(Bloomberg Opinion) -- Whisper it, but Australia’s millionaires factory had until recently risked looking a bit boring.

Macquarie Group Ltd., the country’s largest investment bank, got the nickname in the go-go years before the 2008 financial crisis when returns ran freely and bonuses were rich. To survive the crisis, it remade itself into something akin to a bond fund.

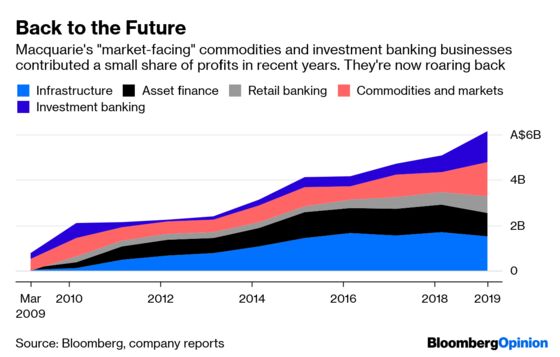

Its core units in infrastructure, asset finance and retail banking were branded “annuity-style” businesses in recognition of their steady but (mostly) unspectacular returns. Net income from its more volatile trading desk and investment bank — the so-called “market-facing” businesses — dwindled to bit less than a quarter of the total in its 2016 fiscal year.

Annual results announced Friday show those less-loved divisions are roaring back. The Commodities and Global Markets trading business saw net income climb by two-thirds, to become Macquarie’s biggest profit contributor for the first time since 2011. The Macquarie Capital investment bank did even better, with net income nearly doubling to A$1.35 billion ($944 million) from A$716 million a year earlier.

The trend is both positive and negative. One argument for Macquarie’s annuity-market split has long been that the two sides are natural hedges against each other. When economic conditions improve and reduce returns from the interest rate-dependent annuity businesses, the transactional activity supporting the market businesses ought to heat up and balance out any weakness.

The evidence to date suggests this strategy is working: The A$1.25 billion improvement in net income from trading and investment banking was more than enough to offset the A$164 million drop from the annuity side.

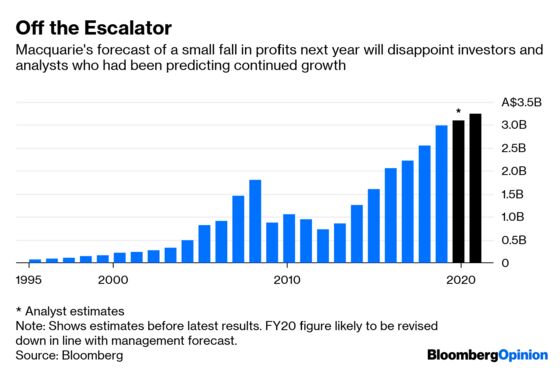

At the same time, it’s early days yet. Earnings next year will be “slightly down,” Macquarie said, in contrast to analysts’ expectations of another year of growth; the shares fell 7 by percent, their worst performance in nearly three years, as a result. A big factor in the downbeat forecast was simply that the past year was an unusually good one for commodities, management said. A return to more normal conditions for such a major division will inevitably weigh upon future income.

In addition, there’s the question of what’s still hidden in the black box of the annuity businesses. As we’ve argued in the past, the potential risks to infrastructure from higher interest rates are profound: Funding costs risk rising faster than revenues and, if those conditions are seen as becoming the status quo, accountants may have to write down the value of long-term investments, stripping more money from the income statement.

There are already some glimpses of this from the core Macquarie Asset Management infrastructure business. Expenses last year rose by a third to A$1.33 billion, even as operating income crept up just 11 percent.

Ultimately the problem is that infrastructure — the engine of Macquarie’s growth over the past decade, with returns on assets of 19 percent or so — may not prove to be quite the annuity that it’s promised to be. A more volatile and robust global economy risks opening up cracks in a business model that’s been rock-solid over the past decade. There’s no guarantee that trading and investment banking will be sufficient to plaster over that weakness.

Investors have liked the new look of Macquarie in recent years as its market-facing businesses have pumped out more profits and taken up a larger share of net income. In contrast to its retail-focused Big Four rivals in Australia, the bank’s price-book valuation has soared to its highest levels in a decade. But the flip side of rising profitability has been rising volatility, something investors are only just starting to appreciate.

If Macquarie wants to win back their affection, it should heed the lesson of its own restructuring. Investors like returns, but they like annuity-style stability even more. In finance, boring is beautiful.

To contact the editor responsible for this story: Nisid Hajari at nhajari@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

David Fickling is a Bloomberg Opinion columnist covering commodities, as well as industrial and consumer companies. He has been a reporter for Bloomberg News, Dow Jones, the Wall Street Journal, the Financial Times and the Guardian.

©2019 Bloomberg L.P.