Pension Funds Should Think Twice About Alternatives

(Bloomberg Opinion) -- High-performing alternative investments are great if you can find them, but pension plans shouldn’t count on it.

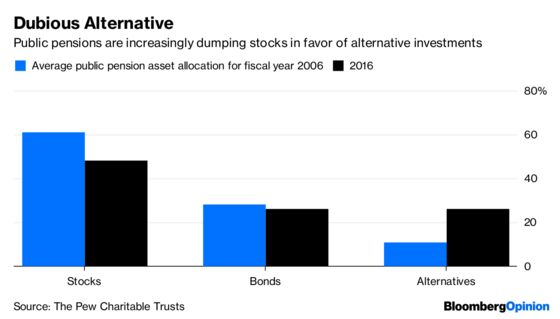

The Pew Charitable Trusts recently published its latest report on the investment practices and performance of the 73 largest state public pension funds as of the 2016 fiscal year. The big development is that pension funds are moving their money from stocks to alternatives such as private assets and hedge funds. The average allocation to alternatives more than doubled to 26 percent in 2016 from 11 percent a decade earlier, with a roughly equal percentage leaving stocks.

In an accompanying blog post, Pew warned that the move to alternatives would result in more volatility and higher fees for pension funds. Writing for Bloomberg Opinion, investor Aaron Brown took the opposite view last week, arguing that alternatives dampen volatility and boost performance, even after accounting for fees.

Neither view is entirely right. And with an estimated $1 trillion in state and local public pension funds invested in alternatives, and the retirement of 19 million current and former state and local employees at stake, decision makers rushing into alternatives should be clear about what they’re buying.

It’s not surprising that alternatives appeal to pension funds. The average fund in the Pew study hopes to generate an annual return of 7.5 percent. With interest rates at historic lows, bonds are unlikely to deliver. Stocks have a better chance, particularly in more reasonably priced markets outside the U.S. But stocks are also riskier, and that risk is unnerving to pension funds desperate to avoid shortfalls.

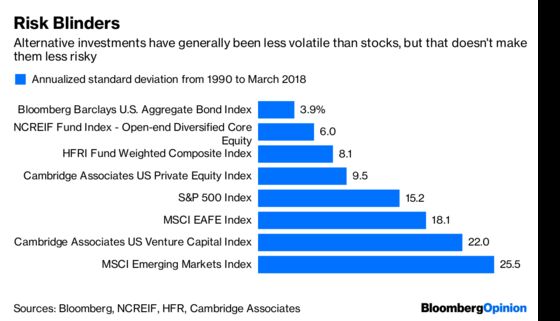

Enter alternatives, a seemingly perfect, well, alternative. For much of the period between 2006 and 2016, the trailing returns of private assets and hedge funds were enticingly higher than those of stocks. And given that investments in private assets and some hedge funds are not marked to market, and that many hedge funds wager both long and short bets, the volatility of alternatives looks more like that of bonds than of stocks. Stock-like returns with bond-like risk. Problem solved.

Except it’s not that easy. For one thing, volatility is a useful proxy for risk when it comes to stocks and bonds, but not so for alternatives. It’s nonsensical to believe that investments in startups or leveraged buyouts or those tied to commodity prices are less risky than the broad stock market. Or that the muted volatility of hedge funds fully reflects the risk that their long and short bets could simultaneously sour. A more sensible assumption is that alternatives are as risky as stocks, and in many cases riskier, despite their lower volatility.

A more obvious pitfall is cost — and there’s no doubt that alternatives are more expensive than stocks. The 2-and-20 fee structure — 2 percent of assets and 20 percent of profits — is still the norm in venture capital, private equity and other private assets. Hedge fund fees have dropped closer to 1.5 and 15, but that’s still more expensive than actively managed stock mutual funds, whose fees generally range from 0.5 percent to 1 percent depending on the strategy. And let’s not forget the huge variety of stock index funds with fees approaching zero.

In fact, while Pew’s numbers don’t show how much pension funds pay for stocks versus alternatives, the available numbers suggest that alternatives take a bigger bite. There’s a positive correlation (0.57) between the funds’ allocation to alternatives and the fees they paid to external managers in 2016, but a negative correlation (-0.56) between their allocation to stocks and those same fees. In other words, a higher allocation to alternatives is associated with higher fees, while a higher allocation to stocks points to lower ones.

In most cases, those higher fees don’t translate into higher returns. As I showed recently, the top 10 percent of hedge funds have produced stellar net-of-fee returns, while the rest have generally been mediocre or worse. The same is true of the top 25 percent of venture capital and private equity funds relative to others. But there’s far more pension money chasing alternatives than top managers can accommodate, never mind all the other investors competing for those same funds.

There’s no reason to believe that the average pension fund would be better off with alternatives and good reasons to believe that it would most likely be worse off. By all means, those with access to the best funds should dabble in alternatives, but everyone else should stick with stocks.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2018 Bloomberg L.P.