Rally in Cyclical Stocks Could Be a False Positive

(Bloomberg Opinion) -- Corporate profits and the shares of companies that are most sensitive to the earnings cycle have been moving in opposite directions recently. That doesn’t happen often, but when it does, it almost always signals trouble.

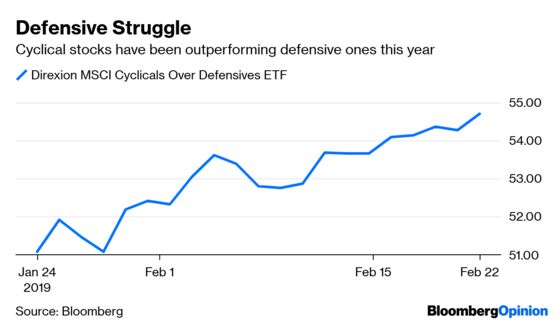

Stocks of companies in cyclical sectors, such as industrials, banking and energy, have been outperformers this year. The Direxion MSCI Cyclicals Over Defensives ETF, which, as the name suggests, measures the relative performance of cyclical stocks against defensive ones, is up 9.5 percent since mid-January, when it started trading. The ETF uses leverage, and the actual difference between cyclicals and defensives is about half that. Still, cyclical stocks, like Bank of America, Boeing and Exxon Mobil, are leading the market this year. The rally is giving some investors renewed confidence in the strength of the current economic expansion, which is already one of the longest but has faced headwinds from rising interest rates and tensions that could ignite a wider trade war.

On Monday, President Donald Trump delayed the date for increasing tariffs on Chinese imports, raising hopes for an end to the trade war. Strategist Jim Paulsen of the Leuthold Group also said in a report on Monday that while his bias is to believe the current expansion is past its expiration date, debt levels for both corporations and households, typically a key warning indicator for slowdowns, remain healthy. Copper prices, often seen as a leading indicator for the global economy, have risen double digits this year.

The problem is that profits are painting a different economic picture. Earnings for the companies in the S&P 500 Index are expected to fall 2.7 percent in the first quarter compared with the first three months of 2018. At the start of the quarter, analysts had predicted 3 percent growth. While the government shutdown was surely a drag in the first quarter, second-quarter profit expectations are also dangerously close to falling into the red. Analysts now think bottom lines will be up just 0.7 percent in the second three months of the year, down from a gain of 3 percent at the beginning of the year. It is rare to have an earnings recession, meaning two quarters of negative growth, without an economic recession, though it happened as recently as 2015.

On top of that, the recent run in cyclical stocks may not be as bullish as it appears; it could just be the market playing catch-up. A year ago, the cyclical-defensive stock story was the reverse of what it is now. Cyclical stocks underperformed defensive ones by about 8 percent in the first six months of the year despite the perception of a robust economy. The drop in those stocks was raising concerns about the economy. In part because of President Trump’s tax cuts, though, growth remained strong and cyclical stocks rebounded. Those stocks are up nearly 14 percent this year, slightly more than the market and higher than the 9 percent return for defensive ones. But the price-to-earnings ratio of the stocks in the MSCI US cyclicals index is 18 times last year’s earnings. That’s down from 22 times in September and is below the nearly 20 times earnings that defensive stocks are trading at, as measured by the MSCI defensive stock index. Cyclical valuations have come back to the pack.

The disconnect last year between the economy and economic-cycle sensitive stocks was resolved with those stocks catching up to the economy. But if they get too far out front this time, the outcome won’t be as pleasant.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.