The Real Currency Manipulators Get Off the Hook

Despite all the bluster, China isn’t the worst perpetrator. US allies like Taiwan, Malaysia and South Korea get a lot more leeway.

(Bloomberg Opinion) -- When is a currency manipulator not a currency manipulator? When it’s your friend.

That’s the best conclusion to draw from the U.S. Treasury Department’s latest report on the macroeconomic and foreign-exchange policies of major trading partners, handed up to Congress Wednesday.

China, the regular target of President Donald Trump’s ire, received a section all to itself. Still, the facts don’t lie: Though the Treasury said it was “deeply concerned” by the country’s trade surplus, activities of the People’s Bank in the foreign-exchange market were declared to be “effectively neutral.”

What’s more notable is what wasn’t said in the report, which tends to reflect how geopolitical considerations end up trumping raw economics. The best picture of this comes when you re-run the numbers yourself, to adjust for the way the Treasury puts its thumb on the scales.

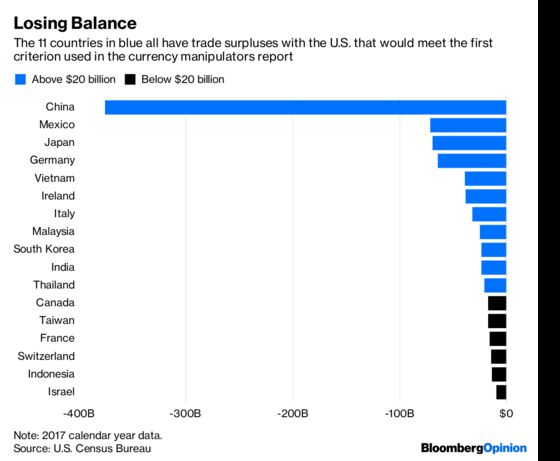

First, let’s look at the countries with which the U.S. has the biggest deficits in goods trade, the first of the criteria now used to label manipulators. Any country that has a surplus of more than $20 billion with the U.S. on this measure is under suspicion. Here’s the list:

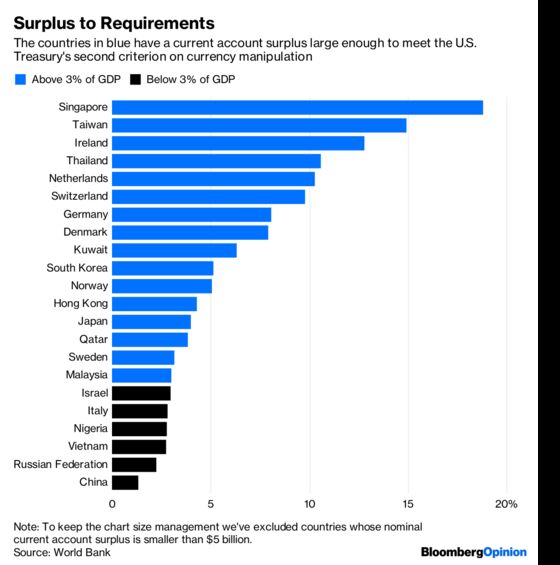

Then we can look at the countries with substantial current-account surpluses. In this criterion, any surplus greater than 3 percent of gross domestic product raises concern. Here’s that breakdown:

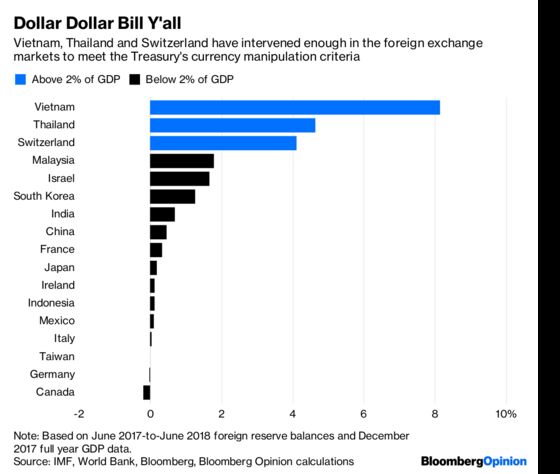

The last measure marks down any country whose purchases of foreign currency equate to more than 2 percent of GDP in a 12-month period. This is a bit harder to calculate so we’ve limited the data to countries on the watch list from the previous two criteria:

