(Bloomberg Opinion) -- If any sector deserves a digital shakeup, it’s consumer banking. The highly-concentrated market is dominated by incumbents that rake in huge profits from bog-standard services like overdrafts and ATM withdrawals. So it’s heartening to hear that several billion-dollar European fintech startups are eyeing the U.S. for expansion. That doesn’t mean they’ll succeed.

The latest such firm to confirm an imminent stateside incursion is N26, a German banking app with 2.3 million customers across Europe that reckons it can grab about half that in the U.S. within one to two years. N26 has raised $300 million to fund its expansion, giving it a $2.7 billion valuation. Billionaires Peter Thiel and Li Ka-Shing were already backers.

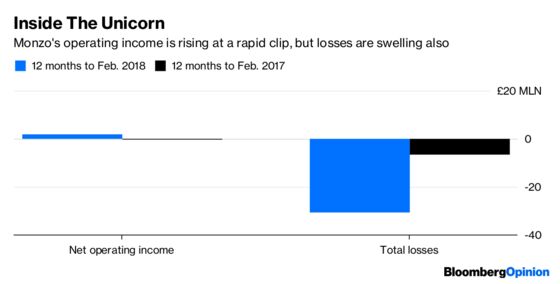

N26 isn’t alone. British rival Monzo also wants to raise money later this year for a U.S. foray, while Revolut — a money-transfer app that won a European banking license last year — says it already has about 75,000 people on the waiting list for its American launch. Both have billion-dollar price tags.

Cracking the U.S. holds obvious attractions. It has a population of almost 350 million that speaks one language and spends one currency. Those aforementioned retail-banking fees might offer the European upstarts, who have no branch networks to maintain, something fat to undercut. And even if mobile banking is already everywhere in the U.S., surveys indicate that active customer engagement has room to grow. Less than half of U.S. banks have more than 20 percent of their customers actively using a mobile device service, according to a December 2017 paper from the U.S. Federal Reserve.

But a U.S. adventure for Europe’s fintechs also means running head-on into the twin problems of regulation and competition. These startups don’t have U.S. bank licenses, and probably don’t want to spend time and resources on getting one. While regulators have made steps toward embracing fintech firms, navigating the thicket of U.S. rules is tough. That means partnering with an existing bank on American soil, rather than disrupting it out of existence.

And as funky as N26 or Monzo’s mobile-banking apps are, it’s not clear that they have the means to outspend the Wall Street stalwarts or outshine them with whizzy apps. JPMorgan Chase & Co. earmarked an extra $1.4 billion on digital investments alone last year, and has rolled out a nationwide mobile-only bank app called Finn. That’s not to say suit-and-tie bankers are inherently better at coming up with good products, but they might have more money to hire the right people who are.

It’s the money-making potential of these fintech startups that’s really at question. These firms are following the cash-burning, fast-growing trail blazed by Silicon Valley: Go full tilt to gain scale, amass a huge customer base, then worry about profit later. But when your business model relies on cross-selling other products, heavy marketing spend and price-cutting, it’s easy to see how losses might pile up. When the manic growth spurt finally stops, those unicorn valuations may be in trouble.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering Brussels. He previously worked at Reuters and Forbes.

©2019 Bloomberg L.P.