Why ‘Maximum Pressure’ on Iran Could Backfire

The outcome could determine the direction of oil prices as the U.S. heads toward elections next year.

(Bloomberg Opinion) -- Middle East policymakers in Washington these days should take some advice from that noted diplomat, Bob Dylan.

His adage “When you ain’t got nothing, you got nothing to lose” is getting tested with the Trump administration’s “maximum pressure” sanctions regime on Iran. The outcome of this particular experiment could well determine the direction of oil prices as the U.S. heads toward presidential elections next year.

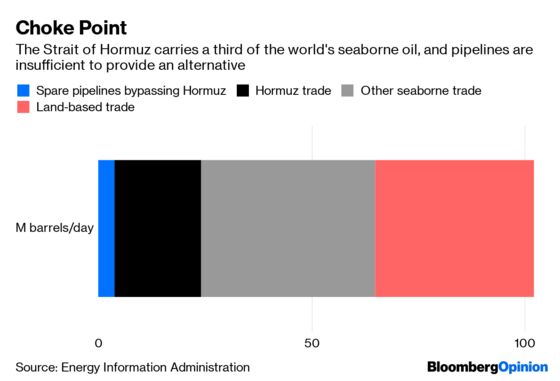

As the recent attacks on oil tankers and a U.S. unmanned drone demonstrate, in military terms it would be relatively easy for Iran to cause disruptions in the Strait of Hormuz, a bottleneck through which about a third of the world’s seaborne oil passes.

The narrowest gap between Omani and Iranian territory in the Strait isn’t much wider than the Strait of Dover. One war-games simulation of a U.S.-Iranian-style conflict in 2002, the Millennium Challenge, resulted in the near-destruction of the “home side” U.S. fleet by an array of guerrilla tactics, such as flotillas of small boats and motorcycle couriers deployed by the “enemy” Iranian team.

Even with President Donald Trump’s latest sanctions on Iran’s leaders and their response Tuesday promising an end to diplomatic engagement, full-blown conflict or a blockade in the Strait is an unlikely outcome. But the relative simplicity of such disruption is a reminder that Tehran’s tenuous investment in the global political and economic order, rather than its military capacity, is the major factor preventing the situation from deteriorating further. That makes Washington’s attempts to erode Iran’s political and economic standing a high-risk game.

This dynamic is most obvious in trade. A key reason that Iran needs the Strait of Hormuz open is because its own crude and natural gas goes through the same passage as the barrels coming from Saudi Arabia, the United Arab Emirates, Kuwait, Qatar and Iraq.

That particular fail-safe is almost gone. Traditionally the U.S. has mostly imposed primary sanctions that only limit American companies from doing business with Iran. As a result, large volumes of Iranian crude tend to keep flowing to importers in Asia and the Middle East.

That’s changed over the past decade as Washington’s Office of Foreign Assets Control has become more aggressive in prosecuting foreign businesses for doing business with sanctioned parties.

When sanctions were first re-imposed by the U.S. last year, Washington initially issued a series of waivers that kept the crude flowing. Since these lapsed at the start of May, Asian importers have turned off the spigots altogether to avoid running afoul of the U.S. government:

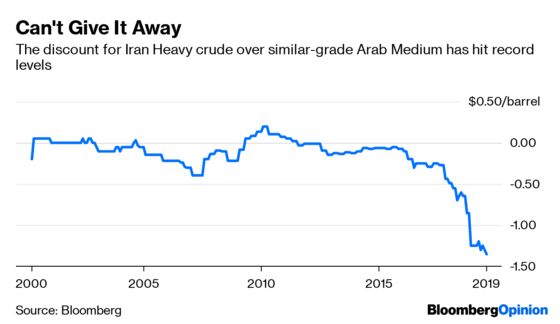

The 225,000 barrels a day shipped during May was the lowest volume in Bloomberg-compiled figures dating back to 2015. The average pace of export shipments so far this year has come to about 993,000 barrels, comparable to the record-low figures for total exports recorded in the immediate wake of the 1979 Iranian revolution.

Killing Iran’s key oil-export market is certainly imposing a great deal of pain on its economy. Real gross domestic product will fall by 6% this year and consumer price inflation will hit 37%, according to the International Monetary Fund. Yet that's unlikely to bend Tehran to Washington’s will, and in the meantime it’s actually increased the risks around Hormuz. With barely any Iranian oil flowing anyway, the further economic pain Tehran would suffer from disrupting traffic through the Strait would be trivial.

At this point, the key factor preventing Tehran from striking back harder is primarily its desire to win the game of public perception. Currently, the rogue regime in the Gulf is the U.S., which blew up the Joint Comprehensive Plan of Action on Iran’s nuclear program when the Trump administration pulled out of it a year ago. Iran’s behavior to date has been carefully calibrated: just aggressive enough to keep a tit-for-tat game going with the U.S., but not so combative that it loses the support of Russia, China and Europe.

“Up until the point they pull out of JCPOA they have moral authority in their favor,” said Rodger Shanahan, a research fellow on Middle East issues at the Lowy Institute in Sydney. “If they threaten to close the Strait and increase their attacks, that goes away.”

The more likely outcome is further attempts by Tehran to push the boundaries of the JCPOA, said Shanahan, such as Iran’s announcement last week that it would exceed a cap on its stockpiles of low-grade uranium. Such actions can create new facts on the ground that can be traded away in any future negotiation with Washington, so as to ensure the resulting agreement is substantially the same as the one the Trump administration pulled out of.

That's hardly comforting. Indeed, it more or less guarantees that the current game of provocation and counter-provocation will continue until both parties reach a stalemate. With the safety nets preventing this from deteriorating into a crisis growing so threadbare, the risks of a miscalculation will only increase.

The Bloomberg figures are derived from ship movements and don’t take piped exportsinto account, so the most recent numbersmay understate thingsa bit.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.