Short Sellers Missed Tencent’s $250 Billion Party

They left a lot of money on the table as the Chinese technology behemoth slumped 44 percent from its peak.

(Bloomberg Opinion) -- If there’s an upside to a downturn it’s that short sellers get to make a buck.

By borrowing shares, investors can sell what they don’t own. If the price falls, they buy the stock back at a cheaper level and return it to the lender (with interest), pocketing the difference. Assuming the shares fall enough and borrowing costs aren’t too high, a short seller can make a tidy profit while other investors lose money.

Many company executives hate this process – and the people who engage in it – possibly to the point of indulging in wayward (and expensive) tweets.

Yet if a large, high-flying and well-known company falls 44 percent from its peak, you might expect to see hedge funds and short sellers popping a lot of champagne.

Except if that company is Tencent Holdings Ltd.

Despite the fact that China’s predominant purveyor of social media lost more than $250 billion of market value in the past nine months, short sellers were few and far between.

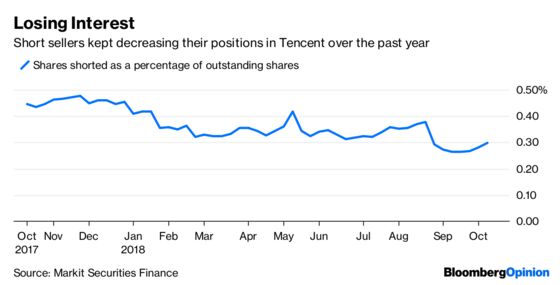

If you look at this one-year chart from Markit – which shows shares shorted as a percentage of those outstanding – it’s clear that short interest is waning. Sure, there’s been a small spike in the past couple of weeks, but the trend is clear.

Less than 0.3 percent of all outstanding shares in Tencent are shorted, according to data compiled by Markit. The highest that level reached in the past year was a mere 0.48 percent in November. (By comparison, short interest in Alibaba Group Holding Ltd. stands above 3 percent.)

That’s a lot of money left on the table by short sellers who could have made a killing.

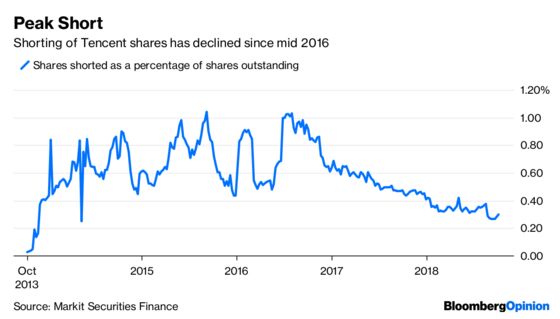

If we zoom out a little and take a look at the shorting action over a five-year horizon, something even more interesting is revealed: Short interest peaked two years ago, after a roller-coaster period, and has been charting a straight line south since then.

One possible reason is rebalancing coupled with fund outflows from Hong Kong exchange-traded funds. Investment advisers, who manage funds on behalf of others, account for 35 percent of disclosed holdings in Tencent, according to data compiled by Bloomberg. Another set of data tracked by Bloomberg shows that Hong Kong ETFs experienced a 13.3 percent outflow over the past year.

Tencent occupies a unique position on investors’ radars. It’s a rare Greater China technology stock that’s listed in a developed market but not the U.S. If your fund remit is to track tech, emerging markets, Greater China, big cap, or non-U.S.-listed shares, then you probably need to put Tencent in your portfolio somewhere. Throw in the internet giant’s “star power” of a year ago, and it wouldn’t be surprising to find some fund managers were overweight.

ETFs account for 16.6 percent of the Tencent stock held by funds, a proportion that’s risen by a third in the past three years. That’s second only to emerging-market funds, which are also often passively managed, with holdings tied to an underlying benchmark. Interestingly, hedge funds own just 0.07 percent of the stock.

By comparison, hedge funds own 4.4 percent of U.S.-listed compatriot Alibaba. ETFs account for just 5.7 percent of that e-commerce company’s reported holdings.

It’s important to remember that correlation doesn’t equal causality. All of this could be purely coincidental, and there are probably other reasons to explain the low shorting action for Hong Kong’s most valuable company.

However, the fact that Tencent has fallen so much this year while short sellers have been largely absent could indicate that the decline isn’t personal – active managers are reweighting their holdings while passive investors are forced to sell in line with fund flows. Short sellers can still profit from these trends by merely riding the escalator to the bottom.

Even if hedge funds didn’t have a particularly negative view of Tencent, they still missed one heck of a short-sell party.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2018 Bloomberg L.P.