Markets, Meet Your New Federal Reserve Maestro

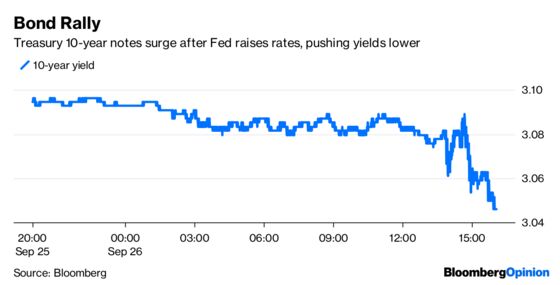

(Bloomberg Opinion) -- Federal Reserve Chairman Jerome Powell should be pretty pleased with his performance Wednesday. The central bank raised interest rates for the eighth time since December 2015, while simultaneously dropping its long-standing description of monetary policy as “accommodative” — implying that low rates are no a longer tailwind for the economy. Markets responded by taking it all in stride. It’s a bit like the 1990s, when investors enjoying buoyant markets dubbed then Fed Chairman Alan Greenspan the “maestro” for what they perceived at the time as his skilled stewardship of monetary policy.

Bonds rallied, the dollar weakened, and although stocks fell in the final half hour of trading, it could have been much worse. What makes those moves all the more remarkable is that the Fed also reiterated its plan to raise rates again in December, and at least three more times in 2019. Two thoughts help to explain the response of markets. First, the removal of the word “accommodative” after so many years means that the central bank is that much closer to the end of its rate-hiking cycle. The target for the federal funds rate has risen from 0.25 percent in 2015 to 2.25 percent, and many think the Fed will stop at 3 percent or 3.25 percent. Second, markets in recent years haven’t responded to rate increases as conventional wisdom would suggest. Remember when the Fed began tightening monetary policy in back in December 2015, and everybody said that it would be the end of the rally in equities, cause the bond market to collapse, and spark such a rally in the dollar that U.S. companies wouldn’t be able to compete in the global marketplace? Well, none of that happened. The reality is that the S&P 500 has gained 41 percent to an all-time high, the Bloomberg Barclays U.S. Aggregate Bond Index has gained 4.49 percent — not something to celebrate, but not the train wreck many predicted — and the Bloomberg Dollar Spot Index has fallen 4.16 percent. What most prognosticators failed to acknowledge is that central banking has become so transparent that forecasting rate moves has become the most predictable game in town.

When the Fed tells you what it is going to do, when it is going to do it and by how much, there are no surprises — and there’s plenty of time to prepare. The current system also accounts for the low levels of volatility across all markets. After all, who can say with a straight face that they were shocked that the Fed raised rates on Wednesday?

WILL HOUSING BREAK?

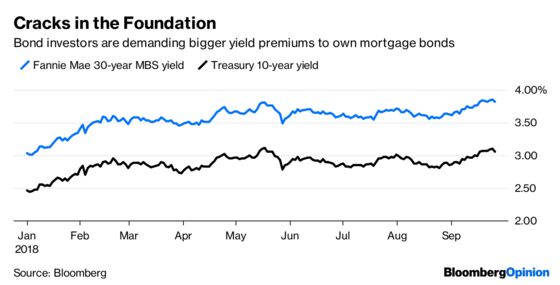

The skeptics are saying that the Fed won’t stop raising rates until “something breaks.” No knows what that will be, whether it’s a collapse in the stock or bond markets, further weakness in emerging markets that puts a drag on the global economy, or any number of potential negative outcomes. But one thing worth keeping an eye on is the U.S. housing market. The Fed’s rate increases have contributed to a big gain in home loan rates, with Freddie Mac saying the average on a 30-year mortgage is now above 4.60 percent, the highest since 2011. An index compiled by the National Association of Realtors shows housing affordability is the lowest since 2008. Although the U.S. government said Wednesday that new home sales came in at a 629,000 rate in August, up 3.5 percent over July, the trend is clearly down, with the three-month average of 618,000 below the six-month average of 636,000, which is below the 12-month average of 643,000. Bleakley Financial Group chief investment officer Peter Boockvar wrote in note to clients Thursday that the slowdown is clearly “a demand issue via rich pricing and higher mortgage rates that is resulting in a slowdown in the pace of transactions.” Bond investors seem concerned. They are demanding about an extra 77 basis points in yield to own current coupon Fannie Mae 30-year mortgage bonds rather than 10-year Treasuries. The spread is the widest since 2016 and up from about 55 basis points at the start of the year. That’s nowhere near crisis-era levels of more than 200 basis points, but the direction bears watching.

OIL SUPPLIES SURGE

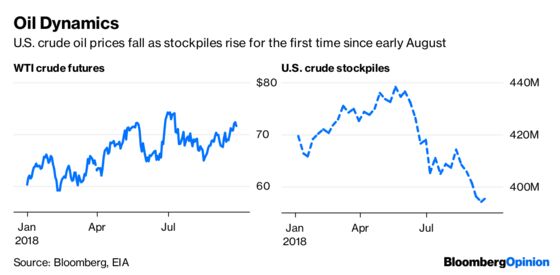

If President Donald Trump really wants to get the price of oil down, maybe he should focus his attention closer to home rather than pressuring OPEC. West Texas Intermediate crude fell as much as 0.97 percent on Wednesday to below $72 as the Energy Information Administration said oil stockpiles expanded by 1.85 million barrels last week, the first increase since early August. Insufficient supply was one reason oil prices jumped from less than $65 a barrel in mid-August to as high as almost $73 this week. So, it’s not hard to conclude that an increase in production by the U.S. oil industry might ease the pressure on prices. The EIA report also showed that overseas demand for American oil jumped to a two-month high, according to Bloomberg News’s Jessica Summers. “We are seeing exports continue to increase, so that is more of a permanent trend,” Matt Sallee, a portfolio manager who helps oversee $16 billion at Tortoise Capital Advisors, told Bloomberg News. Of course, there are plenty of variables that go into the price of oil besides supply, but it’s hard to say that it’s not the biggest. And though it’s not assured that U.S. producers would welcome lower prices, they sure seem to have a lot of capacity these days. The EIA also said refinery utilization rates last week dropped to the lowest since May.

