(Bloomberg Opinion) -- Japan’s health-care stocks are back. Short-sellers have packed up shop, and value investors are nosing around for opportunities.

The sector has risen 7 percent this year, outpacing a 5 percent gain in the broader Topix index. Takeda Pharmaceutical Co., which accounts for almost a fifth of the MSCI Japan health-care index, is up 18 percent. The Japanese drugmaker tumbled more than 40 percent in 2018.

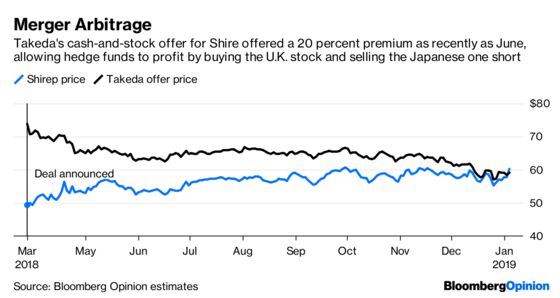

Merger arbitrage hedge funds can congratulate themselves on a big win from Takeda’s $62 billion takeover of Shire Plc. The Osaka-based company offered $30.33 in cash and 0.839 in new shares for each Shire stock. As recently as last June — more than two months after the deal was announced — Takeda’s offer was still almost 20 percent higher than the U.K. company’s market price. Arbitragers would have made good money from a long-Shire and short-Takeda trade.

Even long-only funds that liked Takeda CEO Christophe Weber’s vision had no incentive to buy the shares last year because Shire offered a cheaper way to take a stake in the Japanese drugmaker. More nimble investors who also shorted Takeda were actually doing the CEO a favor by lowering its acquisition cost, even if the share decline added to the pressure from credit downgrades and investor revolts.

Now that Shire is a done deal and the short sellers have gone home (short interest in Takeda tumbled to 1.6 percent of shares outstanding recently from 35 percent), the logic of the acquisition is starting to shine through.

Japan isn’t a good market for health care. The government of Shinzo Abe has been cutting reimbursement costs of medicine covered by health insurance to curb spending, typically by somewhere between 4 percent and 7 percent every two years. This April, when another revision is due, the cuts may reach 10 percent to 15 percent, Nikkei reported.

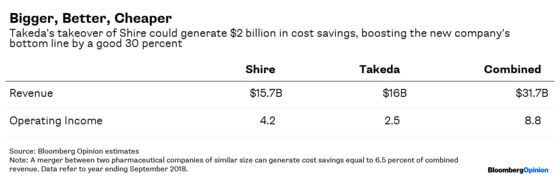

The Shire deal was a way for Takeda to get out of Japan, as my colleague Nisha Gopalan noted. The lucrative U.S. market accounts for two-thirds of Shire’s sales, compared with one-third for its Japanese acquirer. In addition, we can expect $2 billion in cost savings, well above the $1.4 billion estimated by Takeda, according to CLSA Ltd. analyst Stephen Barker. Mergers of two pharmaceutical companies of similar size typically generate cost synergies equal to 6.5 percent of combined sales.

Olympus Corp. is another household health-care name where investors see value. Its stock is up more than 30 percent this year, after the arrival of U.S.-based activist hedge fund ValueAct, which resulted in a leadership and board shakeup. If nothing else, having foreign directors could bolster the medical equipment maker’s image as it moves away from a stagnant Japanese market. The U.S. accounts for one-third of Olympus’s sales.

It wouldn’t take much to improve the company’s operations. Consider this: Olympus has an operating margin of 10.3 percent, versus 25 percent for peer Japan Lifeline Co. — even though both medical equipment makers have similar gross margins.

As recently as 2015, Japan’s health-care stocks traded at 43 times earnings; now they’re at 25 times. As the sector emerges from a sickly phase, there’s still plenty of upside.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Shuli Ren is a Bloomberg Opinion columnist covering Asian markets. She previously wrote on markets for Barron's, following a career as an investment banker, and is a CFA charterholder.

©2019 Bloomberg L.P.