In Asia’s dollar bond market more broadly, junk-rated issuers on average have to pay investors a yield of 7 percent, more than twice as much as their more creditworthy counterparts.

Lately, Son has been talking about raising money for his second Vision Fund. Endowments and pension funds have been more than happy to gain exposure to unicorns these days; but with regular bills to pay, both types of investors need to trust the Vision Fund won’t blow up one day. An investment-grade rating would speak volumes about Son as a prudent risk manager.

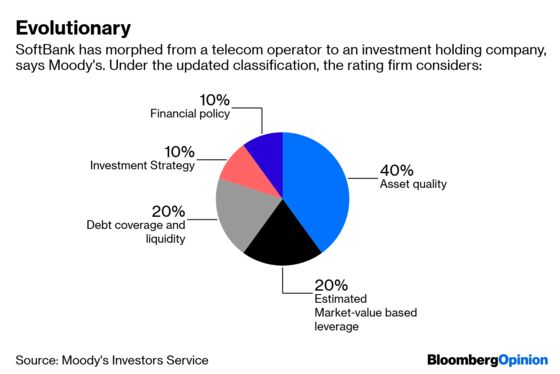

That’s why Moody’s re-classification, which I predicted, was a nice gift. As a telecom operator, SoftBank’s mountain of debt was subject to much deeper frowns: Debt and liquidity accounted for a 35% weighting in Moody’s credit considerations. As an investment-holding firm, leverage ratios matter less — getting just a 20% weighting.

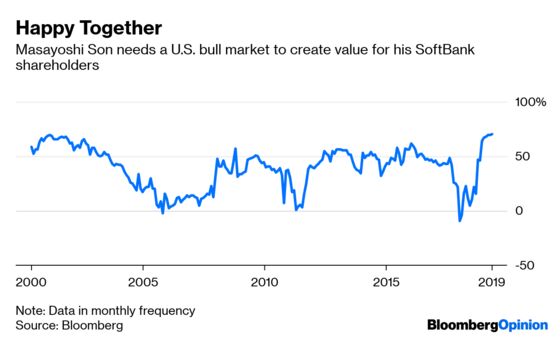

In the past year, the correlation between SoftBank’s Tokyo-listed shares and the Nasdaq Composite Index has soared to a dot-com era high. That seems to suggest investors share Moody’s assessment.

But now, the quality of Son’s investment portfolio is under scrutiny, and the biggest impediment to SoftBank earning an investment-grade rating is its lack of asset diversity. The company’s 29% stake in Alibaba Group Holding Ltd. accounted for about 40% of the market value of its portfolio, according to Moody’s. This high concentration exposes the portfolio value to price volatility.

Despite all the hype, the Vision Fund was valued at only $40 billion when Moody’s published its report in December — and we only have Son to blame. The fund had staged just one meaningful exit at that point — Flipkart Online Services Pvt’s sale to Walmart Inc.

The Vision Fund could have any number of valuable unicorns in its basket, but until Son provides an exit — through a sale to a strategic buyer, an IPO, or organizing a new fundraising round that yields higher valuations — a startup’s fair value has to be its acquisition cost. In other words, there haven’t been enough capital gains.

Crossing that hurdle won’t be easy. After Uber’s debut flop, Son needs time to take his rich horde of unicorns public.

To its credit, the Vision Fund has made a lot of progress since December. It added 19 companies to its portfolio in the March quarter, sending the fund’s fair value to $72.3 billion. Yet the fundamental problems remain. Even with updated figures, the Vision Fund accounts for less than 10 percent of SoftBank’s total investment value, based on my calculations.

To be deemed a proper venture capitalist, Masa Son needs successful IPOs to prove that his most valuable asset isn’t a fluke. Otherwise, he’ll be considered just another shopaholic.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.