SAP May Need a Massive Buyback to Sing Elliott's Tune

(Bloomberg Opinion) -- It’s a simple enough equation: CEO breaks promises, stock lags peers, activist investor buys stake and tells company to knuckle down and make good on its pledges.

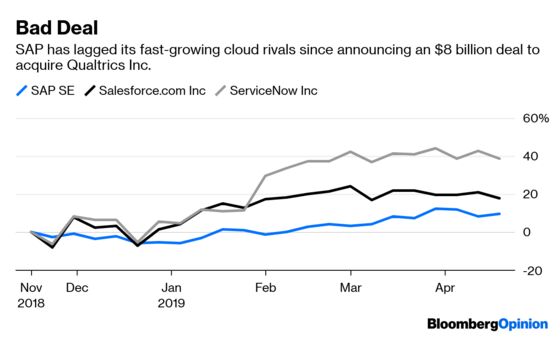

That’s the scenario confronting Europe’s largest technology company, SAP SE. Chief Executive Officer Bill McDermott had committed to improve profitability and refrain from any more major deals at the 133 billion-euro ($150 billion) maker of enterprise software. Then he spent $8 billion on a startup with rapid growth but almost no profit.

Elliott Management Corp. announced Wednesday it had taken a stake of just under 1 percent in the Walldorf, Germany-based firm, the activist’s biggest tech investment since it built a holding in Samsung Electronics Co. three years ago. Given its approach to past acquisitions, it could push for a significant buyback.

The fund, controlled by billionaire Paul Singer, declared the SAP holding just an hour after the German firm announced a new five-year plan to boost profit at its cloud business. The two companies have been in talks for months. The strategy, whose details will be announced in November, is surely the fruit of those discussions. The recent departures of cloud chief Robert Enslin and digital services head Bernd Leukert seem convenient, to say the least.

It’s easy to see where Elliott is coming from. Investors have repeatedly called for SAP to improve the profitability of its cloud operations, which offer companies software to administer processes such as supply chain management, finances and human resources. The gross profit margin of SAP’s cloud business hit 66 percent in the three months through March. Other cloud-centric companies, such as Salesforce.com Inc. and ServiceNow Inc., enjoy a gross margin of 80 percent or more, though based on slightly different accounting standards.

McDermott is now targeting 2023 gross profit from the cloud business that represents 75 percent of sales, and, as he has done previously, is pledging to focus on “tuck-in acquisitions” rather than blockbuster takeovers. SAP has spent $32 billion on deals since he became CEO in 2010, but seemingly at the expense of improving operations.

Elliott is targeting earnings per share of 8.50 euros by the end of the program. Analysts currently forecast EPS of 6.80 euros by then. Even after taking into account the improvements to profitability announced Wednesday, Singer’s goal will likely require significant buybacks, perhaps more than 10 percent of outstanding shares. Investors already seem to be anticipating improved returns – the stock rose the most since 2008.

That would represent a major shift for SAP. The repurchase McDermott announced last year was for less than 1 percent of the stock, and was his first since taking over. The approach would be similar to how Elliott tackled Cognizant Technology Solutions Corp. Soon after Singer declared ts stake in 2016, the Teaneck, New Jersey-based company announced a plan to repurchase about 10 percent of its stock. The shares have since outperformed the S&P 500.

The repurchases at SAP would have an added benefit of neatly tying up excess capital that might otherwise be spent on larger deals.

The risk for McDermott is that, if he doesn’t achieve his profit goals, Elliott could push SAP for divestments, as it has done at Akamai Technologies Inc. and Citrix Systems Inc. For now, the fund has refrained from doing so. And the pressure it’s exerting could provide just the push that SAP needs to deliver value for shareholders.

--With assistance from Chris Hughes.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Alex Webb is a Bloomberg Opinion columnist covering Europe's technology, media and communications industries. He previously covered Apple and other technology companies for Bloomberg News in San Francisco.

©2019 Bloomberg L.P.