(Bloomberg Opinion) -- Christmas trading updates from Britain's grocers began with a value mince pie rather than a luxury yule log on Tuesday.

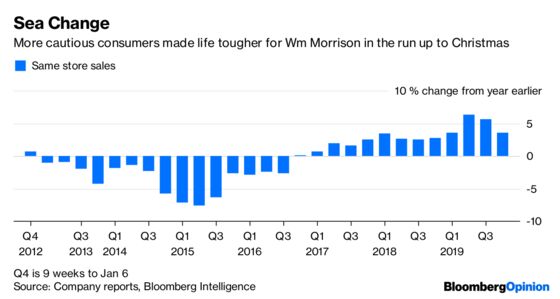

Wm Morrison Supermarkets Plc reported total like-for-like sales growth of 3.6 percent in the nine weeks to Jan. 6. The 0.6 percent increase in retail sales was better than expected. But it included a 0.4 percentage point contribution from online, so sales from stores were only marginally positive.

It’s worth remembering that Morrison is up against tough comparisons for the past two years. Although growth within its wholesale arm was below the consensus of expectations, that is still a relatively new business, so harder for the market to get a handle on.

Chief Executive Officer David Potts said there had been a change in consumer behavior in October and November. Customers became more cautious, with both price-sensitive and more affluent shoppers conscious of their spending in the run up to the holiday.

Overall, it's a decent performance, and the group’s strong management, innovation and financial strength mean it has a good starting point for battling against its bigger rivals.

As the smallest of Britain’s big four supermarkets, with its heartland in the north of England, it is at particular risk both from consumers tightening their belts and price competition from the U.K. arms of the German discounters, Aldi and Lidl.

The latter seems to be getting more intense – Kantar Worldpanel said they together recorded their highest ever Christmas market share in the 12 weeks to Dec. 30, at 12.8 percent.

Still, as a value-oriented supermarket, competing for cash-strapped shoppers plays to Morrison’s strengths.

The company has a strong balance sheet, in part because it owns about 85 percent of its stores. Its wholesale arm should eventually delivery a steady stream of revenue and profit.

That could come in handy if competition authorities force J Sainsbury and Asda to dispose of stores to win approval for their 7 billion pound ($9 billion) merger. Morrison will be one of the few groups able to pick up new locations.

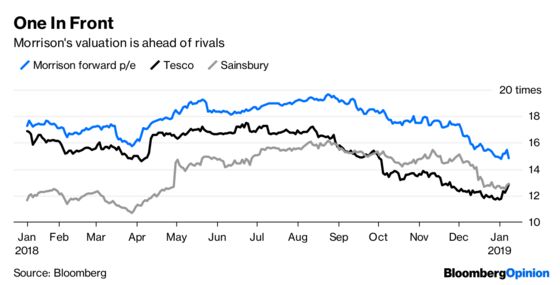

The shares are down more than 20 percent from their year's high in August. Even so, they still trade on a forward price earnings ratio of about 15 times, ahead of both Tesco Plc and J Sainsbury Plc.

The premium to Sainsbury is clearly deserved. It could be one of the Christmas losers, according to the Kantar data. And it also faces considerable uncertainty from regulators’ scrutiny of its acquisition of Asda.

But the big gap to Tesco could come under pressure. Britain's biggest supermarket also looks like it had a decent Christmas, thanks in part to a difficult one last year. And it has a good chance of achieving its target of a group operating margin of 3.5-4 percent in the year to February 2020.

Longtime grocer Potts likes to portray Morrison as the underdog scrapping for sales. With conditions set to get even tougher, he will need every bit of fight to stay ahead.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.