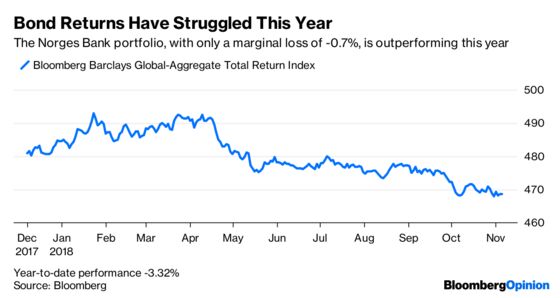

Norway's $1 Trillion Wealth Fund Has a First-World Problem

(Bloomberg Opinion) -- It’s the very definition of a first-world problem, but Norway’s $1 trillion sovereign wealth fund is wrestling with whether to make its investment portfolio less diverse. It’s a subject that cuts to the heart of the “active manager versus passive index” debate.

As part of a long-running review, which will lift the fund’s equity allocation to 70 percent, the Norwegian government appointed a panel of outside experts to advise on how the bond portion should be invested.

It’s a surprisingly controversial question. In September last year, the fund’s own managers proposed reining in the scope of its debt investments, arguing that it has enough currency, emerging market and corporate risk in the much bigger equity portfolio. As such, they argued, it shouldn’t carry the same exposure in bonds, which are often far less liquid.

The panel of experts wholly disagrees. It said this week that the current broad investment in 23 currencies and wide-ranging corporate credit exposure helps “minimize risk and maximize investment capacity.” According to their argument, that’s because it mimics the standard approach in the global fixed-income universe. In effect, they’re saying it’s not humanly possible to get sector allocation decisions right consistently, so far better to stick with the herd.

The debate is fascinating because it boils down to quite what a fixed-income fund should be for, and doubly so because we’re talking about the world’s biggest sovereign wealth fund here. Just how much do you want to tie the hands of your fund managers, especially when they’re eager to go their own way?

My sympathies lie with the managers. The steady rise in U.S. interest rates, and the concurrent reduction in the Federal Reserve’s balance sheet, is already upsetting the emerging market apple-cart as the turmoil in Argentina and Turkey has illustrated so clearly. Meanwhile, the decade-long recovery from the financial crisis is getting long in the tooth, and any economic downturn would no doubt push corporate credit spreads wider relative to government bonds.

Instead of a global remit, which would have to include corporate and emerging market junk bonds, the fund would rather stick largely to government debt out to 10 years in maturity and just in dollars, euros and sterling. To augment that, it wants the flexibility to make “strategic investments” where it sees bond market opportunities and to adopt systematic strategies to take non-vanilla risk. But that’s not the kind of active management the outside experts say is suitable. Sticking to an index should remain the top priority, they say, even if it doubles up on currency and corporate risks.

It’s hard to feel entirely confident with that approach. Liquidity is always most prized when it vanishes, and slavishly following an index isn’t always a good thing when there are obvious duds to avoid — particularly in a rising rate environment. Logically, it makes sense to reduce the range of exposure in bonds where returns are limited, when the same risks are being taken already in a much larger equity portfolio where upside is theoretically greater.

Of course, a multi-currency bond fund’s return is driven much more by its currency exposure than the bond yield. Yet with the QE party coming to an end and emerging markets in turmoil, this isn’t the guarantee that it once was. When your own fund suggests dialing down the fixed-income risk, you ought to listen.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.