(Bloomberg Opinion) -- You don't want to just buy the must-have handbag or wear the pricey jewels anymore, you want to stay at the luxe hotel and dine at the posh restaurant.

That's the motivation behind LVMH’s $2.6 billion purchase of Belmond Ltd, the owner of the Hotel Cipriani in Venice and the Copacabana Palace in Rio de Janeiro.

Across the consumer sector, the move to spending on experiences instead of things is gaining traction. Luxury is no different. In the upper echelons, however, a manicure and a meal out won’t cut it. Cosmetic surgery and a gourmet restaurant are more the order of the day.

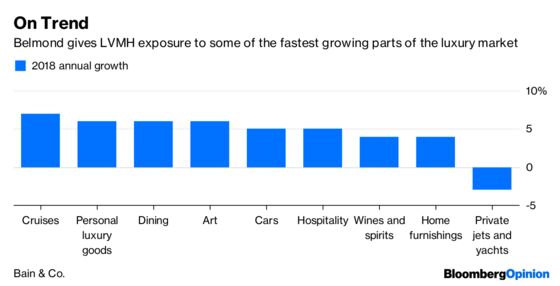

True, pricey personal goods have enjoyed strong growth in 2018. But over the past seven years, high-end experiences have expanded at a faster pace, according to Bain & Co. Hospitality and cruises, two of London-based Belmond’s specialties, were big winners this year.

LVMH, the world's largest luxury goods group, already owns the Bulgari and Cheval Blanc hotel chains, but adding Belmond significantly increases its exposure to hospitality and gives it a portfolio of trophy assets.

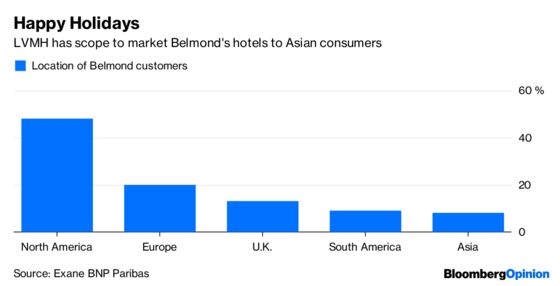

Just under half of Belmond's customers come from North America, and 8 percent come from Asia, according to analysts at Exane BNP Paribas. That offers some useful geographic diversification amid signs of slowing Chinese spending. But longer term, there’s an opportunity to expand the customer base from Asia, and the potential for synergies with the hotel assets the French group already owns.

Those benefits don’t come cheap. LVMH is paying a 42 percent premium to Belmond's closing price in the U.S. on Thursday. The enterprise value of $3.2 billion equates to about 5.6 times trailing revenue and 24 times Ebitda, according to Bloomberg data. That is well ahead of the average for lodging deals in the past three years – 2.6 times trailing revenue and 13 times Ebitda.

LVMH is right to pay up. In the world of luxury, buyers often only get one chance to pick up coveted assets. Once they go to a rival, it’s a long time before they come onto the market again.

And anyway the group, led by Bernard Arnault, can afford it. Net debt had been set to be 0.4 times Ebitda at the end of 2018, according to the consensus of Bloomberg estimates. With this deal, pro-forma borrowings will increase to 0.6 times earnings, according to analysts at Citigroup Inc. That still looks a very comfortable level. What’s more, Bloomberg Intelligence’s Deborah Aitken estimates LVMH could spend $20 billion on deals and still maintain net debt at 2 times Ebitda.

So while the king of bling may have paid up for his luxury vacation, the stay should be worth it.

To contact the editor responsible for this story: Jennifer Ryan at jryan13@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Andrea Felsted is a Bloomberg Opinion columnist covering the consumer and retail industries. She previously worked at the Financial Times.

©2018 Bloomberg L.P.