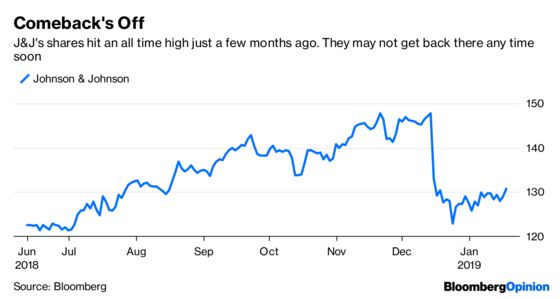

(Bloomberg Opinion) -- Investors look to Johnson & Johnson, the world’s largest health-care company, as something of a bellwether. The firm combines a huge pharmaceutical unit with consumer and medical-device businesses, so its performance gives a broad sense of the industry’s well-being. What’s the prognosis now?

On Tuesday morning, J&J announced fourth-quarter sales and profit that beat analysts’ estimates. But it also projected sales growth of just zero to 1 percent in 2019, its most sluggish rate rate since 2015.

This may attributable to issues that are specific to J&J, including generic competition for a blockbuster, and hundreds of lawsuits claiming that its talc products have caused cancer. But to the extent that the company’s relative pessimism is a sign of more widespread industry malaise, investors should brace for a rough 2019.

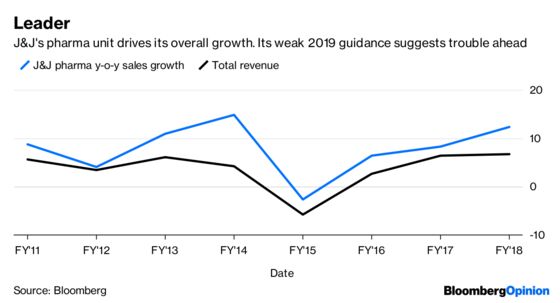

A chunk of J&J’s guidance weakness can be blamed on the strong dollar, as nearly half of its sales come from outside of the U.S. But that can’t explain everything. Another culprit is likely its pharma unit, an industry leader and the source of the vast majority of its sales growth. CEO Alex Gorsky said on Tuesday’s earnings call that the company expects a $3 billion negative sales impact from generic and biosimilar competition. Inflammation drug Remicade and prostate-cancer medicine Zytiga will likely take the biggest hits. Also, J&J executives said net prices of its medicines declined 6 percent to 8 percent last year, and that they expect prices to drop in 2019 as well.

On the bright side, J&J does have a particularly plentiful group of newer medicines. Darzalex, Erleada, and Tremfya are already on the market, depression drug esketamine may arrive. But the fact that management doesn’t believe this better-than-average group of newcomers will do more to prop up sales growth should be pretty concerning for investors.

J&J has spent years trying to turn around its consumer and device businesses, but they still don’t measure up to the pharma unit. Both businesses had sales declines in the fourth quarter relative to the same period in 2017. The year ahead may be tough as well. According to a Bloomberg Intelligence research note, competitive pressure in orthopedics may impact device sales growth in 2019.

The consumer unit may be exposed to talc litigation, which continues to be a significant liability. It’s not yet clear if negative headlines and billions of dollars in legal risk will have a direct sales impact, but the ongoing story certainly isn’t a positive for the business.

J&J’s weak guidance may also reflect broader concerns about trade tensions or a U.S. growth slowdown. Gorsky said on Tuesday’s earnings call that he expects trade to be an “issue in motion for some time.”

The firm’s guidance may be nothing more than an effort to under-promise and over-deliver, or just the result of currency headwinds. But a slowdown this dramatic for a company that’s this significant likely has more to it.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Max Nisen is a Bloomberg Opinion columnist covering biotech, pharma and health care. He previously wrote about management and corporate strategy for Quartz and Business Insider.

©2019 Bloomberg L.P.