OPEC+ Needs to Keep Its Covid-19 Mask On a Bit Longer

Despite the apparent dissent in the ranks during the weekend, OPEC+ has no choice but to stay its hand on raising production.

(Bloomberg Opinion) -- At the best of times, OPEC’s management of the oil market is like flying a plane wearing boxing gloves. In recent years, more pilots have crowded into the cockpit. Then, in 2020, one of the wings fell off as Covid-19 ravaged oil demand.

All of which means, despite the apparent dissent in the ranks during the weekend, OPEC+ has no choice but to stay its hand on raising production. To recap, the issue on the table at the conclave kicking off Monday in Vienna is whether to unwind soon an additional 1.9 million barrels a day of the deep supply cuts agreed (with much arm-twisting) in the spring. The idea at the time was to taper the cuts as the scourge of Covid-19 passed and oil demand rebounded.

Nothing is ever that clear cut in the oil market, and that counts for double when a pandemic is involved. The recent rally in oil futures got underway earlier this month with the first announcement of promising preliminary trial results for a vaccine. Further successes on this front have only bolstered confidence on the part of many that Covid-19 will be under control soon.

Yet for OPEC+, the decision on what to do with its supply cuts is a bit like the decision faced by many on what do with masks, family gatherings and so forth. Everyone is tired of restrictions and can see the sunlit uplands of mass vaccination on the horizon. But we aren’t there yet, and the relentless rise in cases and deaths in the U.S. and Europe are warning us to keep up the regimen of 2020 for just a few months longer. If we don’t — as may well have happened with U.S. travel over Thanksgiving — the valley before we reach those uplands is likely to be frighteningly deep.

Similarly, OPEC+ has good reasons to be optimistic that demand will recover next year as people begin to move around more freely again. Yet a false sense of security could wreak havoc on the oil price, and member countries’ finances, before recovery takes hold. In simple terms, the current Brent crude price of about $48 a barrel implies OPEC+ monthly revenue of about $50 billion (using October production figures). The price need drop by only 5% — taking it back to where it was less than two weeks ago — to wipe out the gain from adding back 1.9 million barrels a day.

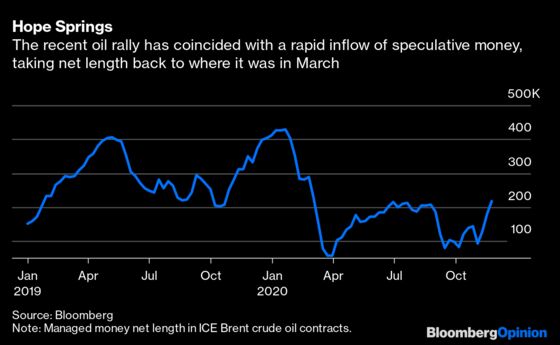

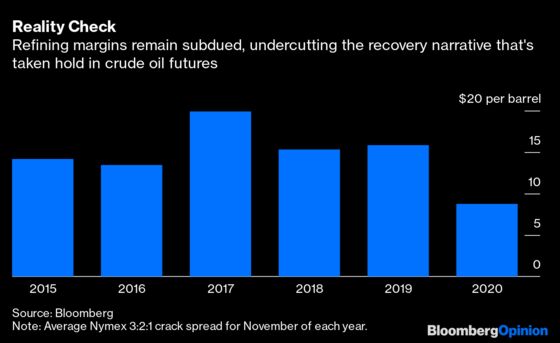

Two charts suggest the optimistic camp is on thin ice:

The November rally has coincided with a big increase in speculative length in Brent futures as hedge funds bet on a vaccine-led recovery and, implicitly, OPEC+ taking the strain until then. In the meantime, refining margins remain dismal; benchmark Nymex 3:2:1 cracks have averaged about $8.75 a barrel in November, about half the average for the past five years. That suggests that, for all the renewed traffic jams in Asia and expectations for a jet-fueled 2021 juicing futures, the physical market is not there yet.

As with the population at large, some OPEC+ members are better positioned to stick with supply cuts than others. This has long been the case for a club lumping together haves, have-nots and have-nothings, but the especially harsh test of Covid-19 has strained the bonds even further. Think of Saudi Arabia as a highly-paid remote worker riding out the storm with relative ease and, say, Nigeria as a worker at a meat-plant home-schooling 10 children.

This disparity — along with dangerous dependence on oil rents for many members — is the group’s underlying chronic condition. On that front, the United Arab Emirates’ recent musings about leaving are especially interesting. The UAE is one of OPEC’s “haves,” but, as existential things like peak oil demand come closer, the wisdom of leaving oil in the ground to help shore up the group’s sick men is ever more questionable. This motley group has struggled to impose order on the oil market for much of the century so far. It is hard to imagine it deftly managing the challenges of the energy transition.

Still, that’s a topic for another day and future meetings. Right now, OPEC+ must do what so many others are doing: Keep its mask on and hopes alive — but in check.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.