Taleb Was Right. We’re Still Fooled by Randomness

You know you shouldn’t chase “hot hands” in the fund management industry. This study says you really, really shouldn’t.

(Bloomberg Opinion) -- In his 2001 book “Fooled by Randomness,” author and fund manager Nassim Nicholas Taleb argued that chance plays a largely unacknowledged role in success, particularly in the finance industry. A new study of the returns generated by fund managers suggests that even the minority able to beat their benchmarks are lucky rather than good — and maybe not even that lucky.

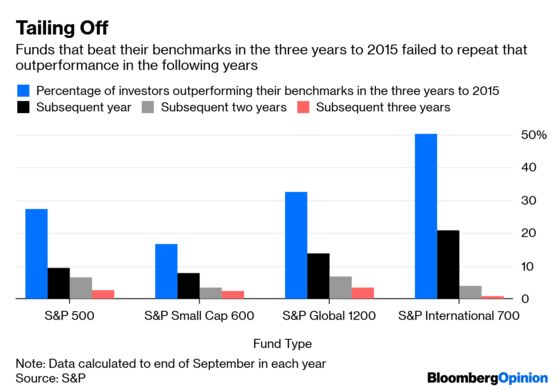

Analysts at S&P Global examined the returns of more than 2,400 investors based in the U.S. Unsurprisingly to anyone who has followed the active-versus-passive debate in recent years, less than a third were able to beat their benchmarks in the three years to September 2015 on an annualized basis and once fees are taken into account.

More remarkably, even those that were able to initially deliver alpha failed to extend their winning streaks in the years after.

Even for U.S. portfolio managers investing in international equities — the most successful group, with almost half of them delivering market-beating performance during the initial three-year period — the luster quickly faded. Less than 1 percent of the winners were able to sustain those excess returns in the year to September 2018.

That’s even worse than the 12.5 percent of outperforming funds that S&P reckons chance alone would produce as persistent leaders in each of the subsequent three years. It seems in investing, luck runs out sooner rather than later.

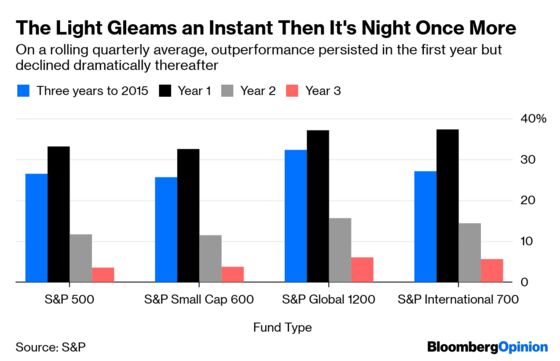

The S&P analysts were worried that “cyclical market conditions” might have skewed their results, which were based on a single point in time, so they redid the calculations using a rolling quarterly average for the time periods. Guess what?

While the picture improves for the first year, by 2018 the number of consistently winning investors drops dramatically once again — suggesting the problem is with the investment managers, not the mathematics.

The health warnings that regulators insist are part of the small print in the marketing materials for the investment industry admit that past performance is no guarantee of future returns. The brochures then typically proceed to stress just how wonderfully the fund in question has performed against some carefully chosen benchmark over whatever time period is the most flattering for its returns. As the S&P analysts say with masterly understatement, “Market participants may want to reconsider chasing ‘hot hands’ or picking managers based on past performance.”

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2019 Bloomberg L.P.