Markets Know a Hollow Threat When They See It

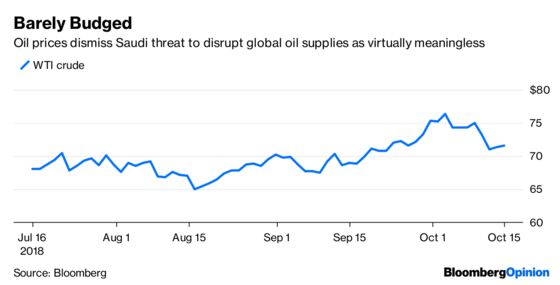

(Bloomberg Opinion) -- Saudi Arabia says it will retaliate against any punitive measures tied to the disappearance of Washington Post columnist Jamal Khashoggi with even “stronger ones.” For many, that means the world’s biggest oil exporter is threatening to hold back on selling crude, creating a global supply shortage and sending prices skyward when the global economy is already decelerating. All that sounds disconcerting — except to the markets.

Perhaps if this was another time, say 30 years ago when Saudi Arabia played the role of “swing producer” and could influence the global economy by setting the price of oil without challenge, this all would matter. But it’s not. The global energy market is now more diversified in terms of products and producers, with even the U.S. a net exporter. Although oil did spike as much as 1.36 percent at the open, it was little changed at $71.45 a barrel in late New York trading. Also, the MSCI All-Country World Index of stocks was little changed as were top government bond markets such as those for U.S. Treasuries and German bunds. As Bloomberg Opinion contributor and economist Gary Shilling noted in a recent column, oil will be in surplus in future years not only because of increasing output potential but also because of rising supplies of natural gas, which have also been made abundant by fracking.

The Saudis, who still pump one in 10 oil barrels produced worldwide, can certainly inflict harm on the global economy in the short term by cutting output, according to Bloomberg News’s Javier Blas. Plus, the kingdom and holds nearly all the spare capacity available to respond to any supply outage. That said, the Saudis have a long history of separating their oil business from politics. And for all its riches, the kingdom’s economy has been under pressure in recent years. As such, markets know the Saudis have little desire to do anything that gets in the way of their plan for an initial public offering of Aramco that values the state-run company at $2 trillion.

MARKETS DOING THE FED’S JOB

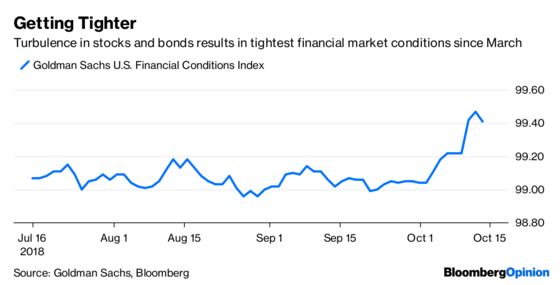

There’s been a lot of soul searching in the wake of the big declines recently in both the U.S. stock and bond markets and what it all means. President Donald Trump blames the Federal Reserve for the gyrations, saying policy makers have gone “loco” and “crazy” by raising rates six times since he’s been in office. Almost nobody expects the Fed to not raise interest rates once more by the end of the year as the market expects because of Trump’s remarks. If anything, the betting is that policy makers will want to show their independence and continue to raise rates at almost any cost. But would it truly be “loco” if the Fed does decided to take a pause? Perhaps not when you consider how much the recent carnage has caused financial conditions to tighten. The more than 5 percent drop in the S&P 500 Index last Wednesday and Thursday, combined with the 10 basis point rise in Treasury 10-year note yields, is roughly equivalent to a 25 basis point increase in the Fed’s target rate, according to Jason Furman, a former top economic adviser to President Barack Obama and a professor of the practice of economic policy at Harvard University. “I was comfortable with the Fed hiking again in (December, but) the market just did it for them,” Furman wrote on twitter. The widely followed Goldman Sachs U.S. Financial Conditions Index, which rises when they tighten, rose last week to its highest since May 2017. While the overall level is historically low, the direction has to be concerning.

