(Bloomberg Opinion) -- Is it all over?

That’s certainly the impression being given by the French and Japanese governments following the arrest and ouster of Nissan Motor Co. Chairman Carlos Ghosn.

Hours after the Japanese company’s board voted to remove him due to allegations of misconduct, the two countries’ finance and economy ministers met and pledged support for the alliance between Nissan and Renault SA, where Ghosn is still nominally chairman and chief executive officer.

Perhaps this particular body can be swept under the carpet and both sides can agree to go about business as usual. But the tensions that the past week has laid bare aren’t going to vanish so easily — if anything, they’ve been exacerbated. So despite the warm words from politicians, it’s worth war-gaming what Renault and Nissan could do if they wanted to push this situation toward a breaking point. Monday’s events show that what’s unthinkable is no longer quite the same as what’s impossible.

Could Nissan push for control of Renault?

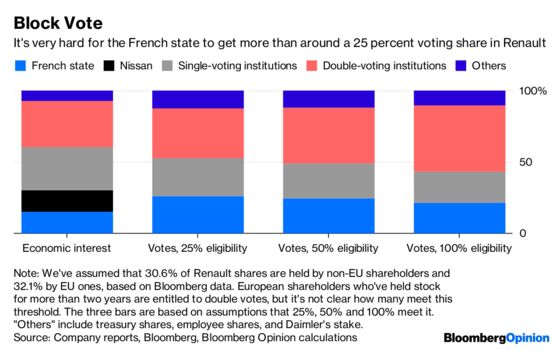

The conventional view is that there’s no way this could be done. France in 2014 introduced a suite of laws designed to make foreign takeovers of key companies more difficult — one reason that the French state’s 15 percent stake in Renault and consequent influence within Nissan has become such an irritant in recent years.

At the same time, these rules aren’t watertight. The one that’s received most attention grants double-voting rights to European shareholders who’ve held their stakes for more than two years. Combined with the fact that Nissan’s 15 percent stake in Renault gets no voting rights (it’s considered a controlled company), that gives the Japanese business a major handicap in any fight for control.

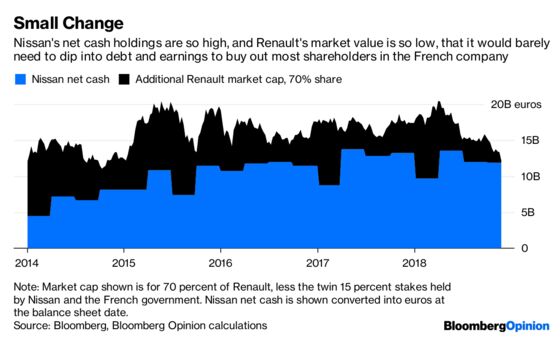

Still, Renault’s valuation has fallen to a desperately low level and Nissan has access to some seriously cheap capital in the form of its net cash holdings and Japanese corporate debt markets. As a result, the Asian company could make a hostile bid over the head of the French government at a valuation so generous that institutional shareholders — many of whom will have the same double-voting rights as the Elysee palace — would be loath to turn it down.

According to Bloomberg’s merger calculator, Nissan could offer 100 euros ($114) per share in cash — a 70 percent premium to current levels, and the best price Renault shares have seen since 2007 — and still increase its earnings per share by more than 70 percent within the first year. Assuming that just 16 percent of shares are owned by European institutions that have held the stock for more than two years, the French government’s blocking vote would remain stuck below 25 percent.

There’s a separate law that requires foreign bidders to seek prior government approval for takeovers in strategic sectors, but it’s hard to argue that car manufacturing has a place on that list, and any attempt to include it would probably violate European Union laws.

It’s unlikely an attack of this sort would succeed in dislodging the French government stake in Renault — but it would remain as a nuisance at best, with Nissan having unprecedented control over the whole group.

Could Renault push for control of Nissan?

This is the other arm of the Mexican standoff. Renault already has 43.4 percent of Nissan shares, so it wouldn’t need to buy many more to move to 50 percent and control of the company.

Nothing as dramatic as a full takeover would be necessary — which is helpful, since Nissan is costlier and Renault’s operating cash flows are weaker. Japanese law treats a two-thirds majority as the more important takeover threshold, and Renault would be allowed to buy shares on-market to top itself up to 50 percent without even launching a formal offer.

To be sure, it wouldn’t be able to control key material issues such as mergers and demergers, and amending Nissan’s articles of incorporation. But it would have the votes to demand non-independent directors of its choosing, and thus get control over company policy.

Will this happen?

With the placatory sounds emerging from French and Japanese politicians, it looks like the danger of all-out war has passed for the moment.

Either of these strategies would be fraught with hazards — financial, operational and even diplomatic. There’s a reason that France and Japan are both seen as being difficult territory for hostile takeovers, and any bid mounted while Ghosn is still locked in a Tokyo prison cell would surely be hostile.

Furthermore, France is further tightening its laws protecting against foreign takeovers, which is likely to make such actions even harder in the future.

Still, it would be foolish to ignore how fragile the truce between the two sides now is, or how potent are the weapons that remain in their armories. This alliance has been held together with bonds of trust, and those withered away in the past week. Even a Maginot Line can be breached.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.