Libor, the $370 Trillion Zombie That the Watchdogs Can’t Kill

(Bloomberg Opinion) -- The tainted suite of interest rates known as the London Interbank Offered Rates is scheduled to be phased out by the end of 2021. But the benchmark for global borrowing costs is proving tricky to replace. It’s time for the regulators to rethink killing off what was once dubbed “the world’s most important number” until the rigging scandals besmirched Libor’s reputation.

The main markets have nominated their official successors to Libor. In dollars, the chosen benchmark is the Secured Overnight Financing Rate. For U.K. markets, it’s the Sterling Overnight Interbank Average Rate. And in the euro zone, the European Central Bank’s forthcoming Euro Short-Term Rate was selected.

But the resulting alphabet spaghetti has proved unpalatable, with SOFR and SONIA struggling to gain traction. Of the $54 trillion of interest-rate derivatives traded in the third quarter, just 3.3 percent were tied to Libor alternatives, according to the International Swaps and Derivatives Association.

In November, the Bank of England calculated that the share of the notional cleared sterling swap market that uses Sonia as its reference rate was 18 percent, up from 11 percent in July 2017. That’s a pathetic growth rate, particularly given that the benchmark, which is based on overnight transactions in the wholesale market with a minimum value of 25 million pounds ($31.7 million), has been in existence since 1997. The Financial Conduct Authority has been bludgeoning banks since the middle of the year to make the transition. Inertia is hampering its efforts.

Earlier this month, the European Parliament backed the finance industry’s calls for a two-year reprieve for the existing euro benchmarks, Euribor and Eonia, until the end of 2021. About 22 trillion euros ($25 trillion) of derivative contracts are tied to Eonia; the ECB doesn’t plan to start publishing its new rate until October, which made the original deadline of the end of 2019 somewhat unfeasible.

FCA Chief Executive Officer Andrew Bailey, one of the chief architects of the benchmark revolution, estimates that about a third of the $170 trillion of swap contracts that still rely on Libor for their prices won’t mature until after the benchmark is scheduled to perish. More than $500 billion of bonds that reference Libor will still exist after the benchmark rates are scheduled to end, the Financial Times reported in October, citing figures compiled by the Linklaters law firm.

Those intimately affected by the coming changeover are worried. In November, Goldman Sachs Group Inc. Treasurer Beth Hammack said shifting to new benchmarks would be “a really painful transition” in part because “markets are really creatures of habit.” The U.S. Government Finance Officers Association said in September that ousting Libor poses risks to about $44 billion of floating-rate municipal bonds issued by states and cities.

But it’s not just the world of high finance that relies on Libor. U.K. homeowners have more than 5.1 billion pounds of mortgages that reference Libor, a tenfold increase since 2014, according to rating company DBRS Ltd. The U.S. Alternative Reference Rates Committee said in March that $1.2 trillion of U.S. retail mortgages are estimated to be tied to Libor.

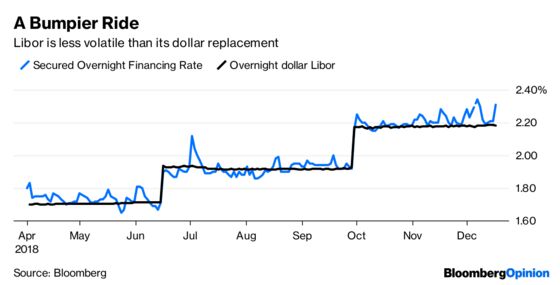

SOFR, the U.S. replacement that’s based on repurchase agreements in the Treasury market, has had a particularly bumpy start. After its launch in April, the New York Federal Reserve announced that bad data had been included in its calculations.

The new rate, moreover, is more volatile than Libor, as the chart above shows, and seems to spike at month end. On average, it’s been set about 2 basis points higher than Libor, with the gap reaching a high of more than 18 basis points at the end of June.

Libor is so enmeshed in finance that market participants are understandably loath to unpick the web of contracts that rely on its matrix of interest rates. There’s a clear preference for maintaining the status quo. So improving Libor rather than abolishing it is starting to look like the lesser of two evils.

Harnessing the wisdom of a bigger crowd, rather than relying on the best-guesses of a bunch of traders, would reduce Libor’s vulnerability to manipulation. Expanding the panels of market folk that submit their best estimate of how much money should cost for various maturities to include corporate treasurers would enhance its credibility. Combining the insights of companies with the real rates they pay in the commercial paper market would make calculating the rates more complicated, but also make them more reflective of real-world borrowing costs — which is, after all, the primary goal of a benchmark.

Given the opprobrium that’s been heaped on Libor — not to mention the billions of dollars in fines paid by the banks that looked away while their traders submitted distorted rates for personal profit — you can sympathize with the regulatory reluctance to allow it to underpin an estimated $370 trillion of securities of various flavors. But this is a case where evolution is preferable to revolution. Long live Libor.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2018 Bloomberg L.P.