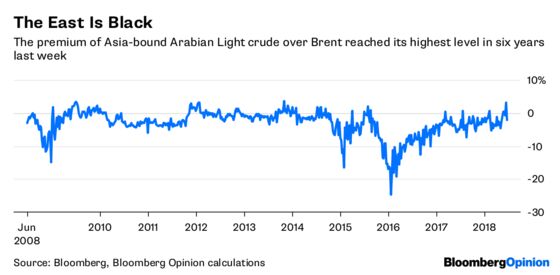

(Bloomberg Opinion) -- Here’s an indicator of what’s been driving the demand side of the oil market of late: Cargoes of Saudi Arabia’s main Arabian Light crude bound for Asia, which tend to be priced at a discount to Brent, last week reached their biggest premium to the European benchmark in six years.

The reason for this isn’t hard to discern. Gulf producers like the OPEC members meeting in Vienna on Friday can choose to send their cargoes east or west, and will raise prices to whichever market seems most likely to tolerate higher costs. In recent months, that’s been Asia, where (as we’ve written) demand has been surging. Should this week’s OPEC meeting end up with a boost to output driven by Saudi production, as many analysts expect, watch out for that dynamic reversing.

To see why, it’s worth considering the many flavors of oil out there.

The Brent and West Texas Intermediate benchmarks are sweet, light crude, with relatively low proportions of sulfur and high shares of the short-chained hydrocarbons that go to make up most transport fuels. They tend to be priced at a premium because they’re easy for refineries to process.

Arabian Light is different. Despite its name, it would be counted a medium sour grade under most definitions of the term. Its API gravity — a measure of the proportion of long-chain heavy hydrocarbons — is 32.5, compared with the lighter 35-to-45 ranges for WTI and Brent. Indeed, it’s more or less interchangeable with the new medium sour futures that the Shanghai Futures Exchange is hoping to establish as a rival benchmark to the New York and London contracts.

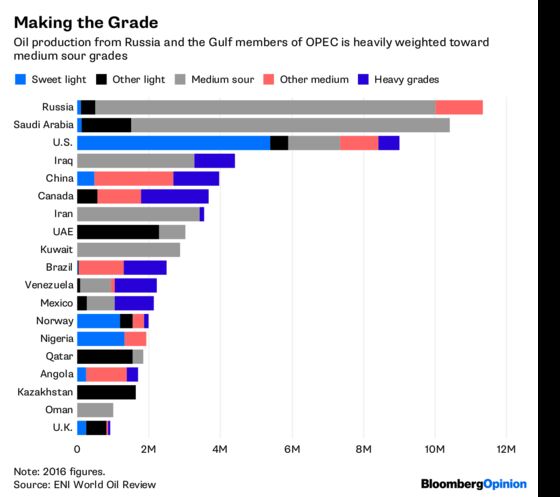

Medium sour grades are also the major ones produced by the Organization of Petroleum Exporting Countries and its allies, comprising about 85 percent of output by Russia and Saudi Arabia, 75 percent from Iraq, and almost all the production from Iran and Kuwait in 2016, according to Eni SpA. Only in the U.S., the North Sea and Nigeria among major producers do sweet, light grades account for more than a sliver of the total.

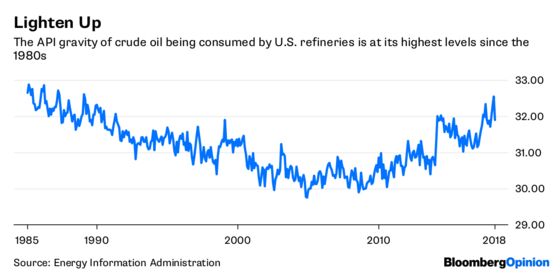

Oil refineries tend to be picky about the balance of crudes they process and can’t easily reconfigure to take a different slate of hydrocarbons. Thanks to the flood of light grades from the U.S. onshore shale boom and the declining supply of heavy Venezuelan crude, the average gravity of oil being consumed by American refiners is now the highest it’s been since the 1980s. With refineries running flat-out processing onshore North American oil, they’re likely to be a less attractive destination for increased Opec output than markets in Asia.

As my colleague Julian Lee has written, the vast majority of the spare capacity within Opec and its allies sits with Saudi Arabia, Russia, and other Gulf countries — producers, in other words, that are weighted toward medium sour. As a result, one way of looking at the mooted 600,000 barrel-a-day increase is a load of supply being dumped on the Shanghai and Arabian Light markets, with a more indirect effect on Brent and WTI. That should reduce those premiums for Asian crude to more normal levels, and even bring back the habitual discount.

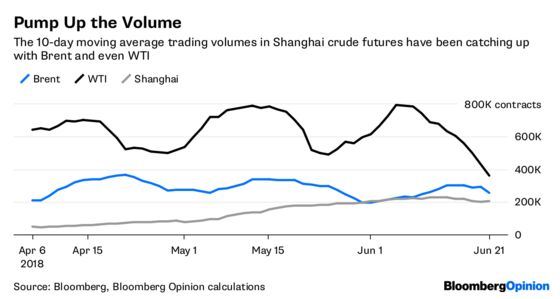

For the Shanghai exchange, this will prove an early test of the new medium sour contract launched in March. While volumes have been healthy — occasionally even overtaking those of Brent — and bid-ask spreads indicate a reasonably liquid market, the daily peak in trading still seems to be in the late afternoon GMT, when U.S. and European traders are battling it out but their Chinese counterparts are mostly asleep.

This indicates the global oil market is still being steered from the North Atlantic, with Shanghai futures ultimately following Arabian Light and by extension Brent and WTI, rather than vice versa. Only when that changes will China have a home-grown oil benchmark worthy of the name.

To contact the editor responsible for this story: Paul Sillitoe at psillitoe@bloomberg.net

©2018 Bloomberg L.P.