(Bloomberg Opinion) -- Private equity firms appear to be signaling “Last one out is a rotten egg.” If those powerhouse investment firms smell something fishy, other investors should take notice.

Holding periods — the amount of time between when a buyout firm makes an acquisition until it flips the company back into the public markets or to another buyer — have been drifting down for the past few years around the world. Last year, though, they took a dive, including in the U.S., where they had risen slightly in 2017. In 2018, it was just 4.5 years from buyout to exit in the U.S., according to research firm Preqin. That’s down from an average of 5.1 years in 2017 and the quickest turnaround time the PE market has seen since 2009.

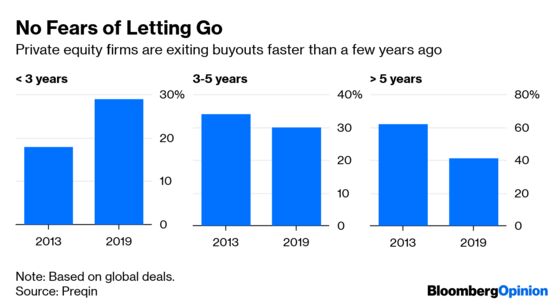

Preqin’s Christopher Elvin, who heads up the firm’s private equity research, thinks it is likely that hold times are down again this year in the U.S., though the data is not yet available. Worldwide, though, it does appear the trend is continuing. Of the investments that buyout firms exited in the first quarter, just 41 percent of the companies had been in their portfolios for more than five years. That was down from 43 percent in 2018. In 2013, it was 62 percent. Similarly, the percentage of companies held by buyout shops for three years or less jumped in the first quarter as well to 29 percent. That’s up from 24 percent last year and a low of 16 percent in 2012.

There could be, of course, several explanations for shrinking private equity hold times. A strong economy makes turnarounds easier to accomplish. Higher interest rates can make buyouts more costly and therefore lower the price acquirers are willing to pay, so sellers may be seizing on that opportunity. A slug of seasoned deals may have been ready to be pushed out the door.

But the mostly likely answer is that PE professionals see economic trouble ahead and are headed for the exits. There is some historical precedent, though the Preqin data on hold times goes back only to 2004. At that time, the percentage of companies held by buyout shops for three years or less was 27 percent. That number jumped to 41 percent the next year and continued to rise until 2008, when deal hold times reached 3.6 years.

Hold periods are unlikely to get that low this time around. PE funds are generally bigger than they used to be, and more and more funds are being raised in which investors are agreeing to have their money locked up for longer. What’s more, investors are generally getting more comfortable with private investments. All told, those forces have spent the past few years expanding hold times, to the point where some had suggested six years or more would be standard.

That’s what makes the recent dip notable. Corporate leverage is at record highs, the economy has been sending some mixed signals, and trade and political winds have been turbulent. Put it all together and you can see why private equity might be smelling some danger and acting accordingly.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.