I Drank Myself to the Bottom of Luckin Coffee's IPO

(Bloomberg Opinion) -- The pending Nasdaq debut of China’s Luckin Coffee Inc. begs the question of whether it’s a purveyor of beverages, or a technology company.

As I pore through its 286-page IPO filing, I find myself struggling to decide. It’s kind of like Starbucks Corp., I guess, but also a lot like food-delivery giant Meituan Dianping and ride-hailing pioneer Uber Technologies Inc.

Luckin splits the difference, deciding that it’s both:

We are China's second largest and fastest-growing coffee network, in terms of number of stores and cups of coffee sold

A coffee network, seriously?

The IPO prospectus is relatively light for such a document. Coffee appears 278 times outside of the “Luckin Coffee” combo (110 times). App or apps features 51 times; technology and network 79 times apiece.

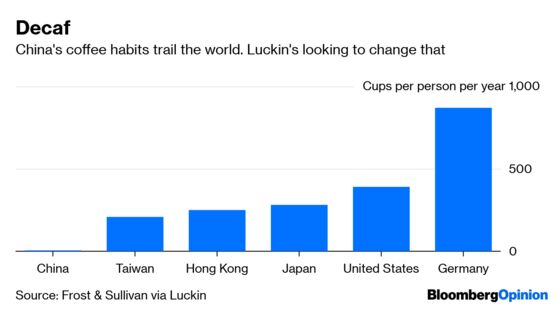

China, a nation of tea drinkers, is only just starting to get a taste for espressos and lattes. Coffee consumption was a mere 6.2 cups per capita last year, the prospectus states, citing consultants Frost & Sullivan. Germany guzzles 867.4 cups. Across the Strait, Taiwanese are downing 209.4 cups apiece.

So there’s a lot of upside potential, which is a big selling point for Luckin’s IPO.

Still, there’s something not quite Starbucks about this company. My colleague Nisha Gopalan wrote a great explainer about Luckin a few months ago. “These days in China, no retailer can flourish without the two Ds — being delivery-friendly and digitally savvy,” she wrote. That’s an important and insightful observation.

Luckin is proud to have an app that offers a “100% cashier-less environment.” That’s no surprise to anyone in China, given the digitization of the country – to the point that even beggars have QR codes.

But it’s the income statement that provides the strongest clue to the company’s true identity.

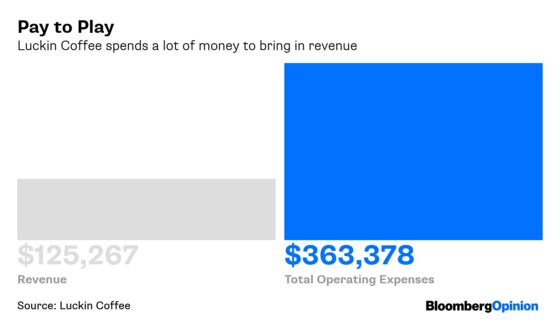

Luckin posted 841 million yuan ($125 million) in revenue last year, exploding from 250,000 yuan the year prior. But its operating expenses were three times higher than sales at 2.4 billion yuan. And it wasn’t even materials, store rentals or admin expenses that blew out the bottom line.

Marketing costs were 746 million yuan last year. To make every 100 yuan from selling coffee, Luckin spent 152 yuan to produce and market that cup – not including rent and general expenses.

Spending three times more than revenue makes Luckin a tech startup, not an F&B company.

Following in the footsteps of compatriots such as e-commerce operator Pinduoduo Inc. and Meituan, Luckin spent glutinous amounts of VC cash to boost the top line, with little care for the bottom line.

Like any good purveyor of addictive substances, its twist on that model has been to hand out free coffee. The U.S. listing of a Chinese company that gives away stuff makes for the perfect mashup of socialism and capitalism.

Luckin needs to remove those marketing subsidies to turn a profit, although doing so will probably see it lose sales. Unless it’s built some kind of loyalty among consumers that others haven’t, I don’t see how it can produce stable profits anytime soon. But maybe I just need to wake up and smell the coffee.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2019 Bloomberg L.P.