(Bloomberg Opinion) -- We’ve all done that mortifying thing where you build up a story too much and the Best Anecdote Ever fails to deliver. Well, OPEC not only did that on Thursday, it doubled down. After one of the longest meetings in years, the oil exporters’ group emerged without an agreement on supply cuts. It now gets another chance to wow the market on Friday, after a bigger meeting including non-OPEC partners such as Russia.

With the oil market already requiring quite the wow factor heading into the first meeting, this kicking of the can by 24 hours means one thing: OPEC’s gonna need a bigger wow. The catch? Even if it pulls that off, that would ultimately work against it.

The recent slide in oil prices demands that OPEC and friends take barrels off the market. Increased production from Saudi Arabia and Russia ran into U.S. waivers on Iran sanctions and growing concerns about trade, economic growth and, thereby, oil demand. Meanwhile, the Permian basin keeps doing its best impression of a perpetual pumping machine. On OPEC’s own projections, taken from its latest monthly report, a supply deficit of about 40,000 barrels a day this year was about to flip to a surplus of almost 1.5 million barrels a day in 2019, much of it front-loaded.

There was speculation OPEC would agree to cut 1 million barrels a day, using that to persuade Russia, Mexico, Oman and others to also cut. Yet that would imply the non-OPEC partners having to match the cuts they pledged two years ago – and actually stick to them – just to get close to balancing the market (and assuming Iranian sanctions bite harder). Given that for some countries, such as Mexico, natural decline was marketed as discipline, and Russia’s apparent ambivalence about higher oil prices, even this seems a tall order.

Such math may explain why it was so hard to agree on a public position Thursday and also why so much may now rest on persuading partners – read: Russia – to salvage something on Friday. Whatever the exact machinations, it reinforces the sense that the wheels are coming off.

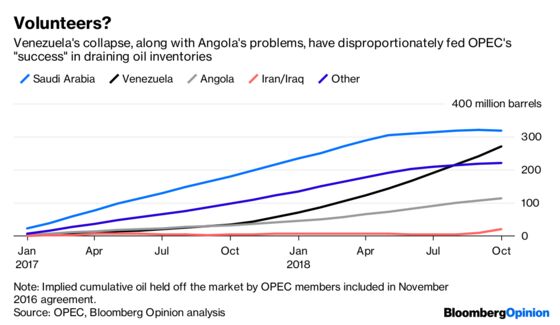

The chart below captures the ramshackle nature of it all. Through the end of October, the original OPEC members bound by the cuts agreed in late 2016 have held about 940 million barrels off the market, or around 1.4 million barrels a day, more than was pledged. But look at how they got there:

Remarkably, 40 percent of the cuts have come from just two countries, Venezuela and Angola, more than Saudi Arabia, even though the latter’s output in late 2016 was almost triple their combined total. A huge chunk of the “discipline” shown to date is really just collapse.

As Qatar’s decision to quit OPEC altogether demonstrated, the organization is increasingly a two-country show, Saudi Arabia and non-member Russia. And they are trying to herd a motley collection of smaller producers while simultaneously placating the U.S. president and figuring out how to co-exist with that country’s seemingly irrepressible exploration and production sector. Yet even success on this front carries the cost of encouraging higher production from competitors, especially in North America. Rather than OPEC-plus, it all looks more like OPEC-divided.

Thursday’s extended non-event came on a day when stock markets around the world were also deep in the red again. As of now, OPEC’s math still includes growth in oil demand next year of 1.2 million barrels a day. Even if an agreement emerges on Friday, it is worth contemplating whether this organization could survive the next recession, whenever it comes.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.