(Bloomberg Opinion) -- Italy managed to scrape by with its 5.5 billion euros ($6.2 billion) monthly auction of three, seven and 20-year government bonds on Tuesday. It has now completed nearly 95 percent of its annual funding target, but that’s where the good news ends. It is still visibly struggling to place longer-dated paper.

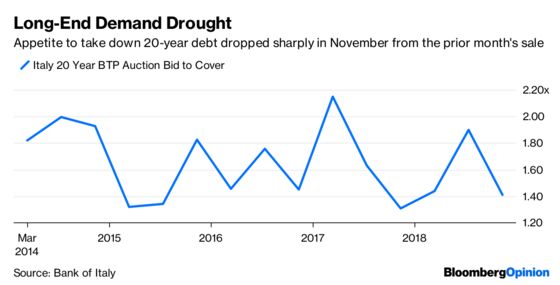

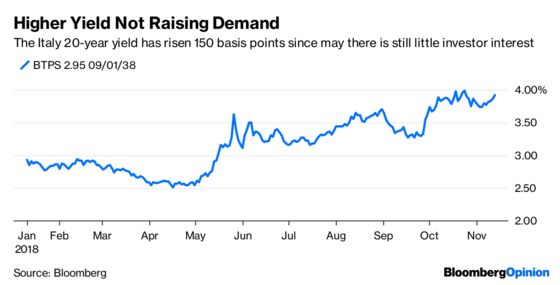

Benchmark 10-year yields stayed high, even after the auction got away. Meanwhile, the sale of the 2038 bond was covered only 1.4 times, down from 1.9 times last month. In fairness, the amount of those 20-year bonds sold was higher this time around, but there was a 3.9 percent yield on offer – 11 basis points higher than October’s sale. With more than 250 billion euros to sell next year, nearly 100 billions euros of which will be 10-year or longer debt, Rome’s funding problems are just beginning.

Investors are naturally nervous about taking a risk on the longer maturities, even more so ahead of the Italian government’s response on Tuesday to the European Union’s rejection of its 2019 budget submission. The populist coalition is expected to stick resolutely to its deficit target of 2.4 percent of gross domestic product.

That will put the onus on the European Commission’s court to decide on a disciplinary course of action by Dec. 4. It could activate the so-called Excessive Deficit Procedure protocol, which might mean Italy being fined for breaching the EU’s Stability and Growth Pact. Not an ideal backdrop for a bond sale.

Tuesday’s auctions failed to inspire increased interest even in the three and seven-year paper, although it’s the shorter term debt that will no doubt help Rome reach its target of raising another 20 billion euros this year – half of which is planned in the five and 10-year maturities.

The Treasury may also choose to adopt, as it has several times recently, to hold so-called “intra-auction taps” and bond exchanges to reduce the pressure of raising large amounts of longer-dated paper at its regular monthly auctions. It’s also launching a new four-year inflation-linked bond aimed at retail investors.

These are all smart ways to avoid having to raise paper where investors are nervous to tread – at least until the budget dispute hopefully reaches some form of conclusion. Italy will hit its 2018 funding target by various creative methods. Next year will be the true test.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.