(Bloomberg Opinion) -- Singaporeans aren’t spending like they used to, at least not in shopping malls. There are too many already and more are being built. But investors still have good reasons to back mall owners.

The city-state has 6.1 million square meters of retail space, of which 8.7 percent is vacant. Yet companies are forecast to add a further 364,000 square meters, with the biggest chunk hitting the market this year. This is when online shopping is catching on, retailers such as Crabtree and Evelyn are closing physical stores, and rents are scraping the bottom.

Two years ago, the median tenant was shelling out S$9.76 per square foot ($77 per square meter) in the main shopping district of Orchard Road, when the going rate for category 1 offices was S$8.65. Now, office rentals have zoomed to S$10.18 – 30 Singapore cents more than top-grade retail space – while prospects for a spending recovery aren’t great. CapitaLand Mall Trust, the island’s biggest shopping mall landlord, classifies its tenants in 17 categories, out of which 11 – including supermarkets and department stores – saw sales fall in the first quarter from a year earlier. Telecommunications, home furnishings and music and video led with big double-digit declines.

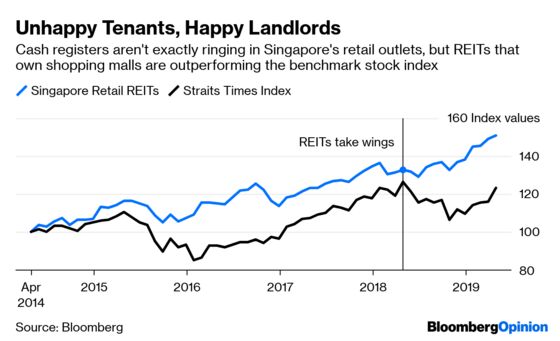

Paradoxically, real-estate investment trusts that own malls are outperforming the benchmark Straits Times Index. Interest rates may be a part of the story. With global rates expected to stay lower for longer, a 5 percent dividend yield on CapitaLand Mall’s shares implies a near 3 percentage point spread on 10-year Singapore government bond yields.

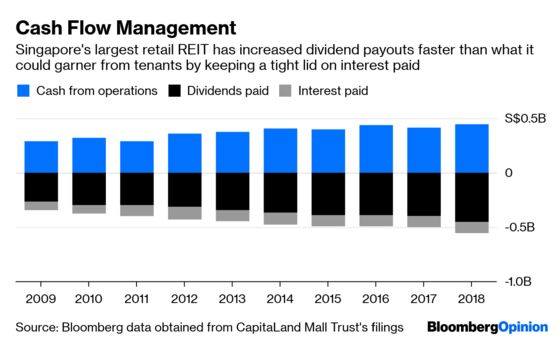

Singaporean savers got burned after being lured by the 6 percent perpetual bonds sold by water-purification company Hyflux Ltd. To them, the fact that REITs are cautious about their balance sheets is a big attraction. CapitaLand Mall sold a 2029 U.S. dollar bond last month, swapped the 3.609 percent coupon to an attractive 3.223 percent Singapore dollar 10-year liability, and used the S$407 million proceeds to reduce debt coming due between now and 2022. Of the S$2.3 billion increase in the trust’s assets in the past five years, S$1.4 billion has come as new capital from shareholders. Over the same period, Frasers Centrepoint Trust, the city’s third-biggest retail REIT landlord, has financed a S$700 million expansion of its assets with almost S$500 million of equity.

But then, Singapore is Asia’s REIT capital, which means there’s no dearth of well-managed investment vehicles. Almost every other kind of Singapore REIT – office, industrial, hospitality, residential, and healthcare – is forecast to offer a somewhat better dividend yield next year than retail, according to Maybank Kim Eng Research Pte.

Look beyond the short term, though, and there are sweeping changes coming to the city. DBS Bank Ltd. analysts are excited about Starhill Global REIT, which may be a key beneficiary when its marquee Orchard Road malls are allowed a 29 percent increase in their plot ratio, a measure of how much floor space landlords can squeeze out a parcel of land. The other idea in the Urban Redevelopment Authority’s new draft master plan is to encourage more of the older office buildings in the central business district to be converted into homes and hotels. Singapore’s CBD, rather deserted during the weekends, will see a more steady flow of retail traffic.

I wrote last year that online shopping is upending the economics of malls in Singapore. That challenge still holds, and last month’s opening of the Jewel Changi Airport, a five-story glass dome boasting the world’s tallest indoor waterfall as well as 280 stores, has aggravated the oversupply of physical retail. Still, a combination of low interest rates and a government push to remake the city’s landscape could be powerful mitigating forces. Or at least that’s what investors seem to be betting on.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andy Mukherjee is a Bloomberg Opinion columnist covering industrial companies and financial services. He previously was a columnist for Reuters Breakingviews. He has also worked for the Straits Times, ET NOW and Bloomberg News.

©2019 Bloomberg L.P.