Pfizer’s $11 Billion Cancer-Drug Deal Takes Pricey Path to Growth

(Bloomberg Opinion) -- Pfizer Inc. is demonstrating once again how expensive it is for pharma firms to buy their way to growth.

The company announced Monday morning that it’s paying almost $11 billion for cancer drugmaker Array Biopharma Inc. The deal would bolster Pfizer’s cancer portfolio and add medicines that could meaningfully augment sales and profit. But the company isn’t getting much of a bargain, and its recent track record with a similar deal is a cautionary tale for investors.

Pfizer’s relatively anemic projected sales growth and drug pipeline mean that, cost aside, a deal like this makes sense. Cancer is a particularly attractive market for drugmakers, offering both limited pricing pressure and an expanding set of potential treatments and areas to target; Array’s lead medicines Braftovi and Mektovi are already approved for melanoma patients and recently produced promising data in colon cancer. Also, the company has developed drugs for other companies that would net Pfizer royalties.

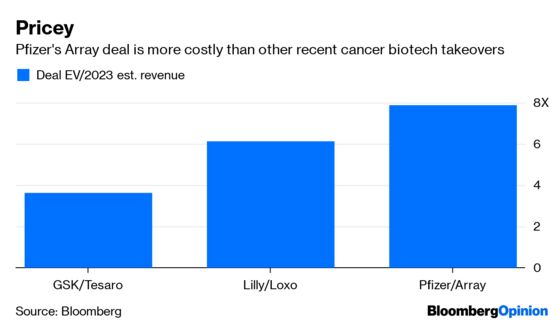

But cost does matter when assessing a deal and in this case it seems excessive. Pfizer is paying a 62% premium on a stock that had already appreciated by more than 100% in recent months. Acquiring drugs that have been approved is always extra expensive, but Pfizer really ponied up here. Pfizer is paying nearly 8 times Array’s projected 2023 sales, which is higher than what GlaxoSmithKline PLC and Eli Lilly Inc. paid in comparable recent deals for Tesaro Inc. and Loxo Oncology Inc., respectively.

Array is expected to generate $274 million in revenue this year, and that figure is expected to pass $1 billion by 2022. That growth is still theoretical, though, and the company’s current product roster would have to exceed expectations to justify this price. Its many partnerships with other companies also limit its upside.

All of this suggests that Pfizer is also paying up for Array’s extensive drug development expertise and broader pipeline. It could do worse on that front; Array has been unusually successful at inventing medicines. But Pfizer may not be able to retain the scientists that have turned Array into an R&D powerhouse or get the most out of what’s currently in the company’s labs.

Pfizer’s last big oncology deal demonstrates the danger of paying up based on optimistic evaluations. The company bought Medivation for a hefty $14 billion in late 2016 for its prostate-cancer drug Xtandi and several pipeline assets. It’s only been about three years, but so far no part of the deal has lived up to Pfizer’s expectations or the price paid.

Array may well help Pfizer transition into a more significant player in the cancer market or prove to be a bargain. But there’s a decent chance that we’ll be back for round three in just a few years.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.