(Bloomberg Opinion) -- Europe’s biggest buyout of 2019 is on the rocks.

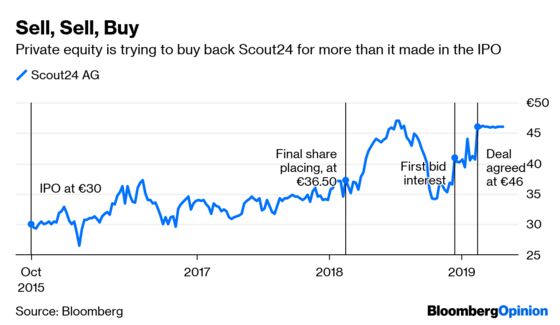

The 5.7 billion euro ($6.4 billion) bid for German classified advertising group Scout24 AG from Blackstone Group LP and Hellman & Friedman looks less generous after the market rally. Investors are pushing back. Add the fact that the private equity firms are trying to reclaim a company they recently took public, and the chance of failure is ticking higher by the day.

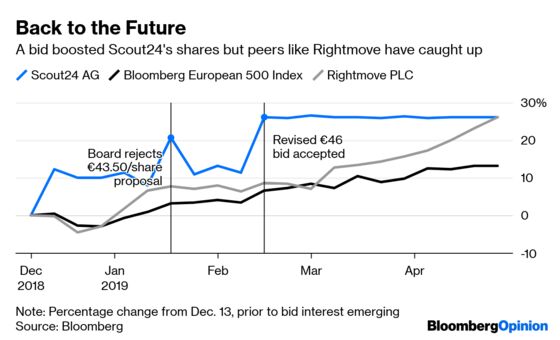

The 46 euros-a-share cash offer is a 27 percent premium to where the target was trading in December before takeover talks emerged. European stocks are up 12 percent since. Peers Auto Trader Group Plc and Rightmove Plc are up 27 percent and 22 percent. If Scout24 had done just as well the deal would offer almost no premium, regardless of its punchy valuation multiple.

Blackstone and Hellman & Friedman say they won’t raise in response to shareholder demands. No wonder: the holdouts are fighting a lonely battle. There’s no rival buyer. Scout24’s supervisory board, led by Hans-Holger Albrecht, boss of music streamer Deezer SA, isn’t championing the minority cause. It agreed to a transaction relatively quickly and continues to back the offer.

It’s this deal or no deal. Even if cunning lawyers can find a way to backtrack on the “no sweetener” statement, budging now would torch the bidders’ credibility. The acceptance condition of 50 percent plus one share is as low as it can be. It can’t be cut to adjust for weak support, as happened amid resistance to the 2017 private-equity bid for drugmaker Stada Arzneimittel AG.

The bidders can’t be completely absolved from the drop in the Scout24 share price that laid the ground for their return. Blackstone and Hellman & Friedman listed the company in 2015 and were out by February 2018. Their last representatives left the board in June. The next month the shares hit a high of 48.62 euros – some 33 percent above the last placing price. All good, or so it seemed.

Things went awry quickly afterwards. Scout24 did an acquisition and the CEO quit almost immediately. When an outsider was appointed in September, the CFO said he would leave this year. At the same time, there were shock government proposals to change the commission structure in German real-estate, prompting the shares to fall to where they started 2018. Then, the bid.

Private equity clearly didn’t set out to engineer a crisis. But would the shares have reacted so badly to the reforms if the succession from private equity supervision hadn’t led to so much boardroom instability? This is a source of annoyance for investors having to weigh this offer in a stronger market.

If there’s not going to be a higher bid, the next best scenario for investors would be staying in as Blackstone and Hellman & Friedman return as controlling shareholders. That result is possible if holders of just over half the shares accept the offer.

Scout24's stock price, at just below the offer level, is saying this is a likely outcome. That may be overoptimistic. The more that shareholders want to stick with the company, the smaller the chance the bid will get the acceptances required for it to go ahead. You can't ride the private equity merry-go-round and get someone else to buy the ticket.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Chris Hughes is a Bloomberg Opinion columnist covering deals. He previously worked for Reuters Breakingviews, as well as the Financial Times and the Independent newspaper.

©2019 Bloomberg L.P.