Sears Turns Into Wrong Kind of Anchor for Signature REIT

(Bloomberg Opinion) -- Investors, it seems, have come to see only the softer side of Sears Holdings Corp.’s bankruptcy. But there are signs that the likely demise of one of the nation’s largest and oldest retailers could be a lot harder on the economy, and in particular on companies in the commercial real estate business, like banks and REITs, than markets are anticipating.

Earlier this month, Bank OZK disappointed investors with an unexpected 20 percent drop in its earnings. A large portion of the drop came from $45 million in losses on two loans, one of which was tied to a mall that has J.C. Penney and Sears as its two anchor tenants. A report earlier this month from S&P Global Ratings noted that Sears still had $14 billion in revenue in the past 12 months and that going-out-of-business sales could drag down profits for nearby retailers, which includes most national chains, given that Sears is in malls across the country. The S&P analysts also said that the Sears bankruptcy would add to the challenges of second-tier malls, where Sears stores represent about 10 percent of square footage and have been longtime tenants. The mall owners will have to spend a considerable amount of money to be able to redevelop those spaces for new tenants, according to the S&P analysts.

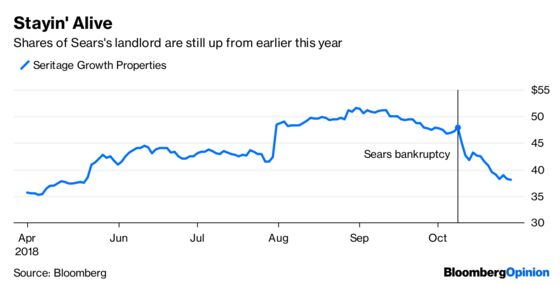

Nonetheless, the CMBX 6, an index of subprime commercial real estate debt that has about the most significant mall exposure that you can find, has fallen just 2.3 percent since news first emerged that Sears was facing bankruptcy. But where investors seem to be the most delusional is in the stock of Seritage Growth Properties, the real estate investment trust that was hived out of Sears three years ago and whose primary tenant remains the retailer. Shares of Seritage have fallen 20 percent since the early reports of Sears’s pending bankruptcy proceedings. But at a stock price of just more than $38, investors are still valuing the company at nearly $1.4 billion. Its true value is most likely much lower.

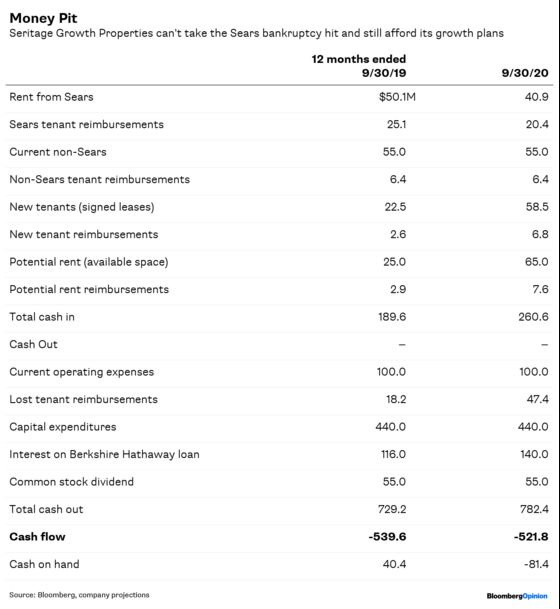

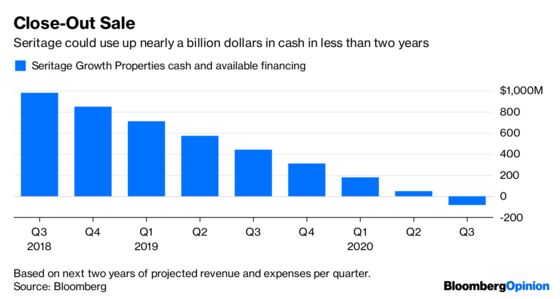

In fact, the Sears bankruptcy and an ambitious redevelopment plan are likely to suck $133 million a quarter out of the REIT’s bank account. Seritage says it has $580 million in cash and an additional $400 million in financing it can readily tap from a credit line from Berkshire Hathaway. But at that rate, Seritage will blow through nearly all of its cash within a year and its additional financing within two. And that’s if Sears is able to reorganize and emerge from bankruptcy with a good portion of its stores open. If Sears instead shuts down completely, Seritage and its shareholders could be wiped out sooner than that.

Schall’s “well positioned” assessment is somewhere between best case and fantasy. Consider that 30 percent figure. Seritage says that’s the percentage of rent it receives from Sears “on a signed lease basis.” The key is that last part. A good portion of those signed leases are not occupied or even generating any revenue and won’t for a while. Seritage has not disclosed its third-quarter earnings yet, but my best guess is that more than 60 percent of its revenue still came from Sears. As for the rent comparison, that’s not apples to apples. Sears does pay Seritage a lower-than-market rent for its properties, most likely because many have not been renovated in a long time. But in return for lower rent, Sears pays additional fees that cover a good deal of the operating expenses of the properties it rents, like utilities and upkeep. Non-Sears tenants cover some expenses, but much less. In the second quarter, for instance, Seritage received 40 percent of its rent from non-Sears tenants but only 13 percent, or just $1.6 million, of its fees.

A bigger problem for Seritage is the rate at which Sears has been shrinking. Annual rent from Sears shrunk to $61 million last quarter from nearly $89 million three months before. Based on that, Seritage is likely to generate $50 million rent from Sears in the next year, along with $25 million in fees. On top of that, Seritage gets $61 million annually from other tenants, which it expects to increase $20 million a quarter for the next two years. That adds up to revenue of nearly $190 million for the next year and $260 million for the one after that.

Here’s where things get messy. Seritage has $100 million a year in operating expenses. As Sears exits properties, Seritage will have to cover more of its own property expenses, which will add up to an additional $18 million in the next 12 months and as much as $47 million the year after that. On top of its day-to-day expenses, Seritage has an ambitious renovation and development plan, which it needs if it is to release all of those former Sears locations. What’s more, many of those signed but not yet occupied leases most likely require Seritage to make upgrades before the tenants move in. Seritage plans to spend $880 million on renovations and development over the next two years.

Then there is some debt service. Seritage took out a $1.6 billion loan in August from Berkshire Hathaway. That loan, which shareholders cheered at the time, has a 7 percent rate and an annual interest payment of $112 million. Some of that loan was used to pay off other debt. The REIT’s access to an additional $400 million in funding also comes from Berkshire, on which it pays 1 percent even if it doesn’t tap it and the full 7 percent if it does, which it will most likely have to do as early as a year from now, raising its total borrowing bill to Berkshire to $140 million a year.

Finally, Seritage has been paying $55 million in dividends to shareholders for the past few years. It has hinted it would stop paying those if its profits no longer justified it, which they haven’t for a while, but Seritage is still making the payments. And those are all cash expenses, meaning Seritage will have to lay out $729 million in cash in the next 12 months. It will collect $190 million in rent and fees, so the cash burn is a mere $539 million, which is manageable but I assume not all that pleasing to investors. The real problem is the next year, when the cash burn shrinks, but not by nearly enough. At $522 million, Seritage, unless it raises more money, will be out of cash by sometime in mid-August of 2020. It could generate some cash from asset sales, but the terms of its borrowing from Berkshire require the firm’s approval, presenting a significant roadblock.

As much as Seritage would like to convince investors that it has distanced itself from Sears and its woes in bankruptcy, the retailer is still a significant anchor. Unfortunately, it’s the kind that pulls everything down.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.