(Bloomberg Opinion) -- Talk about shutting the stable door after the horse has bolted.

The looming insolvency of once-mighty commodities trader Noble Group Ltd. is an overdue reckoning for a company that has long sailed close to the wind.

More than that, though, it’s a black mark against the city-state where it’s been listed since 1997: Singapore. Noble has spent the past year squirming through an attempted restructuring to keep it from bankruptcy, hampered by its money-losing operating business and years of squandered trust.

Now, just yards from the finish line, Singaporean regulators are blocking its relisting, a move that could force the company into bankruptcy. They’ve previously said they’re looking at accounting issues between 2012 and 2016. That looks strikingly similar to the arguments of Arnaud Vagner, a former employee who blew the whistle on the company with a 2015 report under the name Iceberg Research that highlighted the company’s strange accounting of hard-to-value contracts.

Vagner’s arguments now look prophetic. That begs the question: Why did Singapore allow Noble to get away with it for so long? One explanation comes from looking at the nature of the rest of the exchange.

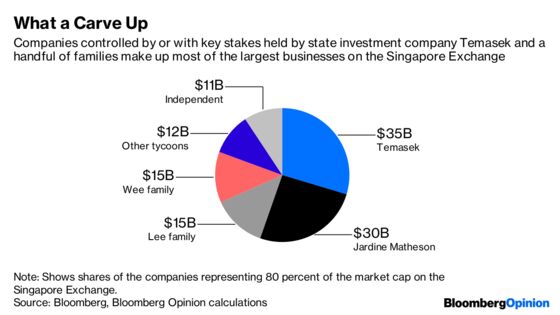

Go through the 45 companies that comprise about 80 percent of the market capitalization on the Singapore exchange and one fact immediately jumps out: All but four are either controlled or have significant ownership stakes held by a small number of families and the government.

More than half of that market capitalization belongs to government-owned investment company Temasek Holdings Pte. and Jardine Matheson Holdings Ltd., a Hong Kong-British trading company whose origins date back to the 19th-century Opium Wars. Another quarter has significant control from the Lee and Wee families, founders of Oversea-Chinese Banking Corp. and United Overseas Bank Ltd. A further 10 percent goes to other Asian tycoons, such as Robert Kuok, Lim Kok Thay, and Charoen Sirivadhanabhakdi.

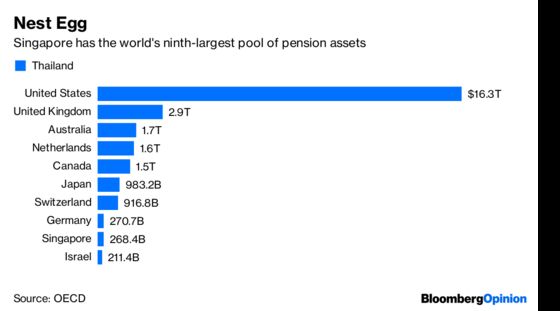

For a country that cherishes its self-image as a meritocracy, a market that’s sewn up between a few family dynasties and the state isn’t a good look. It’s also a long-term worry given that the country has one of the world’s largest pension pools and a fast-aging population. It’s hard to be confident that companies will do what’s best for all shareholders in the long term when owner-managers are so often in charge.

Given those concerns, it’s remarkable how ham-fisted Singapore has been in attracting listings that could turn its exchange into more of a genuine capital market. S-chips — the Singapore-listed Chinese businesses that were in vogue during the 2000s — have all but cleared off now after a string of scandals that will be familiar to any followers of the wilder fringes of China’s equity markets. Saudi Arabian Oil Co. was also touted for a potential Singapore listing — a deal that wouldn’t have done a lot to burnish the bourse’s corporate governance image, and one that now looks to be more or less off the table anyway.

And then there’s Noble. It’s ironic that a market looking to diversify away from its dominance by Jardine Matheson should have seen its salvation in a company whose buccaneering founder named it after “Noble House,” the James Clavell novel based on the founding of Jardine. Still, at its peak in 2011 it was worth more than S$14 billion ($10 billion), enough to make it one of the biggest stocks on the exchange, and its only tycoons were self-made.

The experience should be a cautionary one for Singapore. With a huge pool of retirement funds and strong marks for corruption and ease of doing business, the city-state has many of the virtues needed to attract high-quality listings — but its willingness to let its standards slide to tempt a Noble or a Saudi Aramco has hindered, rather than helped. If Singapore wants to stop itself being overtaken by equity markets in Indonesia, or Malaysia, or falling further behind Thailand, it needs to build on its virtues — not abandon them.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2018 Bloomberg L.P.