(Bloomberg Opinion) -- Lenovo Group Ltd.’s net income beat analysts’ expectations by $53 million, or 45 percent.

While that upside surprise was helped by slightly stronger revenue and a slimmer operating-expense margin — from a reduction in sales and distribution costs — operating income benefited a lot from one-time accounting items.

A fall in gross margin by 0.3 percentage points from a year earlier to 13.4 percent is a hint that profitability isn’t as solid as it looks. It missed estimates of 13.9 percent.

Going through the P&L, we can see that various valuation metrics were the primary contributors to stronger-than-estimated numbers.

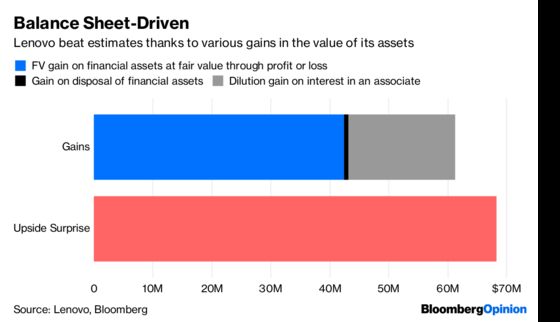

Chief among them: fair value gains on financial assets at fair value through profit or loss boosted the operating line by $42.4 million. Another line item, dilution gain on interest in an associate, added $18 million. All up, Lenovo gained $61.3 million from these accounting tweaks. That’s more than the scale of the company’s net income beat, and accounts for 90 percent of the $68.4 million by which expected operating income surpassed reported operating income.

While investors are keen to see a turnaround at Lenovo, this may not be it.

To contact the editor responsible for this story: Rachel Rosenthal at rrosenthal21@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Tim Culpan is a Bloomberg Opinion columnist covering technology. He previously covered technology for Bloomberg News.

©2018 Bloomberg L.P.