(Bloomberg Opinion) -- Buy low, sell high. It’s a great strategy, so long as someone else is willing to take the other side of the trade. Happily for private equity firms, stock-market investors appear to be more than willing to provide the opportunity.

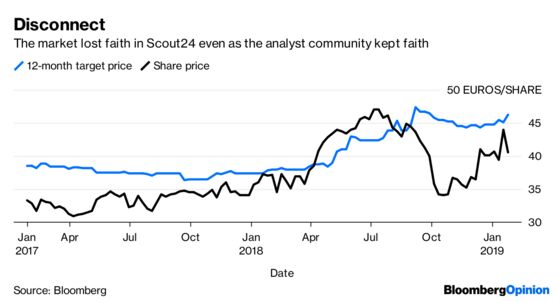

Blackstone Group LP and Hellman & Friedman have been trying to buy back Scout24 AG, the German classifieds group they took public in 2015. Scout24's market value fell sharply last year after lawmakers suggested that property vendors should pay real estate agents’ commissions instead of passing them on to buyers. Investors freaked out at the uncertainty this created for Scout24’s business model. Yet Blackstone and H&F have been prepared to offer 20 percent more than what investors were willing to pay for the shares in December.

Their interest has only hardened the stock market’s negativity: short interest in Scout24 has spiked since then. The suitors may yet be emboldened by Apollo Global Management's deal last week to acquire Britain’s RPC Group Plc – another heavily shorted company, this time in the packaging industry and suffering from stubborn doubts about its ability to generate cash.

Apollo didn't previously own RPC, but it owned a rival, and would have had good knowledge of the assets the company had acquired. The buyout firm agreed to pay a premium of almost 25 percent to where the shares traded as recently as last month – but still well below the stock’s 12-month high.

Are private equity firms getting one up on the market?

The two institutional investors who cried foul at the measly seven times Ebitda Apollo was offering don’t appear to have widespread backing from other shareholders on the register. If Apollo can present a simpler and more transparent business to the world, that alone could enable it to sell it at a bigger multiple of earnings.

At first glance, Scout24 looks like harder work. The rejected 43.50-euros-a-share approach valued it at 5.5 billion euros ($6.3 billion), including debt – a punchy 17 times estimated Ebitda.

UBS analysts assume that Scout24's revenue growth will be hit as the changes to commissions take effect, but its margins, which trail those of Rightmove Plc and Auto Trader Group Plc, will improve slightly. A leveraged buyout firm should still be able to generate an internal rate of return in the mid-teens over four years, the analysts estimate. LBO firms normally seek IRRs in the mid-20s.

But there is a another, much better, potential outcome. Scout24 reckons it should weather any reforms given most German regions already require real estate commissions to be shared between buyer and seller. Suppose the company is right, and margins can expand more rapidly as the business expands. Then the returns would comfortably clear private equity’s traditional threshold.

Meanwhile, the mooted acquisition multiple is still less than what ZPG, the owner of Zoopla, sold for last year. That implies there is scope for Blackstone and H&F to offer more. A counter-bid would keep the two firms honest, but – as with RPC – no other suitor will have quite the same knowledge of the business.

What about the chances of a hedge fund like Elliott Management Corp. holding the would-be buyers to ransom for the last block of shares that would take them to 100 percent ownership? “Don’t bother” is the message. The duo is seeking only 50 percent plus 1 share, according to Bloomberg News. The board should put up a fight, but their incentives aren’t helpful – life under private ownership could be more comfortable.

It is possible that private equity firms are just spraying money around because they have too much capital to deploy, and companies they previously owned feel less risky whatever the noise around the stock. But it’s hard to avoid the suspicion that herd investors, short-sellers in particular, are only providing fodder for better-informed buyout funds.

To contact the editor responsible for this story: Edward Evans at eevans3@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.