(Bloomberg Opinion) -- We’re eight days away from the official Brexit deadline and things aren’t going well. Westminster is in disarray, Theresa May’s deal is in tatters and EU leaders aren’t sure of how to delay the shambles, if at all.

With politicians unable to patch things up, European and U.K. financial supervisors have been among the few adults in the room. They’re made reassuring moves to calm investors in the event of a no-deal Brexit, promising to preserve continuity in critical areas of the financial system such as the $400 trillion derivatives market. A truce of sorts has emerged.

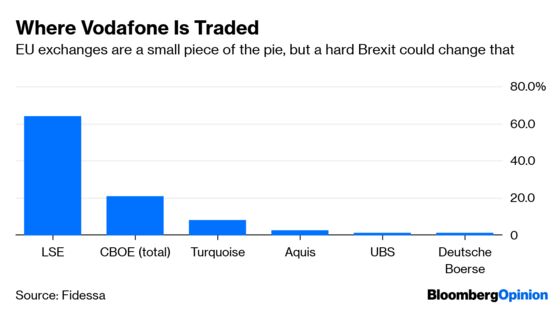

But the toxic political mood is starting to infect regulators, too. This week, EU financial markets watchdog ESMA quietly lobbed a grenade by outlining the impact on stock-market trading of a no-deal Brexit (which technically could still happen on March 29). It provided a list of 6,000 liquid stocks that would have to be traded on EU soil to comply with its oversight rules. Some 14 of those were U.K.-listed shares, including FTSE 100 giants Vodafone Group Plc, BP Plc and GlaxoSmithKline Plc. So any regulated investment firm in the EU wanting to buy a chunk of Vodafone — which after a no-deal would be based outside the EU — would have to make sure the trade happened on the continent. In short: a hard border for the stock market.

The disruption could be huge once you take into account potential tit-for-tat responses. Britain’s Financial Conduct Authority has warned ESMA that it, too, would have to draw up trading rules in a no-deal scenario, and that there might be a “large degree of overlap” with the ESMA list.

Imagine investment firms in the U.K. being told that thousands of liquid European stocks must be traded on British soil, including index behemoths such as Total SA or Siemens AG. It would be like yelling “fire” in a crowded theater: Liquidity in these shares would be hit overnight. The headache of splitting up trading desks between London and Paris or Frankfurt (or wherever) might seem less bother than giving up entirely on some stocks. The end loser would be the consumer — retail investors and pension funds — paying the extra cost of this dual regulation and less market activity, according to David Berney of Ergo Consultancy.

Any two-way split would especially hit the approximately 230 European stocks that have a roughly 50-50 share in trading volumes between U.K. and the continent, according to trade technology firm Fidessa. It reckons these stocks accounted for 2 trillion euros of trading in 2017.

It’s hard to see what the Europeans would gain here over the long run. Any dream of grabbing swathes of stock-market trading would probably be short-lived. If anything, the U.S. would suddenly look like the better option. A single, deep pool of liquidity for companies looking to list sounds better than two shallow ones.

Avoiding this chaotic outcome relies on pragmatism, at a time when there isn’t much of it on show. The EU could rule that the U.K. is an equivalent country in regulatory terms, even after a hard Brexit. That’s a purely political decision, and would no doubt be easier should Westminster sign up to Prime Minister Theresa May’s Brexit deal before time runs out. If that were to happen, all of this uncertainty would evaporate, but as things stand you wouldn’t fancy her chances. Her decision to blame lawmakers for her predicament hasn’t gone down very well in the House of Commons.

Either way, investors have been given a glimpse of the regulatory and political tensions that may be about to fracture the world’s biggest single market. It’s not a pretty picture.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Lionel Laurent is a Bloomberg Opinion columnist covering Brussels. He previously worked at Reuters and Forbes.

©2019 Bloomberg L.P.