(Bloomberg Opinion) -- On the face of it, Banco Santander SA might look as if it’s pandering to investors with the decision to redeem a $1.5 billion issue of its riskiest debt on the expected date. But it’s not. This is just the cold, hard financial logic that Spain’s biggest lender always adopts when dealing with the bond markets.

The bank infuriated many of its debt-holders back in February, when it chose to break an established convention and not redeem (or “call,” to use the industry parlance) a similar 1.5 billion euro note, known as a perpetual contingent convertible (or CoCo for short).

These notes, created after the financial crisis to bolster banks’ financial reserves, offer a generous rate of interest to reflect their riskiness. There has also always been an unwritten rule – in Europe, at least – that they would be called by the issuer on or before their expected redemption date, offering investors some certainty.

But Santander decided to tear that all up in February, after calculating that it would be more expensive to redeem the euro-denominated note and set up a replacement than to just keep it running, regardless of the hurt feelings of investors. This was the first time any issuer hadn’t called one of these CoCos, and the bank’s lack of communication of its intention deeply irked the market.

Given all of this, some market commentators are interpreting Santander’s decision this week to call a separate $1.5 billion (dollar-denominated) CoCo as some kind of olive branch to debt investors. They’re wrong to see it like that.

For one, the dollar-denominated CoCo market is a very different beast to its euro counterpart; American bondholders don’t have any expectation that issuers will redeem the notes automatically.

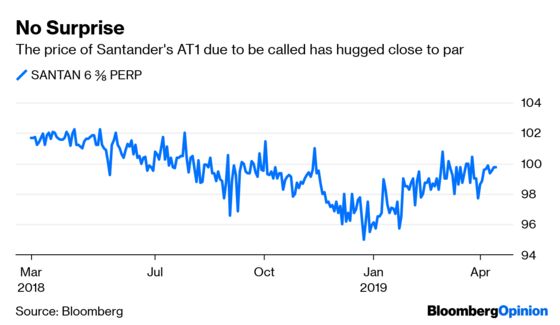

Second, and more important, while it made economic sense for Santander not to redeem the 1.5 billion euro note, the opposite is true with the dollar CoCo: It would cost the bank more to keep the hybrid bond going than to refinance at some future point. At the May 19 redemption date, the bond would have switched from its fixed coupon to a variable rate. That would have boosted the coupon to about 7.2 percent, up from 6.375 percent, which is higher than what it would probably pay for replacement funding.

There’s a lesson here that the hybrid capital market needs to digest: Global banks are duty bound to their shareholders to extend or call this type of debt on the basis of economic rationale alone, rather than some unwritten code of honor. Santander has certainly handed out some painful tutoring on the subject this year.

Smaller euro-area banks that need to work harder to attract investors will no doubt stick to the practice of calling automatically at the first possible date, but you’d be brave to bet on larger lenders sticking by that rule in future.

About the only sop from Santander to its debt-holders is that this redemption notice comes a few days before it had to, no doubt because of the upcoming Easter holidays. But don't confuse this early call for a dollar CoCo as any change of the bank’s practice of doing anything it can to cut its financing costs. It treats every bond individually and conventions are for the birds. Caveat emptor.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.