Pew Got It Wrong. Pension Funds Need Alternative Investments.

(Bloomberg Opinion) -- The Pew Charitable Trusts is out with a report on public pension funds featured the arresting subtitle: “Substantial investment in complex and risky assets exposes funds to market volatility and high fees.” There are two independent assertions here, both misleading.

The first is that investment in risky assets exposes pension funds to market volatility. True enough, but the report documents that the amount allocated toward stocks has fallen from 61 percent in 2006 to 48 percent in 2016, the latest year for which data are available. So, the subtitle is true, but a fairer version might be “Declining investment in risky assets reduces funds' exposure to market volatility.”

The second assertion concerns complex assets and high fees. Public pension funds pay about $12 billion in investment fees per year, and underperform passive investment strategies as a group by about the same $12 billion. But the funds paying higher fees and making more use of alternative investments are not the ones paying the cost. With some exceptions, they outperform passive after the higher fees. The worst net performances versus passive are seen in funds with moderate fees and low allocation to alternatives.

Average stated investment fees have increased to 0.33 percent in 2016 from 0.26 percent of assets in 2006. But fees are not stated in standard ways, and may not represent the full cost of investments. I prefer to use an implied figure. I compute the return if a fund used the same allocation among stocks and bonds, but had used Vanguard index funds. The average pension fund would have earned an annualized 5.91 percent over the last 10 years with Vanguard, but the actual average return was 5.55 percent, suggesting the funds paid 0.37 percent in true economic costs over the sticker price to invest in a passive vehicle.

Again the subtitle is literally true, but it suggests a link that does not exist between “complex” alternative assets and high fees and high risk. Alternatives as a group have significantly lower volatility and much lower market exposure than traditional portfolios limited to long-only investments in stocks and bonds. And there is a significant negative correlation (-0.36) between fund allocation to alternatives and implied investment fees paid — more alternatives means lower fees. The alternative asset class contains many low-fee products, and there are plenty of managers who charge high fees to invest in stocks and bonds.

The match between $12 billion paid in fees and $12 billion of underperformance relative to passive suggests public pension funds as a whole would be better off scrapping active management and alternative investments, and putting all their money into low-cost passive index funds. The amount paid in fees came straight out of net performance. There was no additional return associated with active management or alternatives. But what's true for public pension funds as a whole is not true for all funds individually.

Look at the graph below of stated fees paid versus fees implied by subtracting actual fund performance from its passive benchmark. The funds with negative “realized investment cost” earned more from outperforming a passive allocation strategy than they paid in fees. The funds with high realized investment cost either paid a lot in fees, or underperformed passive by a lot, or both. The data show no clear pattern between low or high fees and superior performance net of fees. The funds with the highest realized investment cost had the worst net performance and paid average to moderately above average fees. But the lowest stated fee funds, as a group, had slightly below average net performance. The best net performances were turned in by funds paying a range of fees from about half the average to three the times average. The two funds reporting the highest fees did not have terrible net performance.

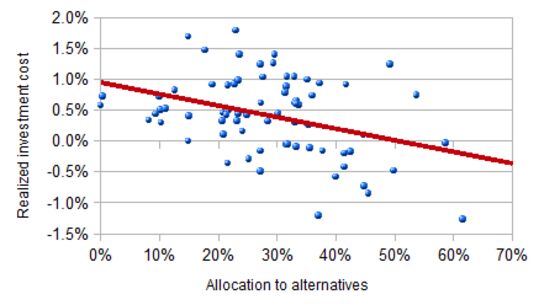

We get a clear picture if we graph realized investment cost versus allocation to alternatives. While there is quite a bit of variation around the trend, higher allocation to alternatives is associated with better net performance relative to passive investment. The red regression line suggests that going from zero to 50 percent alternatives improves net performance by one percent per year on average. No fund with less than 20 percent alternatives beat passive over the last 10 years. Since alternatives also likely reduce risk, it seems to be a win-win.

The Pew report suggests that funds should cut market risk and fees paid, meaning put more money in passive bond index funds or U.S. Treasury securities. But a more granular look at the data suggests funds should be willing to embrace more broadly diversified portfolios and to pay fair fees, and that the damage is done by high fee investments that underperform passive, not by any particular asset class.

To contact the editor responsible for this story: Robert Burgess at bburgess@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Aaron Brown is a former Managing Director and Head of Financial Market Research at AQR Capital Management. He is the author of "The Poker Face of Wall Street." He may have a stake in the areas he writes about.

©2018 Bloomberg L.P.