CHINA STOPPED DELEVERAGING

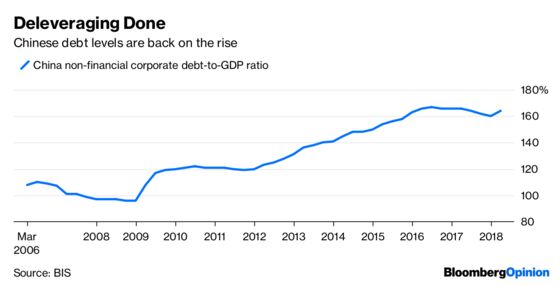

Along with U.S. and pan-European junk bonds, the only other major debt market to show a gain this year is the one in China. It’s not much, but the Bloomberg Barclays China Aggregate Index has eked out an increase of 0.1 percent through Tuesday, which compares favorably to the 2.06 percent drop in the benchmark Bloomberg Barclays Global Aggregate Bond Index. China has attracted a lot of global investors in recent years attracted to talk by officials there that they were embarking on a concerted effort to deleverage from elevated levels. But now, those efforts look to be falling by the wayside as China seeks to bolster its economy against tariffs levied by the U.S. New data from the Bank for International Settlements shows that Chinese non-financial corporate debt jumped to 164.1 percent of gross domestic product in the first quarter from 160.3 percent in the final three months of 2017. The increase erased more than half of the progress Chinese companies had made in reducing debt loads since the ratio topped out at 166.9 percent in the second quarter of 2016, according to Bloomberg News. In 2017, “faster GDP growth allowed the authorities space to operate tight monetary policy. As a result, debt growth slowed,” Freya Beamish and Miguel Chanco, economists at the independent research firm Pantheon Macroeconomics Ltd, wrote in a report published Wednesday. “That benign backdrop has now dissolved.”

TALK IS CHEAP

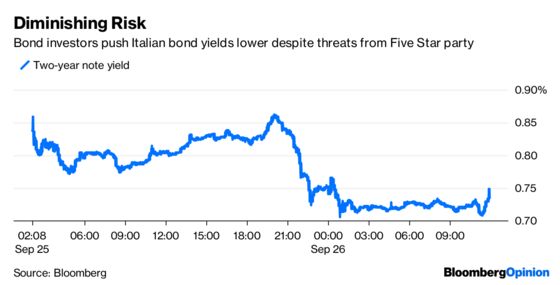

It was just a couple of months ago that the primary concern among many big investors was that political turmoil in Italy and the rise of the euro-skeptic Five Star party would majorly upset global markets. Such anxiety was warranted when you consider that Italy has $2.33 trillion of debt, compared with just $383 billion for Greece, which caused all that trouble a few years ago. But the situation in Italy has calmed to the point where investors view the latest Five Star threats as mere bluster. That was on display Wednesday, as Italian two-year bond yields dropped a rather large 8.2 basis points to 0.14 percent as investors bid up the price of the notes even though Five Star Leader Luigi Di Maio threatened to block the 2019 budget barely 48 hours before the deadline to produce an initial deal. Despite leading the biggest group in parliament, 32-year-old Di Maio has been consistently outmaneuvered by the anti-immigration drive of his coalition partner Matteo Salvini, according to Bloomberg News’s John Ainger and Alessandra Migliaccio. Salvini’s League won barely half as many votes as Five Star in March’s general election, but recent opinion polls have shown the League with a consistent lead of around 4 percentage points over Di Maio’s group. “Di Maio hasn’t won in his internal debates yet,” Richard Kelly, head of global strategy at Toronto-Dominion Bank, told Bloomberg News. “The default position now is a smaller deficit unless Di Maio can get concessions, rather than the other way around.”

TEA LEAVES

For all of Trump’s efforts, the U.S. trade deficit has gotten worse under his watch. America’s merchandise trade shortfall expanded to $72.2 billion in July from $63.5 billion at the end of end of 2016. The Commerce Department is slated to release the latest data for August on Thursday, and the median estimate of economists surveyed by Bloomberg is for a deficit of $70.6 billion, which may only prompt Trump to ramp up the rhetoric about how foreign countries are taking advantage of the U.S. What we know is that some businesses in the U.S. stepped up imports last quarter ahead of announced tariffs and the threat of further levies, prompting foreign customers to also accelerate orders with American producers, which helped to boost gross domestic product. The August data may show whether that trend continued into the third quarter, and if so, to what degree.

DON’T MISS

Fed Is Accommodative to Flattening Yield Curve: Brian Chappatta

Powell’s Fed Is Taking Off the Training Wheels: Daniel Moss

Why Foreign Funds See Pandas in China’s Bear Market: Shuli Ren

Underemployment Is the New Unemployment: Leonid Bershidsky

Matt Levine’s Money Stuff: Abacus CDO Bites Goldman Back

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.