(Bloomberg Opinion) -- Your online grocery order can often contain substitutions – which can also be a cheeky way for a seller to gain an advantage by giving you something that isn’t quite what you wanted.

Ocado Group Plc’s tie-up with Marks and Spencer Group Plc is no exception. The two companies on Wednesday said they had entered into a joint venture to sell M&S’s upmarket food, and the retailer will replace supermarket Waitrose as Ocado’s grocery supplier.

Tim Steiner, Chief Executive Officer of digital grocer Ocado, seems to have negotiated the better deal than veteran retailer and M&S chairman Archie Norman, who is paying a very high price for finally making a foray into food delivery. The stock market reaction says it all – early trading showed Ocado was the biggest gainer in the FTSE 100, and M&S the biggest laggard.

The deal gives Norman an online food business, something the company had been exploring how to crack on its own. But this market takes time to develop and perfect. And the average value of an M&S grocery basket is less than 20 pounds ($26.54), which makes the economics of home delivery extremely challenging. With Ocado, it is getting a service provided by a quality operator that will be up and running by 2020. The timing of this deal is true to Steiner’s form – he has a habit of stepping in just when retailers are most desperate to get online.

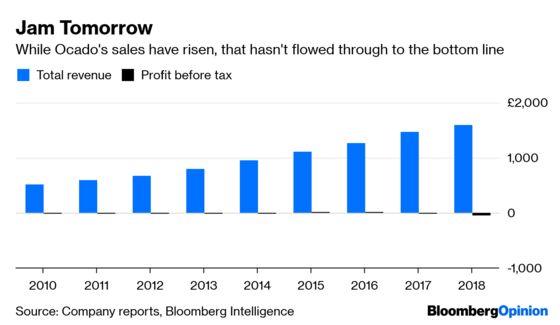

M&S is acquiring half of the company’s U.K. retail business for 750 million pounds. The price values the whole of this division at 1.5 billion pounds, and the companies say the joint venture would have generated Ebitda of 34.2 million in the year to Dec. 2, excluding fees due to Ocado. This implies a valuation of a massive 44 times trailing Ebitda.

Steiner gets most of the cash upfront – which he can use to invest in Ocado’s business that provides technology to retailers – even if the service doesn’t live up to M&S’s expectations. And his company will continue to get about 50 million pounds a year for running the venture.

In return M&S will get some synergies – at least 70 million pounds by the third year following completion. And sales through the joint venture should continue to expand.

Even so, the price it is paying looks extremely steep.

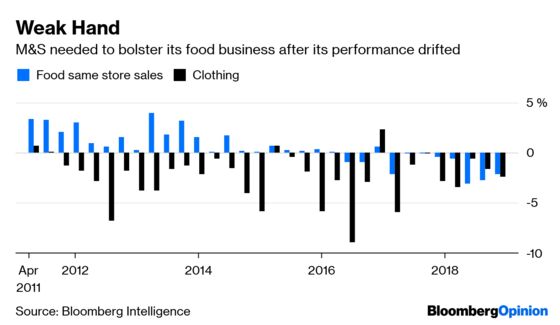

It could have been even higher had the recent fire at Ocado’s Andover warehouse not weakened its hand slightly. But neither was M&S in a strong position, given that its food performance has lost ground over the past few years.

And there are challenges. Chief among these is migrating customers who shop for Waitrose food via Ocado to M&S’s selection, particularly when Waitrose has its own competing online businesses. Expect a marketing blitz from the food arm of the John Lewis Partnership to retain its customers.

Norman must also convince investors that the outlay will be worth it, particularly as he is asking them to fund the deal through a 600 million pounds rights issue, as well as a dividend cut. Right now they are skeptical.

This is clearly a huge transaction for Norman. If it does take off, and M&S can bolster its food sales and generate the promised synergies, then the entry price will look less demanding.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2019 Bloomberg L.P.