(Bloomberg Opinion) -- Italy’s budget battles are really jacking up its cost of financing its debt.

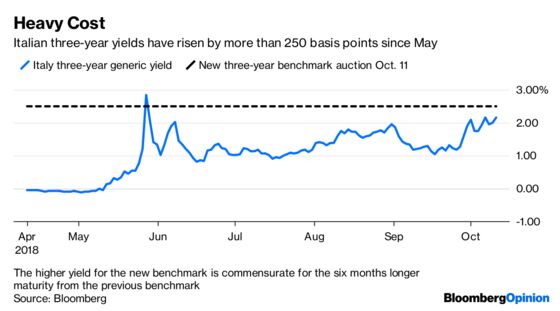

At Thursday’s bond auction, the country had to offer a yield of 2.51 percent on three-year debt. That’s twice as high as last month’s sale. Indeed, Italian three-year yields were actually negative before the populist Five Star Movement and League formed a government in May, heralding a prolonged bout of political turmoil.

But even with the giveaway pricing, the substantially higher yields are still not attracting investors in sufficient numbers. Italian yields across different maturities rose slightly after the auction results.

The Treasury in Rome is eager to raise its anticipated funding this year, with 35 billion euros ($40.5 billion) still remaining of its 245 billion euros target for bond sales in 2018. It sold the maximum amount on offer of 6.5 billion euros at Thursday’s regular bi-monthly auction. But it’s heavily skewing the sales to shorter maturities.

This reflects investor skittishness at taking a punt on Italian debt, especially over the longer term. Both Moody’s Investors Service and Fitch Ratings warned this week about the likely impact to Italy’s credit rating from the government’s fiscal plans.

Some 3.5 billion euros was sold of a new 2.3 percent October 2021 bond, a billion euros more than last month’s sale of a similar maturity. The ratio of bids received to the amount sold fell to 1.26 times from 1.67 times in September. That’s despite the fact that 12.5 billion euros of Italian bonds are due to be repaid next week, which would raise the demand for re-investment in more ordinary times.

The Italian Treasury is trying valiantly to maintain a semblance of normality in its funding. But, before long, it’s bound to run into trouble selling its debt smoothly. Italy is going to need to raise a similar level of finance in 2019, according to analysts at JP Morgan. On anyone’s terms, that’s a lot of money.

So the European Central Bank’s planned termination of new bond purchases under its Quantitative Easing program at the end of this year couldn’t come at a more difficult time for Italy. The cost of its populist experiment is becoming clearer.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2018 Bloomberg L.P.