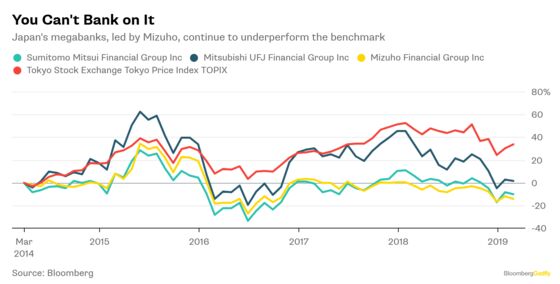

(Bloomberg Opinion) -- What is it about Japanese banks and overseas misadventures?

Mizuho Financial Group Inc. last week reported about 150 billion yen ($1.35 billion) of valuation losses on its foreign-bonds portfolio, while Mitsubishi UFJ Financial Group Inc.’s foray into U.S. high-yield debt underwriting went awry. Less than two months ago, Nomura Holdings Inc. took an impairment charge of almost $750 million for its overseas investment-banking business. Meanwhile, the government is worried that banks’ love affair with U.S. collateralized loan obligations could blow up.

Mizuho and its rivals have a combined stockpile of 142 trillion yen in international bonds, so getting out of overseas markets is hardly realistic. Besides, they’re sitting on too many deposits that need investing, and Japan’s ultra-low interest rates make finding domestic opportunities a challenge.

More mishaps may be unavoidable, unless Japanese banks become rapidly more sophisticated about overseas markets. But there is a damage limitation option – and it lies at home. That’s especially true for Mizuho, whose surprise 680 billion yen writedown last week could be a trigger to beef up its domestic lending infrastructure, embrace the fintech revolution and start focusing on the Japanese consumer.

About 460 billion yen of Mizuho’s charges were related to a long-delayed move to integrate its computer systems, which should be up and running this year. Born out of a merger of three banks with separate IT networks in 2002, Mizuho has been prone to frequent ATM crashes, most famously in the wake of the Fukushima earthquake and tsunami in 2011, and suffered an embarrassing failure of its online stock platform last year. Such incidents have given it a reputation as the tech weakling of Japan’s megabanks.

More skeletons could emerge when Tatsufumi Sakai, who took over as CEO in April, announces a three-year strategic plan in May.

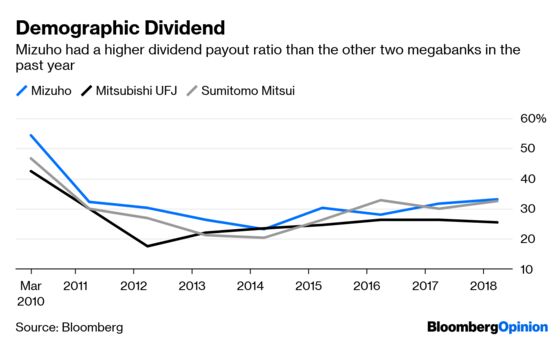

Mizuho has the flimsiest balance sheet of the three megabanks, with a leverage ratio of 4.37 percent at the end of December, versus 4.93 percent for Sumitomo Mitsui Banking Corp. and 4.97 percent at MUFG , according to data compiled by Bloomberg. In what may be a blessing in disguise, that’s limited the lender’s overseas expansion. It’s only investment in a foreign bank is a 15 percent stake in Vietnam's Vietcombank. Its closest competitors have far more investments in Southeast Asia and the U.S.

That doesn’t mean Mizuho won’t be able to find growth at home, if it gets its technology changes right and bulks up on consumer finance, while reducing a focus on low-margin corporate loans. The lender has already made a start: Mizuho has a consumer finance venture with Softbank Group Corp. called JScore that uses artificial intelligence to gauge borrowers’ creditworthiness. It’s also roped in 60 banks to form a payments app, JCoin Pay. That could disrupt SMFG, the leader in credit cards.

Granted, such changes will take time. For now, Mizuho’s rivals may remain more attractive for investors: MUFG and SMFG both have higher returns on equity, and are better placed to raise dividends.

The bank will also have to be more resolute in cutting costs. In November 2017, Mizuho pledged to cut 100 branches by March 2025 and shed 19,000 positions , or around a quarter of its workforce, by 2027. By the end of March 2018, none had been cut, according to Morningstar analyst Michael Makdad.

If it has the will, the laggard of Japan’s large lenders may just be able to carve out a future as the fintech megabank. Just as long as it abstains from more overseas expeditions.

Defined as the ratio of Tier 1 capital to total assets adjusted for derivative exposures etc.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Nisha Gopalan is a Bloomberg Opinion columnist covering deals and banking. She previously worked for the Wall Street Journal and Dow Jones as an editor and a reporter.

©2019 Bloomberg L.P.