Why We Can Forget About a Rate Cut in China

Borrowing costs are already below neutral and lowering them won’t help funnel credit to private businesses, researchers argue.

(Bloomberg Opinion) -- Those arguing China will cut interest rates are likely to be disappointed, even if the country fails to reach a trade deal with the U.S.

In its latest quarterly policy report, the People’s Bank of China signaled it will continue to use more targeted policy tools to boost credit, such as reserve ratios and medium-term lending facilities.

Parsing PBOC reports is like reading Federal Reserve statements – many carefully drafted and nebulous words that can be interpreted to the reader’s liking. More interesting are four research articles also published this week in the Financial News, an outlet overseen by the central bank. The benchmark lending rate is already “below neutral,” the central bank’s research department wrote in one.

Here’s the department’s back-of-the-envelope case: The neutral rate for emerging markets is 4 percentage points below a country’s GDP growth rate. Since China is growing at a real rate of roughly 6.9 percent, that translates to 2.9 percent, plus 2 percent for inflation, for a neutral rate of 4.9 percent. The central bank’s current benchmark one-year lending rate 4.3 percent.

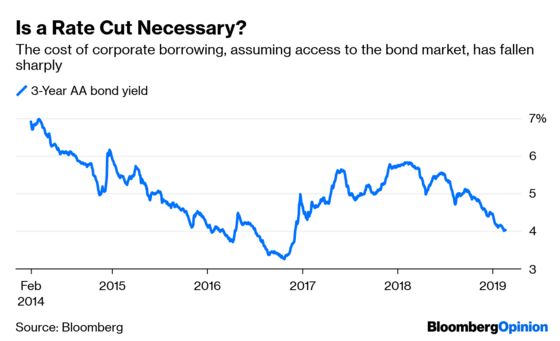

Even if you disagree with the PBOC on what the true GDP growth rate is, China Inc. isn’t paying higher costs of financing onshore, the research department argued. One-year dollar notes on average yield at least 2.9 percent. Adding on currency hedging and transaction costs brings the total cost of offshore borrowing to at least 4.35 percent.

The central bank has a point. Since last September, China’s $12 trillion bond market has been staging a bull run. The cost of financing – assuming you’re able to tap the market – has tumbled.

Intriguingly, the PBOC acknowledges that China may have “capital swamps” – pockets of excess funds and lower financing costs – and that interest rate differentials may be here to stay. The cost of financing in the three tier-one cities of Beijing, Shanghai and Shenzhen is 20 basis points to 80 basis points lower than elsewhere in China, according to the researchers.

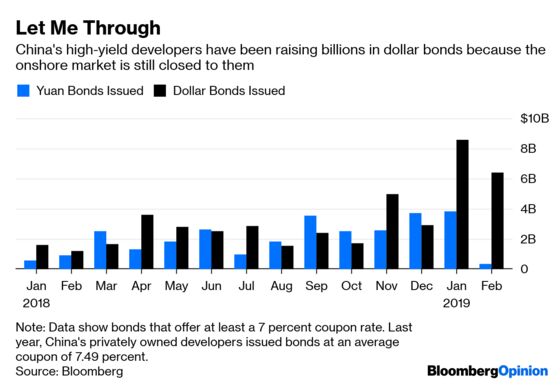

The true cause of China’s credit crunch isn’t higher rates, but the availability of financing. The state sector has no trouble getting loans, and is benefiting from the PBOC’s liquidity easing. Private businesses, on the other hand, continue to have limited access to credit. High-yield developers are still going offshore to raise funds because they can’t borrow from banks or sell bonds onshore.

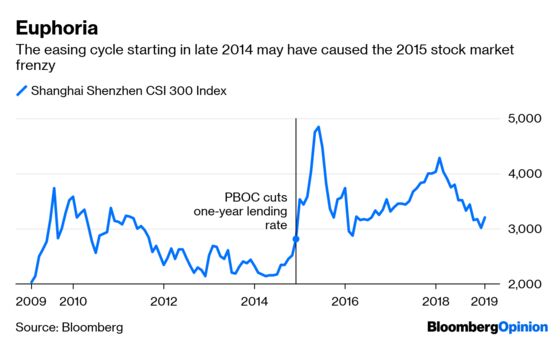

Whether to cut the one-year rate has become a contentious topic at the central bank. The last reduction in late 2014 arguably propelled the following year’s stock frenzy, which eventually led to a spectacular bust.

An interest-rate cut won’t help unblock the credit pipeline for private businesses, and that’s the thornier challenge for China’s policy makers. Capitalism loves the rich and shuns the poor, and that’s a natural phenomenon, as the central bank researchers ruefully noted.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.