Netflix, Welcome to Ratings Hell

With last quarter’s weak showing, the video-streaming service gets to experience what the media giants went through.

(Bloomberg Opinion) -- The TV-network giants went through ratings hell. It’s time for Netflix’s own version of that.

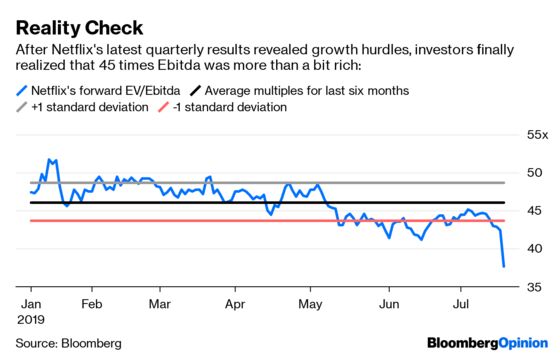

After the market closed on Wednesday, Netflix Inc. reported that it lost 126,000 U.S. streaming customers during the second quarter, which appears to be the first time it’s ever done so. Global membership growth was also well short of management’s own expectations, with 2.7 million net sign-ups versus an anticipated 5 million. The company blamed its uninspiring results on subscription price increases and a less-enticing mix of movies and TV series. While it signaled that “more typical growth” and better content is in store, shares of Netflix sold off 12%, erasing $17 billion from its market value.

This marks a turning point in how investors view the future of Netflix vis-a-vis its biggest emerging threats, Walt Disney Co. and AT&T Inc.

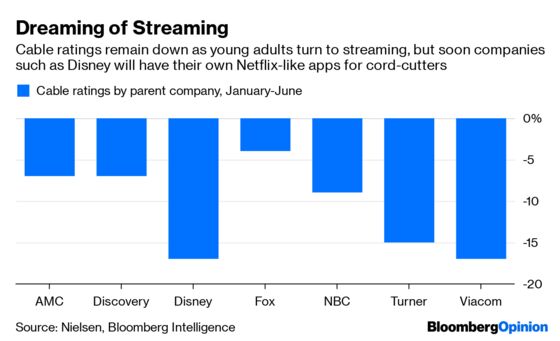

In recent years, the popularity of Netflix has been a chief reason for the accelerated drop in cable subscriptions and viewers tuning out traditional live TV. As investors were entranced by the video-streaming app’s rapid growth and awarded the company an absurdly rich valuation, companies such as Disney and Time Warner (now called WarnerMedia, a unit of AT&T) were punished by shareholders for their audience shrinkage.

Those media giants’ audiences are still shrinking (see next chart), and their businesses still rely on TV commercials and cable fees to drive profit. But they have managed to change the narrative so that more attention is paid to their own streaming opportunities. Nov. 12 is the launch date for Disney+, which Disney plans to bundle with ESPN+ and Hulu for fans who want all three services. Shortly thereafter, AT&T’s WarnerMedia will introduce HBO Max, a souped-up version of the HBO app that will contain Turner network programs and Warner Bros. films. Given the relatively low price of Disney+ at $6.99 a month and the quality of Disney and HBO/Warner content, both products have the potential to lure a considerable number of streamers away from Netflix.

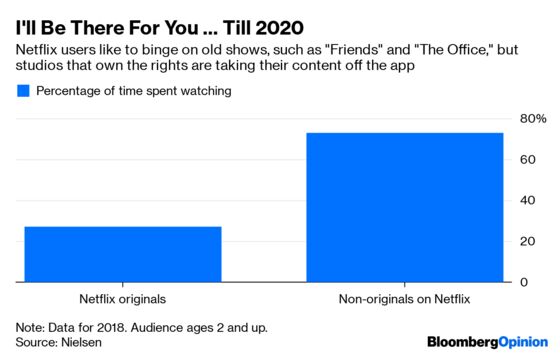

This means Netflix investors will become even more obsessed with its quarterly subscriber count. They’ll also want more real data as far as how many people are watching Netflix’s costly originals – much in the way investors have picked apart the traditional media companies’ Nielsen viewership ratings. By now you’ve heard that “Friends” is moving to AT&T’s HBO Max next year, and that Comcast Corp.’s NBCUniversal is reclaiming “The Office” in 2021. Those are the most-watched shows on Netflix, so their expiration dates create a sense of foreboding.

As my colleague Shira Ovide alluded to Wednesday, Netflix may be drifting too far from what it made it so attractive in the first place: being a constant bazaar of binge-able video entertainment. By blaming its own content slate for last quarter’s weak showing, Netflix is saying that it’s not all that different from HBO, which is dependent on a select few hit programs and goes through lulls when there aren’t new episodes. I’ve written that Netflix has the benefit of already being the “base” streaming service for many people, but that could change if Netflix becomes less of a one-stop shop and other services seem to offer more bang for your buck.

Disney+ launch day is just four months away. And the closer we get to D-Day, the more skittish Netflix shareholders will be. Cable-network operators know all too well what that’s like.

Apple TV+ is also coming later this year to challenge Netflix.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tara Lachapelle is a Bloomberg Opinion columnist covering deals, Berkshire Hathaway Inc., media and telecommunications. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.