THE DOLLAR AND DEFICITS

If the U.S. economy is really the strongest in history, then how do you explain the malaise in the dollar? The Bloomberg Dollar Spot Index, which measures the greenback against its main peers, is basically flat over the last four months and is up just 2.59 percent for the year. To a growing number of traders and strategists, the dollar’s lackluster performance appears tied to jitters over what is perceived to be out-of-control fiscal spending that shows few signs of slowing, let alone reversing. For example, the spot index fell to its lowest in more than two weeks on Monday as the U.S. government said its budget deficit grew to $779 billion in the 2018 fiscal year ending Sept. 30, the biggest shortfall since 2012 amid tax cuts and spending increases. “A budget deficit that’s heading toward ($1 trillion) at a rapid pace while the economy’s growing above potential is going to scare the FX market when the slowdown hits, as it surely will,” Kit Juckes, a global strategist at Societe Generale SA, wrote in a September report. “The dollar’s going up by the stairs and risks coming down by the elevator, starting sometime in 2019.” By that reasoning, it’s only a matter time until the dollar bulls, who have raised their bets on a gain in the greenback to the highest since January 2017, throw in the towel and start reversing those positions, putting further pressure on America’s currency.

ALL TOGETHER NOW

The S&P 500 failed to post its first back-to-back gain on Monday since the week of Sept. 17, falling rising 0.59 percent after Friday’s 1.42 percent surge that was the biggest since April. One of the more notable byproducts of the recent gyrations in the equity markets is that it has sparked a sort of herd-like mentality among traders, with the implied correlation among S&P 500 members jumping to the highest level since April. Heading into the heart of earnings season, a high correlation coefficient means it may be trickier for investors to pick stocks because market turbulence will affect all companies regardless of their individual results, according to Bloomberg News’s Cecile Vannucci. So, which companies and sectors might investors want to avoid? Bloomberg News looked at about a dozen companies that analysts have soured on the most, which means cutting their earnings-per-share estimate by at least 5 percent. Among them, insurers American International Group Inc. and Chubb Ltd. have found themselves in the crossfire of Hurricanes Florence and Michael, according to Bloomberg News’s Brandon Kochkodin. Ford Motor Co. cited “a tale of two hurricanes” for tumbling F-Series pickup sales. And its troubles spilled into the materials sector. PPG Industries, a maker of automotive paints that counts Ford among its biggest customers, blamed falling demand in China and factors that would affect “most of the auto suppliers.”

GOLD BUGS DO THE JITTERBUG

Things are finally looking up for the gold bugs. After a sort of delayed reaction to the turmoil in emerging markets, bullion has begun to move higher, trading at its highest level since July, or about $1,229 an ounce. Its 1.11 percent gain last week came after a surge of 1.07 percent the previous week. That marked its strongest showing of the year since gold jumped 2.52 percent in one week in March. Because gold is widely seen as a haven asset, it’s probably safe to say that the latest move higher is a reflection of the market’s belief that the turbulence in global markets has a much a much bigger chance of developing into some sort of contagion than the carnage that was seen in emerging markets for much of the year. “Sentiment for gold should improve given the risk rising in the equity market,” Maxwell Gold, a director of investment strategy at Aberdeen Standard Investments, which oversees about $730 billion, told Bloomberg News. “Right now is an attractive time to strategically add positioning for gold investment to hedge against concerns on equity volatility and add to diversification.” But not everyone is convinced that gold is due for a sustained rally. Speculators boosted their net short position in bullion futures and options to the largest since at least 2006 in the week ended Tuesday, according to government data released three days later. Because gold pays no interest, its appeal diminishes when interest rates are rising, and the Fed has not signaled any slowdown in the pace of the rate-hiking cycle.

TEA LEAVES

It is that time when market participants get a barrage of data on the health of housing. The reports are sure to receive some extra attention with 30-year mortgages rising last week to their highest since early 2011 and housing affordability as measured by the National Association of Realtors at the lowest in a decade. Any significant weakness in the data may spark cries that the Fed has gone too far, too fast in raising interest rates. First up will be the National Association of Home Builders/Wells Fargo sentiment index. The gauge is forecast to drop 1 point to 66 for October. Although that would be the lowest since September 2017, it would still mark a relatively high level. The surprise is that sentiment among home builders isn’t worse, given a Bloomberg index tracking their share prices has crumbled 33 percent this year. On Wednesday, the government is expected to say that housing starts fell 5.6 percent in September, and on Friday the National Association of Realtors may say existing home sales dropped 0.9 percent in the months.

DON’T MISS

Economic Leaders Point to Mounting Risks: Mohamed A. El-Erian

Saudi Arabia Points the Oil Weapon at Itself: Liam Denning

Oil Demand Is Cooling. Don’t Expect Prices to Follow: Julian Lee

Housing Market Is Raising Serious Red Flags: Lakshman Achuthan

Fed Inflation Policy Keeps Unemployment Too High: Karl W. Smith

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Robert Burgess is an editor for Bloomberg Opinion. He is the former global executive editor in charge of financial markets for Bloomberg News. As managing editor, he led the company’s news coverage of credit markets during the global financial crisis.

©2018 Bloomberg L.P.