(Bloomberg Opinion) -- By the end of 2021, the smorgasbord of benchmark borrowing costs known as the London Interbank Offered Rates is due to die. Rendered archaic by shifts in the wholesale money markets, not to mention sullied by rigging, the world’s regulators have deemed Libor no longer fit for purpose.

And yet:

The effort to replace Libor is “the largest financial engineering project the world has ever seen,” Darrell Duffie, a finance professor at Stanford University, said last week. Dubbed in the past “the world’s most important number” by the British Banking Association, the body that used to oversee it, Libor is proving almost impossible to kill off.

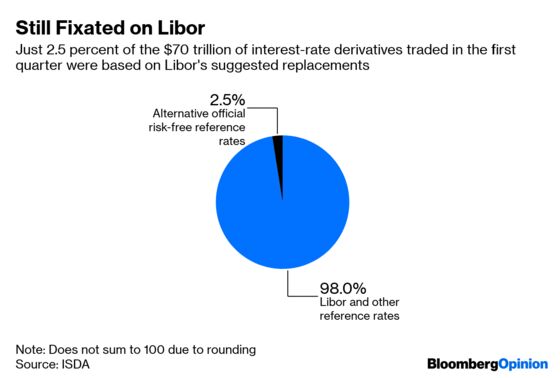

With less than three years to go before Libor is scheduled to end, a new study by the International Swaps and Derivatives Association shows that the interest-rate derivatives market continues to rely on the old benchmark. Just 2.5 percent of the $70 trillion of contracts traded in the first quarter were tied to Libor’s suggested replacements, which include the Secured Overnight Financing Rate in dollars and the Sterling Overnight Interbank Average Rate in U.K. markets.

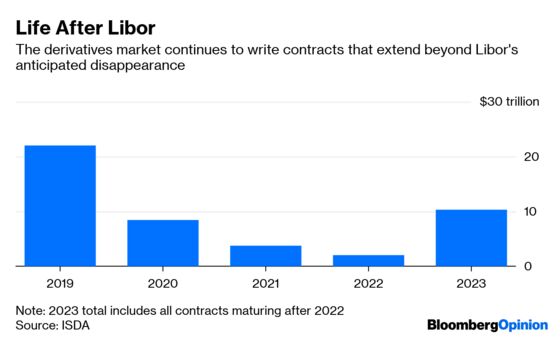

Perhaps more worryingly for the regulators who’ve been urging market participants to work faster to prepare for Libor’s demise is the $10.3 trillion of derivatives traded in the first three months of the year that have maturity dates that extend beyond the 2022 expiry date.

U.K. law firm Linklaters estimates that about $2 trillion of loans will require revised documentation to cope with the disappearance of Libor. That won’t come cheap; Linklaters banking partner Benedict James reckons some banks could end up spending 20 percent more on dealing with the post-Libor environment than they’ve had to lay out dealing with Brexit.

There are technical issues with the suggested replacements for Libor. The U.S. SOFR rate suffers from month-end spikes, while both the U.S. and U.K. flavors demand extrapolations to turn their overnight nature into the three- and six-month reference rates typically preferred as benchmark borrowing costs. Still, the biggest obstacle to the transition remains inertia.

“Many market participants seem to have moved quickly through the stages of anger, bargaining and depression, and have arrived at some level of acceptance,” ISDA Chairman Eric Litvack told an audience of bankers in Hong Kong earlier this month. “Although some of you, admittedly, are still working your way through the depression stage.”

As the deadline for the end of Libor approaches, the scramble to adopt its replacements is likely to accelerate. For now, though, Libor is reminiscent of Schrodinger’s cat — both alive and dead. Whether it survives past the scheduled opening of the box remains to be seen.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.