Don’t Let Stocks’ Big Dogs Crowd Out the Small Ones

(Bloomberg Opinion) -- There are roughly 3,700 public companies in the U.S., and most stock investors ignore all but the biggest ones, which is a bit odd. If, as investors routinely claim, their goal is to broadly diversify their portfolios, or assemble a mix of stocks that promises the best risk-return tradeoff, or find the best businesses, then overlooking broad swaths of the market makes little sense.

In fact, the big boys have rarely been more popular than they are today. Investors have poured money into behemoths such as Apple Inc., Microsoft Corp., Amazon.com Inc., Facebook Inc., Google parent Alphabet Inc., and more recently Tesla Inc., and in the process ballooned their market value relative to the rest of the field. As a result, those six companies now account for more than 40% of the Nasdaq 100 Index by weighting and a quarter of the S&P 500 Index, making it the most top heavy since at least 1980.

Even broader market indexes are dominated by the largest companies because most of them, or at least the most recognizable ones, are weighted by the market value of their component stocks. The largest 650 stocks in the Russell 3000 Index by market capitalization, for example, account for 90% of its weighting. That explains why the performance of the Russell 3000 since inception in 1979 has been indistinguishable from that of the S&P 500. No matter how you slice it, buying the broad market is almost always a bet on the biggest players.

The bias in favor of big companies is even more curious when you consider that small-cap stocks have outpaced large caps historically. The smallest 30% of U.S. stocks by market cap have outpaced the largest 30% by 1.7 percentage points a year since 1926 through October, including dividends, according to numbers compiled by Dartmouth professor Ken French.

So why do investors prefer big to small? One reason, as skeptics of small caps are quick to point out, is that they don’t trade as much and are therefore more expensive to buy and sell, a detail that the back-tested record ignores. Those additional trading costs might have more than wiped out any advantage small caps offered historically.

Smaller companies are also riskier because they’re, well, smaller and less established. That’s clear in the numbers. Shares of small caps have been 60% more volatile than those of large caps since 1926, as measured by annualized standard deviation, and their drops have often been more harrowing. After accounting for that additional risk, large caps regain the edge. They produced a Sharpe Ratio— a common gauge of risk-adjusted return — of 0.39, compared with 0.3 for small caps.

That hardly settles it, though. For starters, investors don’t have to choose between large and small. It turns out that a balance of the two would have produced a higher absolute return, and a comparable risk-adjusted return, than owning large caps alone. That’s because the two don’t move perfectly in tandem, so a meaningful allocation to both dampens the volatility of owning just the small caps while still capturing some of their upside. A 50/50 mix of large and small caps has outpaced the S&P 500 by 0.8 percentage points a year since 1926, and with nearly identical Sharpe Ratios.

Of course, few people have 100 years to invest, so it’s also important to look at the data over shorter rolling periods. And there, too, the odds favor a balanced approach. The 50/50 mix beat the S&P 500 close to 70% of the time over rolling 10-year periods since 1926, and its Sharpe Ratio was higher 62% of the time.

As for trading costs, they’re probably less of a burden than many fear, at least when investing in small-cap index funds. Markets have become more liquid and orderly over time, which has pushed costs down. Vanguard Group’s Small-Cap Index Fund, for example, has beaten the index it tracks by 0.05 percentage points a year since inception in 2000, despite that the index ignores the impact of trading and other costs.

Still, not everyone is persuaded that small caps have a role in portfolios. To see why, you have to go back a few decades to a time when small companies were even further off investors’ radar than they are today. In 1978, a doctoral candidate at the University of Chicago’s business school named Rolf Banz wrote a groundbreaking dissertation showing that small caps had historically beaten large caps. When the paper was published three years later, a wave of small-cap mutual funds followed. Today, there are more than 3,000 small-cap mutual and exchange-traded funds, according to Morningstar.

It happens that in the years since Banz published his paper in 1981, small caps haven’t shined as brightly as they did before. From 1926 to 1980, they beat large caps by 3.6 percentage points a year with a slightly lower Sharpe Ratio. They also won 85% of the time over rolling 10-year periods and produced a higher Sharpe Ratio 65% of the time. Since then, it’s been an entirely different story. Large caps have won by 0.9 percentage points a year, and with a much higher Sharpe Ratio. They also beat small caps 50% of the time over rolling 10-year periods and produced a higher Sharpe Ratio 72% of the time.

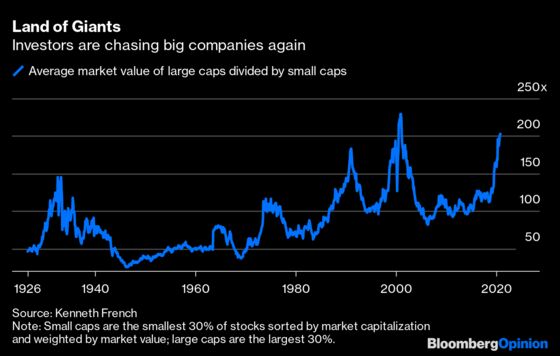

For many, it’s a cautionary tale about how quickly an investing strategy can sour when it’s broadcast to the world, but there’s more to the story. The years since 1980 have been bookended by two highly unusual periods for large caps. The first is the two-decade bull market in the 1980s and 1990s that favored big companies, eventually lifting their market value relative to small caps to record heights. Since 1926, the market value of large caps has been 87 times that of small caps, on average. By the peak of the dot-com bubble in 2000, however, that multiple had swelled to 230, by far the highest ever recorded (for stats aficionados, a 3.7 sigma event).

When the bubble burst, the size differential between large and small gradually returned to its historical average and hung around there for much of the 2000s. That helped small caps outpace large caps by 7.5 percentage points a year during the 10 years from 2000 to 2009. But in the years since, large caps have swelled again to more than 200 times the size of small caps, outpacing small caps by 4.1 percentage points a year over the last decade.

All of that leaves some questions unanswered, unfortunately. Have large caps reached a permanently high plateau, in the ill-timed words of economist Irving Fisher, or are they poised for another decade of disappointment relative to small caps? Has the market entered a new era of extreme swings between large and small caps, with neither one gaining any long-term advantage? And as the historical record now stands, is the edge for small caps large enough that it can confidently be called a signal rather than noise?

It’s hard to be sure about the answers, but thankfully there’s an easy and sensible way to sidestep the uncertainty: Don’t bet on one size fits all.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2021 Bloomberg L.P.