The Market’s Best-Performing Stock Is a Coin and a Prayer

(Bloomberg Opinion) -- What happens when you combine the cryptocurrency craze, a pie-in-the-sky marketing pitch and the public company alchemy championed by Jay Clayton, the chairman of the Securities and Exchange Commission?

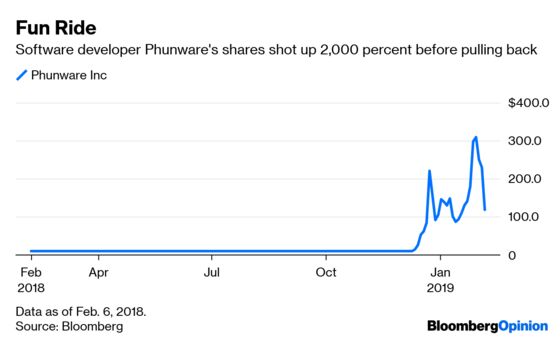

You get the best-performing, but also most volatile, stock of the year. Shares of software developer Phunware Inc. have risen 721 percent to $119 after trading for $10 in December. The rise is nearly 15 times that of the best-performing stock in the S&P 500 — Xerox Corp., which is up a respectable 49 percent.

How Phunware attracted these investors, and more important what it’s doing to live up to the promise of its lofty valuation, is a convoluted tale that includes a cast of characters from Greece to Texas, a death threat to Facebook, some financial gloss and the recurring question about the benefit of special purpose acquisition companies.

Phunware never really went public, at least not in the typical way. Until December, Phunware was called Stellar Acquisition III Inc., one of a growing number of so-called SPACs, or blank-check companies, that raise money in anticipation of doing a deal. They have multiplied as listing requirements have loosened, again thanks to Clayton and in this case Nasdaq.

Stellar, it turned out, was blanker than most. The company, listed on Nasdaq, was based in the Marshall Islands and run from Athens by two Greek shipping executives who said they planned to do a deal in the energy logistics space. Instead, on the day after Christmas, the company closed its purchase of Phunware, and as blank-check companies often do, changed its name and assumed the Austin-based app developer’s identity and history.

But there was a final twist. By SPAC rules, shareholders have to vote to approve the transaction. But even if they do, they can still ask for their money back, and in the case of Phunware more than half did. That left Phunware with few shares outstanding that are not in the hands of insiders. The result is the stock is prone to sharp swings. For example, Phunware’s shares plunged $111 on Wednesday after the company disclosed that a number of its insiders, including its chairman, Akis Tsirigakis, and several original investors had registered to be able to sell their shares. In December, Tsirigakis, said he was “pleased” to be part of such “exciting company at the forefront of innovation.” Less than two months later, though, it seems as if he would be pleased to have his money invested elsewhere. After the proposed sale, Tsirigakis would own no Phunware shares, though he may still retain some of his warrants.

Much of Phunware’s revenue comes from its existing app development business, and on the surface it wouldn’t appear to justify its $3.3 billion market cap. In the 12 months ended Sept. 30 — Phunware has yet to report fourth-quarter results — the company booked revenue of $29.5 million, which means that its stock is trading at 112 times sales. Growing companies do trade at generous multiples. Streaming service Netflix Inc., for instance, trades at nearly 10 times its sales. The problem is Phunware has been shrinking. Its revenue has dipped more than a third, from just more than $47 million in 2016.

The promise of Phunware, and the apparent reason for its soaring stock, is its digital currency, PhunCoin, which, among other things, will put Facebook Inc. out of business, or so Phunware CEO Alan Knitowski claimed on Twitter recently.

There is a white paper, and it has a somewhat compelling and timely pitch. Last month, the company was selected to be part of a blockchain accelerator program sponsored by Columbia University and IBM. Phunware says Facebook, Google and others are making billions of dollars by monetizing users’ data, and consumers have so far been helpless to stop them until now, or whenever PhunCoin is adopted widely. Essentially, Phunware says users will be able to register in its system the personal information they are willing to share online. A digital platform will track where and by whom that data is used, and companies will have to pay for that. Those payments will be made, naturally, in PhunCoin, which will eventually be redeemable for goods or services. Got it?

