(Bloomberg Opinion) -- After some unsightly stains over the past couple of years, Vanish maker Reckitt Benckiser Group Plc managed to produce a clearer performance.

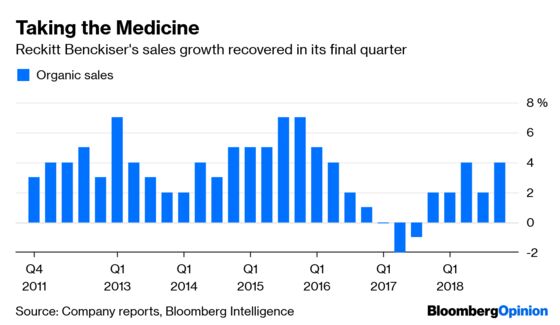

On Monday the group reported better than expected like-for-like sales growth of 4 percent in the fourth quarter, and forecast 3-4 percent expansion this year. The shares rose as much as 5.5 percent in early trading.

Investors really ought to temper their enthusiasm.

Chief Executive Officer Rakesh Kapoor is still on track to step down by the end of 2019 – his departure is all the more puzzling given the good performance at the end of 2018. As I have argued, he’s leaving with the housework half done: Although baby milk maker Mead Johnson improved recently, the company has yet to show that this was the right deal to do. He’s also not taken the separation of the group into a health arm and another division containing its hygiene and home businesses to its logical conclusion: most likely a sale or demerger of the hygiene unit.

It looks like Kapoor ran out of energy to complete the tasks. He’s also left investors somewhat in limbo too. They should bear in mind that the investment case from here rests on the merits of Kapoor’s replacement, and his or her new strategy.

There are two issues a new CEO will have to address. Both are linked to some extent.

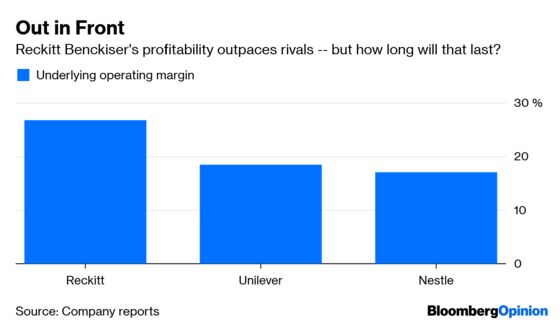

The first is whether Reckitt can maintain its margins, which are higher than rivals’, or whether these will have to be brought down to create the platform to turbocharge sales growth. The company didn’t take this step on Monday – it forecast flat margins this year – but a new CEO certainly could.

The second is the group’s structure. The company said Monday that it remained committed to the separation into two autonomous business units by the middle of 2020.

Analysts at UBS estimate that the hygiene home division could have an enterprise value of between 17 billion pounds ($22 billion) and 20 billion pounds with a 39 billion to 47 billion-pound valuation for health. This would imply a sum of the parts value of 64 pounds to 80 pounds per share. At the bottom end, that’s only slight a premium to the current share price of about 63 pounds, with more upside at the higher levels.

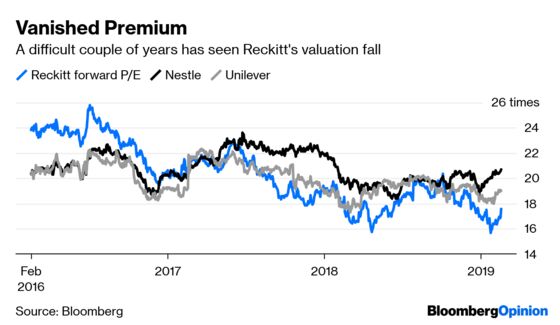

However, extracting the most value means maintaining or increasing profitability. Given the current state of flux at Reckitt, there’s no guarantee that it will clean up.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.