Aramco’s Cash Flow Gets the Royal Treatment

(Bloomberg Opinion) -- Saudi Aramco has worked hard these past few weeks on displaying resiliency. This week, its owner chipped in to help.

While Saudi Arabian Oil Co., to give its full name, focuses on repairing damage from last month’s attacks, the government wants to shore up the pitch for the forthcoming biggest IPO ever. The latest tool is a presentation posted to Aramco’s website. Like the recent earnings call, it is brief. But tucked in toward the back was an eye-catching number: $75 billion. That is the company’s guidance for a “base dividend” in 2020; a figure 50% higher than the combined dividends of BP Plc, Chevron Corp., Exxon Mobil Corp., Royal Dutch Shell Plc and Total SA in the year through June.

When you’re IPO-ing Bigger Oil, getting a commensurate valuation means promising giant payouts. Aramco seems able to afford it, with free cash flow of $88 billion in the 12 months through June. That said, this is a cyclical business replete with risks; and, as we have just been reminded, Aramco isn’t based in Switzerland.

So there’s another sweetener in that presentation – and one which doesn’t cost Riyadh anything.

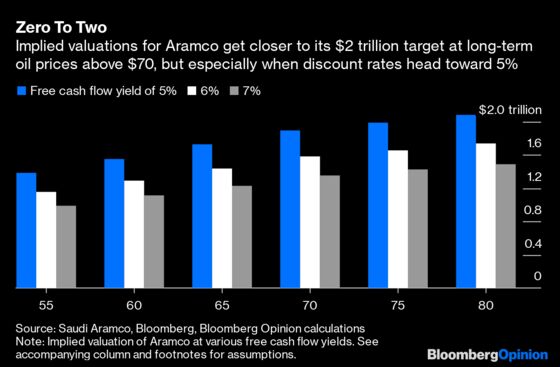

I’ve updated my Aramco valuation from last year using the various bits of pre-IPO marketing, including April’s hefty bond prospectus. The main assumptions are 11 million barrels a day of crude oil production, Brent flat at $65 a barrel, net refining margins of $3 a barrel and chemicals net margins of $100 a tonne. (There are many others, so please see the footnote if you care. ) These spit out free cash flow of almost $87 billion. Put that on a prospective yield of 5.85% (the yield on Aramco’s 30-year bonds plus a 2% risk premium), and the implied valuation is $1.48 trillion – humongous, though still short of Riyadh’s $2 trillion dream.

Saudi Arabia may yet engineer an initial valuation with a two in front of it anyway, with reports of local billionaires being pitched on the idea of chipping in for a domestic listing and fulfilling their patriotic duty. Done artfully enough, this could secure any headline valuation desired, albeit in a way similar to how, way back when, your dad might have paid you $5 for a cup of that homestyle lemonade you pretended to make.

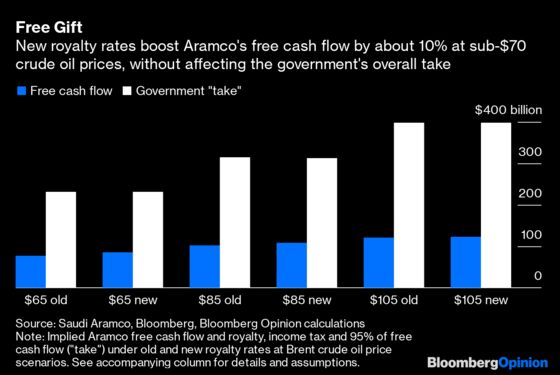

A more fundamental support is that other item in the presentation: a change to Aramco’s royalty rates. These are the cut of revenue from oil and gas production the government takes off the top, operating on a sliding scale determined by oil prices. Under the old system, Aramco paid 20% when Brent crude oil was $70 or less, 40% on the next $30, and then 50% on anything over $100 a barrel. From January 1, 2020, those rates will shift to 15%, 45%, and 80% .

That cut of five points on the lowest tier is especially important, because that is where oil appears to be anchored for now. The biggest surprise arising from the recent attacks on Aramco’s infrastructure is how quickly the market shrugged it off and slipped back into its despair at the direction of the global economy. In taking royalties down at the lower tier but jacking them up for triple-digit oil prices – to the point where virtually none of that excess hits the bottom line – Aramco is signaling it’s built to be resilient, and generous, at lower oil prices, rather than necessarily representing a bet on another supercycle.

On my calculations, using $65 Brent, the new royalty rates add almost $8.5 billion to Aramco’s free cash flow. That’s worth a whopping $145 billion in valuation using the same discount rate. What’s more, given the government reaps money not just at the royalty line, but also in income tax and dividends, the change doesn’t cost it a thing.

This is especially important if Aramco really means to debut at a time of heightened tension in its neighborhood and gathering clouds on the economic front. Unlike the scenario above, Aramco’s crude oil production has averaged only 9.8 million barrels a day this year; and it may have to stay restrained given the weakness in oil prices, with the consensus forecast for Brent in 2020 standing at just $60 a barrel. And Aramco is buying a 70% stake in Saudi Basic Industries Corp., or SABIC, at a cyclical low point, with analysts expecting free cash flow for that company of just $4.7 billion next year.

Plug those assumptions into my Excel contraption, and out pops a free cash flow figure of $65 billion – $10 billion less than that dividend guidance. My model could be off, of course, and 2020 could turn out better; add $5 to oil and 500,000 barrels a day to production and, voila, free cash flow jumps to more than $77 billion. Plus, that dividend is discretionary; and, like one of its peers, Aramco could borrow to cover some of it in a pinch, especially given its low leverage today.

Even so, that change to the royalty regime suggests its current royal shareholder isn’t taking any chances.

Other key assumptions include the following. Upstream production costs (including SG&A, exploration and R&D) of $3.50 per barrel of oil equivalent (BOE). Depreciation of $2.50 per BOE. Corporate tax rate of 50% and interest rate on debt of 3.85%. Capex of $35 billion. Dividend from Saudi Basic Industries Corp. equivalent to 70% of estimated mid-cycle free cash flow of $7.5 billion. Natural gas and ethane production of 9and 1 billion cubic feet priced at $8.50 and $10 per BOE, respectively. Natural gas liquids production of 1.3 million barrels a day, priced at 50% of Brent crude. Refining utilization of 95% on projected net capacity of 3.9 million barrels a day. Chemicals utilization of 90% on projected net capacity of 20.8 million tonnes per year.

Aramco also pays royalties on its natural gas liquidsbut these are negligible.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.