(Bloomberg Opinion) -- When President Bill Clinton had to scale back his ambitious fiscal stimulus plans in 1993 because he was told that bond investors would react negatively to the resulting increased debt and deficits, leading to higher borrowing costs across the economy, Democratic political adviser James Carville had this response:

“I used to think that if there was reincarnation, I wanted to come back as the president or the pope or as a .400 baseball hitter. But now I would like to come back as the bond market. You can intimidate everybody.”

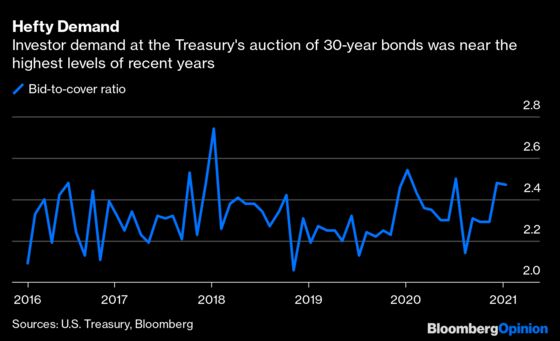

That may have been true then, but today no such worries should deter lawmakers as they debate whether to pass President-elect Joe Biden’s $1.9 trillion economic relief plan or some scaled-down version. For proof, look to Wednesday’s auction by the government of $24 billion in 30-year U.S. Treasury bonds. Investors placed bids for an impressive 2.47 times the amount of bonds offered, above last year’s average of 2.36 for that maturity and the third-highest level since last January. (The bonds are sold monthly).

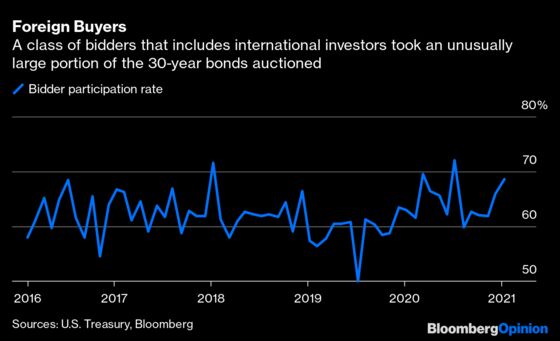

Not only that, but a group referred to as indirect bidders — which includes foreign central banks and institutions — bought 68.6% of the bonds offered, above last year’s average of 65.9% and also the third-highest level since last January. Showing the auction was no fluke, the government’s sale of $58 billion of three-year notes and $38 billion of 10-year notes generated similar levels of demand.

The results are remarkable for a few reasons. For one, they came at a time of historic political upheaval, with the House of Representatives voting to impeach President Donald Trump for inciting an insurrection. Evidence that investors were penalizing the U.S. for a dysfunctional government would have surely found its way into the auctions, but it didn’t happen. On top of that, everyone knew Biden’s relief package would be in the trillions of dollars, resulting in even more borrowing in the months ahead, and yet buyers flocked to the debt offering anyway.

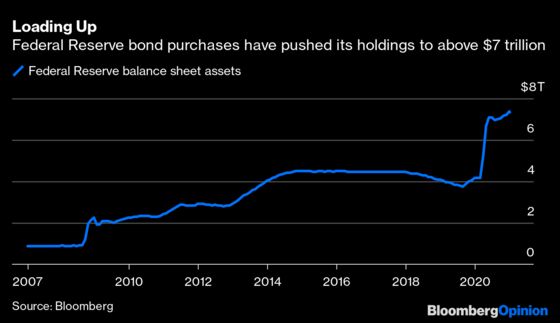

Of course, what Clinton didn’t have was a cooperative central bank. The Federal Reserve’s bond purchases have increased its balance sheet assets by about $3 trillion over the last 12 months to $7.33 trillion, and by about $6.5 trillion since before the Great Financial Crisis hit in 2008. And the Fed has no plans to slow down, buying about $120 billion of bonds every month.

“Now is not the time to be talking about an exit” from asset purchases, Fed Chair Jerome Powell said Thursday during a virtual discussion of monetary policy. “A lesson of the global financial crisis is, be careful not to exit too early.”

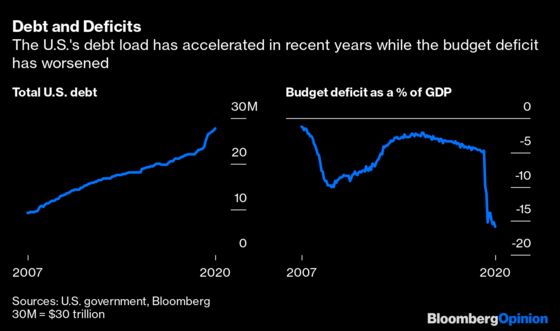

The U.S. has already done a lot of borrowing in recent years to make up for the loss of revenue from the Trump administration’s tax cuts and last year’s pandemic relief packages. Total debt soared by $4.55 trillion in 2020 alone to $27.7 trillion, according to the Treasury Department. The 19.6% increase was the most since at least before 1974, data compiled by Bloomberg show. The budget deficit has blown out to some 16% of gross domestic product from 3% at the end of the Obama administration.

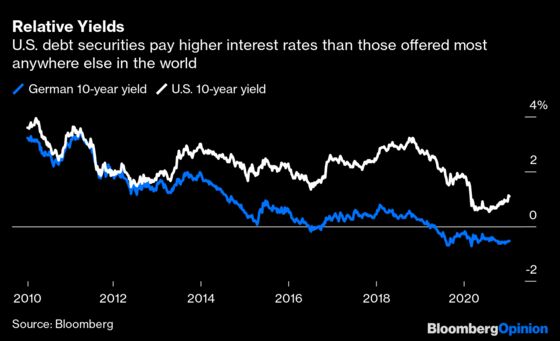

Debt and deficits may matter again some day, but at the moment there are few realistic alternatives to U.S. government bonds for investors. Not only does the U.S. have the biggest, deepest and most liquid debt markets in the world, the interest rates offered are actually pretty juicy on a relative basis. Yields on U.S. Treasury securities average about 0.7 percentage point more than government debt securities elsewhere, according to the ICE Bank of America bond indexes. A decade ago, they yielded about 1 percentage point less on average.

The bond auctions were also notable in that they should temper concern that all the fiscal relief coming, when combined with the trillions of dollars pumped into the economy last year, will spark much faster inflation. Nothing scares bond investors more than the prospect of faster inflation, and they watch it closely. That’s because inflation erodes the value of bonds’ fixed-interest payments, making the securities worth much less. So if bond investors really believed inflation was poised to accelerate, the last thing they would do is pile into 30-year Treasuries.

There’s little doubt that in the days and weeks ahead some lawmakers will object to the size of Biden’s relief plan out of concern that it will ruin the country financially. Perhaps such arguments would carry some weight in normal times, but these are not normal times, and bond investors are clearly saying more spending to support the economy is the right course of action.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is the Executive Editor for Bloomberg Opinion. He is the former global Executive Editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2021 Bloomberg L.P.