(The Bloomberg View) -- Wall Street’s powerhouses are beginning to lose some power.

JPMorgan Chase & Co. kicked off third-quarter earnings for the big banks on Friday, and while the results were better than expected, they showed a lack of energy in key division: investment banking. Revenue from fixed-income trading was down 10 percent, which was worse than analysts were expecting. Fees from equity and debt underwriting as well as advising on mergers and acquisitions were down 1 percent from a year ago. Equity trading, the one bright spot, was up 17 percent.

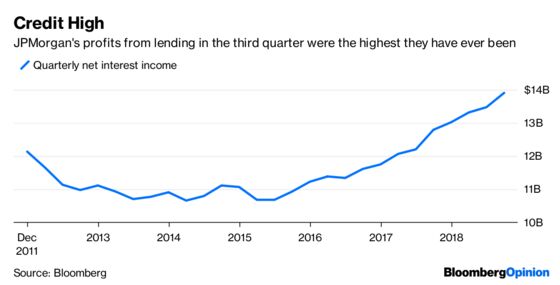

None of that was enough to upend JPMorgan’s quarter, most likely because the economy overall is still quite good — even if the markets have turned rocky — and the benefit of this year’s tax cut is still fresh. Revenue was up 5 percent from a year ago. Earnings per share rose 33 percent. Loans were up 6 percent. But the big driver of profits was that few of those loans are going bad, which is to be expected in an economy with a 3.7 percent unemployment rate. JPMorgan lowered its provision for credit losses in its consumer bank by $537 million, or 35 percent, from the same quarter a year ago. What’s more, the recent increase in interest rates has at least so far helped more than it has hurt. JPMorgan’s interest income was $13.9 billion, which is the highest three-month total in the firm’s history, topping the $13.8 billion it earned in the final quarter of 2008.

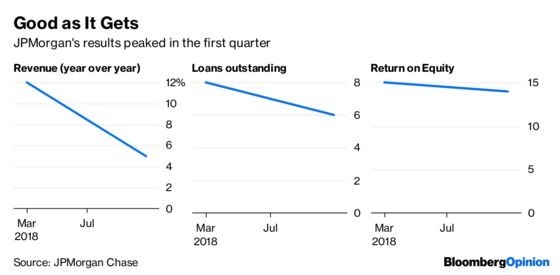

But along with the good results is growing evidence that this could be as good as it gets. That was essentially the call of longtime bank analyst Charles Peabody of Portelas Partners earlier this week when he downgraded JPMorgan’s shares to a sell rating. “It feels like 1987 to me,” Peabody said. JPMorgan’s earnings provided evidence of that.

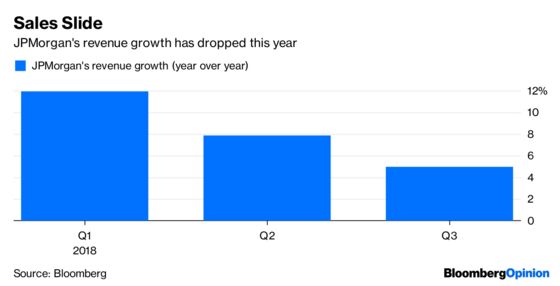

Revenue growth eroded from the 8 percent growth in the second quarter, which itself was down from 12 percent in the first quarter. Return on equity of 14 percent was among the best JPMorgan has had in years, but it still only matched last quarter’s result and was down slightly from the first three months of the year. And in one of the strongest economies in years, the bank’s 6 percent loan growth is better than rivals, but that’s not saying much. The yield curve has steepened slightly since the end of the third quarter, which will help a bit if it stays that way, but not as much as it would have if interest rates had risen a few years ago. Two years ago, JPMorgan forecast that a 1 percent increase in interest rates would boost earnings by $3 billion. It recently cut that forecast by two-thirds.

Dimon has long said his bank is better prepared to weather downturns than rivals because of its size and diversification. And Dimon may indeed have built the best financial firm in the land. But in the past few years, he has tilted the bank more toward those Wall Street-centric businesses that will be hurt first when the economy turns, and the stock market rockiness this week may have signaled the start of that.

While Dimon himself has had some public stumbles in the past few months — most notably drawing President Donald Trump into a political war of words, and then backing down — his giant bank never lost its stride. Dimon the CEO is on firmer footing. What comes next, though, might give Dimon something to be worried about.

Stephen Gandel is a Bloomberg Opinion columnist covering banking and equity markets. He was previously a deputy digital editor for Fortune and an economics blogger at Time. He has also covered finance and the housing market.

©2018 Bloomberg L.P.