Mnuchin Forgot to Check His Figures on Stock Volatility

(Bloomberg Opinion) -- U.S. Treasury Secretary Steven Mnuchin is concerned about market volatility.

So concerned, in fact, that he said in a roundtable interview at Bloomberg’s Washington office on Tuesday that he plans to ask the Financial Stability Oversight Council, which he oversees, to look into what’s causing the turbulence. His working hypothesis is that high-speed traders and the Volcker Rule are to blame.

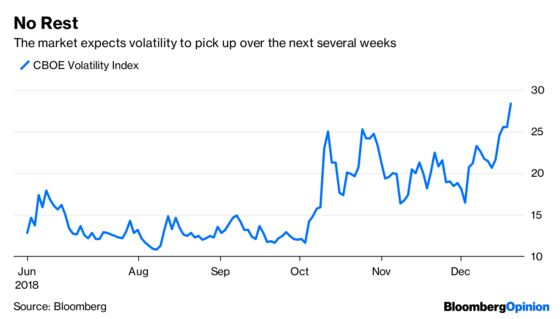

If Mnuchin was concerned on Tuesday, he must be spooked by now. The S&P 500 Index fell 1.5 percent on Wednesday and an additional 1.6 percent on Thursday. And the market expects more pain. The CBOE Volatility Index, or VIX, which measures expected volatility over the next 30 days, closed at 28.38 on Thursday, up 73 percent since Dec. 3 and 11 percent since Tuesday.

But here’s the reality: There’s nothing amiss about the recent volatility, and if anything, volatility has been lower than usual in recent years, not higher.

High-speed trading is a popular bogeyman for a variety of market ills, but there’s no reason to believe that higher volatility is one. High-frequency trading represented a small portion of total stock trades in the U.S. before the mid-2000s. The 30-day trailing volatility for the S&P 500, as measured by annualized standard deviation, averaged 15.3 percent from 1928 to 2004. Since then, volatility has averaged — wait for it — 15.3 percent.

Similarly, the Volcker Rule, which generally prohibits banks from trading for their own accounts or owning hedge funds and private equity funds, hasn’t had any discernable impact on volatility, either. Before the rule went into effect in April 2014, the 30-day trailing volatility for the S&P 500 averaged 15.5 percent. Since then, it has averaged 11.7 percent.

And it doesn’t matter what yardstick you use. The volatility numbers before and after high-speed trading and the Volcker Rule are nearly identical when looking at one-, three-, six- or 12-month trailing volatility.

Nor is there anything unprecedented about the market’s recent gyrations. The 30-day trailing volatility for the S&P 500 is 22.2 percent through Thursday. Since 1928, it’s been as high or higher 15 percent of the time.

It’s even less unusual when measured over longer periods. The three-month trailing volatility of 20.4 percent has been as high or higher 18 percent of the time. And the six- and 12-month volatilities have been as high or higher 37 percent and 35 percent of the time, respectively.

It’s also worth noting that there’s nothing worrisome about the fact that “a normal trading day now is a 500-point range,” as Mnuchin complained. Sure, when the Dow Jones Industrial Average was at 10,000, a 5 percent move might be distressing. But when the Dow is at 26,000, as it was just a month ago, a 500-point move is a mere 2 percent. That’s well within the market’s normal range.

The fact is, the market swoons occasionally. It can’t help, however, that the White House is fighting with the U.S.’s trading partners, particularly when the big multinational companies that dominate the Dow and S&P 500 generate much of their revenue overseas and investors are counting on those revenues to justify lofty stock prices.

It may or may not be possible to quiet the market, as Mnuchin apparently wants to do, but calling the FSOC is surely the wrong place to start.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nir Kaissar is a Bloomberg Opinion columnist covering the markets. He is the founder of Unison Advisors, an asset management firm. He has worked as a lawyer at Sullivan & Cromwell and a consultant at Ernst & Young.

©2018 Bloomberg L.P.