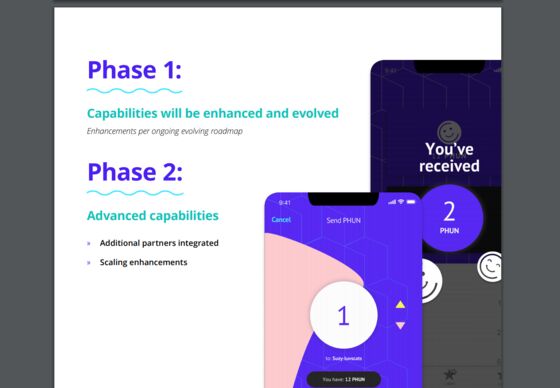

It’s also unclear how this would all get started. The white paper lacks details about that. It says its plan includes Phase 1, in which “capabilities will be enhanced.” Phase 2 lists simply “advanced capabilities.”

PhunCoin’s success, it seems, would require everyone, or at least a lot of people, to opt out of sharing all their personal data everywhere, even on their phones. Facebook and other companies would then have to agree to pay for that data, and, on top of that, adopt Phunware’s platform and currency. Also unclear is whether any of this is allowed under cryptocurrency regulations. Knitowski has said that Phunware is the first company of its kind to do a securities offering for a digital currency that has been blessed by the SEC, but that appears to be an exaggeration. The SEC declined to comment. Phunware did file a document with the SEC notifying investors of the PhunCoin offering, but it was a Registration D filing, which is technically unregistered, meaning it was neither approved nor rejected by the SEC. In fact, the form Phunware filed says clearly that the SEC has not necessarily reviewed the information or verified its accuracy. The form says Phunware was seeking to raise $100 million in the PhunCoin offering.

PhunCoin has not exactly caught on. Phunware introduced its digital offering in June. Since then, it has raised only $94,210 publicly, according to an offering website that is linked to Phunware’s corporate home page. Phunware’s most recent financial statement, though, says it has raised $913,000 from the sale of digital currencies, which includes private transactions. The prospectus for the SPAC merger in February 2018 said it had hoped to raise $10 million through the PhunCoin offering by mid-2018. Knitowski said a delay in regulatory approval forced the company to scrap that time frame. Instead, the company raised a similar amount through an equity offering, rather than in PhunCoin directly, he said.

If Phunware’s ambitions are outsized, so are the boasts of its CEO. At a conference last August, Knitowski told a crowd that Phunware was profitable and debt free. Phunware did turn a profit in the second three months of 2018, but it has never reported an annual profit. In 2017, it lost nearly $26 million. For the first nine months of 2018, even with that one profitable quarter, the company lost $6 million. Also, it’s true that Phunware does not have any long-term bank loans or bonds, but it does have $8.2 million in deferred revenue, which is generally considered debt and is listed on Phunware’s financial statements as a long-term liability. Phunware says deferred revenue is upfront cash payments that has been billed to clients for future projects. The company’s financial statements, for instance, say it received $3.5 million in cash from deferred revenue in 2017 alone. It records those sales as actual revenue along with any other payments and costs when it performs the service, as required under accounting rules. The problem is it appears much of that upfront cash has been spent. At the end of the third quarter, Phunware had just $122,000 in cash.

Worse, it appears Phunware struggles to get clients to pay once it has actually completed the work. As of the end of September, Phunware had $7.4 million in accounts receivables, of which $3.2 million, or 43 percent, were listed as doubtful. Many companies have some customers who end up not paying their bills, but that’s usually in the single digits. Robert Willens, an accounting expert, said he had never seen a company with such a high percentage of doubtful accounts. Phunware attributed the bulk of the doubtful accounts to Uber Technologies Inc., which Phunware is suing for payment. Uber has countersued, contending Phunware falsely billed for ad clicks it didn’t generate. Uber also contends Phunware falsified reports to hide the fact that it was running Uber’s ads on porn sites against the companies wishes. Phunware has said in its financial filings that Uber’s allegation is without merit.

As for the drop in revenue, Phunware attributed it to complying with an accounting change and exchanging one business for a faster-growing one. Still, the company doesn’t appear to be living up to its own projections. In early 2018, Phunware said that its sales backlog would hit $55.4 million by the end of the year. Instead, as of Sept. 30, Phunware’s backlog had fallen slightly to $26 million, from $32 million the year before.

When I talked with Knitowski, he echoed Clayton’s sentiments about blank-check companies. He said public markets had long been unfair and unwelcoming to small companies like his and that without the growing market for SPACs, Phunware would have never been able to go public. The question is whether that is really an improvement. Whether or not companies like Phunware end up being the exciting investment opportunity for “Mom and Pop 401(k)” that Clayton envisioned, the market’s going to get a lot more like it. Investors need to watch out.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2019 Bloomberg L.P.