We're One Mistake Away From a Global Recession

The International Monetary Fund this week cut its forecast for global gross domestic product to 3% in 2019 and 3.4% next year.

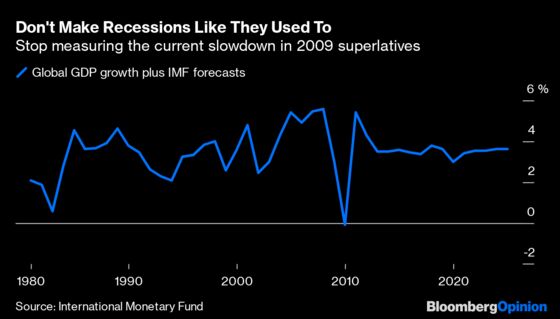

(Bloomberg Opinion) -- Here's the silver lining to slowing world growth: We are a long way from 2009, when the global economy contracted. The bad news is that this balancing act is looking increasingly shaky.

The International Monetary Fund this week cut its forecast for global gross domestic product to 3% in 2019 and 3.4% next year. That's the weakest outlook in a decade, and down slightly from the lender's projections in July. (The IMF views a pace of less than 2.5% a recession.) So while that’s not exactly rosy, comparing these numbers with the disaster of 2009, when GDP fell 0.1%, is very wide of the mark. The IMF also trimmed its outlook for China, which helped revive world growth after the past two slumps.

Another key difference with 2009 is monetary-policy coordination. Central banks have been easing “simultaneously,” IMF Chief Economist Gita Gopinath told reporters Tuesday in Washington. Without that stimulus, which is likely to increase, the lender reckons the trajectory of world growth would be 0.5% lower.

Back in 2007-2009, policy was disjointed at first. The Fed began cutting rates in the late summer of 2007 while the European Central Bank hiked just two months before Lehman Brothers Holdings Inc. collapsed. China only joined the effort toward the end of 2008. The Bank of Japan's main rate, meanwhile, had already been near zero for a decade.

In the current downdraft, global central banks have gotten in sync a lot more quickly. The People's Bank of China was out of the gate first, reducing reserve requirements for lending last year. The Fed's first cut of this cycle came in July, about six months after the central bank stopped hiking. The ECB followed fast by restarting its quantitative-easing program and lowering rates, and the BOJ — which has carried on buying bonds — has foreshadowed more moves to juice growth.

Australia’s response has also been instructive, especially because its economy has been on pedestal for fostering decades of expansion, as I wrote here. After two quick cuts this year, observers had thought the Reserve Bank would take a breather. Yet another reduction came quickly, with dovish signals to boot. The Bank of Korea signaled some reluctance to lower rates further after cutting again Wednesday, but we'll see how that plays out: Exports are tumbling and deflation is on the horizon.

All this points to the precarious nature of the global economy. Manufacturing is slumping, fiscal policy is patchy and an awful lot rides on the shoulders of consumers, whose spending is buttressed by low unemployment across major economies. The IMF's Gopinath warned that a policy mistake could easily push this expansion off the rails.

Measures to spur growth are always more effective when coordinated across jurisdictions. What we have now is the opposite: a deep reluctance to embrace multilateral policies, and trade prescriptions designed to unravel the links between economies instead of knitting them closer together. President Donald Trump and Liu He, China's vice premier, barely shook hands on the first phase of a trade accord before skeptics began picking it apart, with some justification.

In the context of 2009, this muddling-through economy is something to protect. All policy levers need to be working to nourish, not starve, it.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Daniel Moss is a Bloomberg Opinion columnist covering Asian economies. Previously he was executive editor of Bloomberg News for global economics, and has led teams in Asia, Europe and North America.

©2019 Bloomberg L.P.