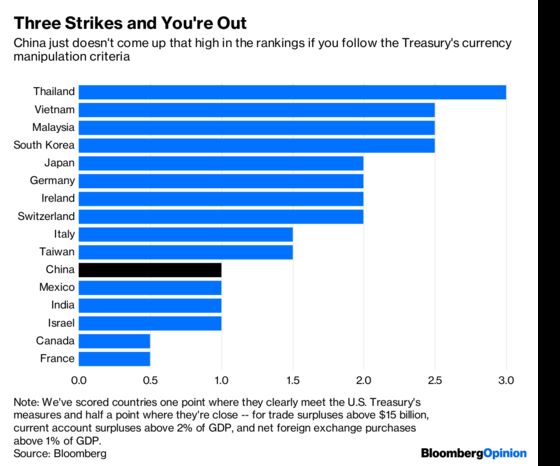

Put that all together and you get the following chart, which suggests that only one country – Thailand – meets all three criteria for manipulation. China is way down the list, on about the same level as Mexico, India and Israel:

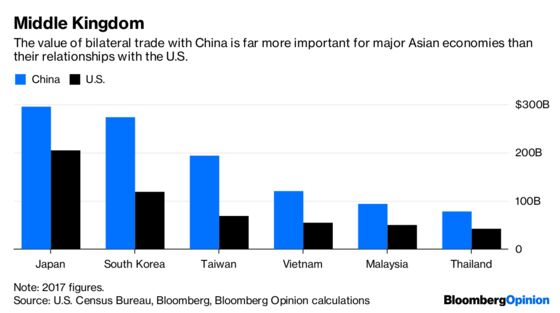

The most striking thing about this analysis isn’t so much China’s low position, but the high position of other Asian countries including Vietnam, Malaysia, South Korea, Japan and Taiwan.

If you think of this report as purely an economic document, it’s strange that this group of countries gets off the hook. Japan, India and South Korea – which is scolded for its “excessively strong external position” – merely get a warning to try harder in the future. As Council on Foreign Relations fellow Brad Setser has pointed out, Vietnam and Thailand (and Malaysia, for that matter) aren’t even mentioned in the report:

That one-sidedness makes a lot more sense if you consider the study not as a piece of financial analysis, but as a tool of economic diplomacy. Thailand, Malaysia, Vietnam, South Korea, Japan and Taiwan are all U.S. allies in Asia that Washington hopes will act as bulwarks against Beijing’s rising global might. Criticizing their exchange-rate policies would risk antagonizing them, and send them spinning back into China’s orbit. Given the long-term stakes, being too fastidious about how they manage their currencies doesn’t make much sense.

Of course, the governments in question know this, and adjust their exchange-rate policies accordingly. This allows Washington’s allies to take advantage of its forbearance and keep their currencies weak, thus boosting their exports to the U.S. But it’s probably not quite right to say this is the main driver of what’s going on.

After all, take another look at the players on our reconstructed sin list. Germany, Ireland, Italy, France and Switzerland are far more concerned with their trading and current-account relationships with respect to the euro than the dollar. They still come up because the criteria assume that the world revolves around the U.S. alone.

That’s the way to think about the Asian economies on the target list. If their currencies end up weaker against the greenback than they should be, that’s really a second-order effect of the thing these countries care about: keeping their exchange rates and export industries competitive in relation to China, by far the more important trading partner.

Getting named in the report doesn’t do much more than allow the U.S. to engage in the same sorts of bilateral talks it’s haltingly pursuing now, but the political pressure for China to be singled out in the next edition, due six months from now, is ramping up. As long as it uses empirical analysis, though, the Treasury will keep coming up against the fact that if anything China has been supporting, rather than depreciating, its currency.

Perhaps a different set of criteria than the ones Washington has been using would produce a result more acceptable to the White House. Still, if you’re going after manipulation, cooking up a new methodology to get the result you want seems a bit on the nose.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.