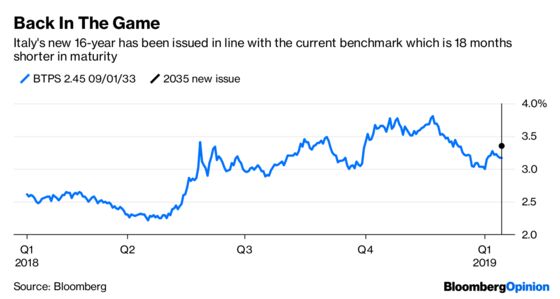

(Bloomberg Opinion) -- Italy has had the market for syndicated sovereign bonds all to itself this week, and it’s taken full advantage. Though the terms are yet to be finalized, it looks like the country has successfully raised a multi-billion euro deal for 16-year maturities at an acceptable premium of 18 basis points over its existing benchmark yield. Demand from investors exceeded 30 billion euros ($34 billion), way ahead of supply. The Prosecco will be flowing at the Treasury in Rome tonight.

With about 250 billion euros of new bonds to sell this calendar year, 80 billion euros of which are earmarked for maturities of 10 years and longer, it was vital to make a good start. Italy struggled with new issues in the second half of 2018, especially in longer-dated paper, as investors fretted over its prospects.

But with the budget battle between the populist government and Brussels resolved for now, investors have found it hard to resist the lure of a 3 percent-plus coupon. With strong demand for issues from Ireland, Portugal and Belgium last week, it’s reassuring to see there’s also interest in long-dated Italian debt.

The country isn’t out of the woods yet, though. Investors in Italian bonds still have to wrestle with whether that EU peace pact is a sign that the ruling Five Star-League coalition will now behave in a manner more befitting of lower-yielding core European debt. There’s also the question of a potential recession and the knock-on impact on Italy’s financial stability.

The chance of a rate hike this year from the European Central Bank is receding in line with the euro zone’s growth outlook. But even though that may increase the attractiveness of havens such as German bunds, it doesn't necessarily mean the same for Italy given the nature of its ruling partnership. The ECB’s halting of its QE bond-buying program is also poorly timed for Italy, which has been the heaviest user of the stimulus packages (with the weakest growth record).

Still, it would be churlish to deny Rome its moment of celebration, given the ominous signs around its long-term debt late last year. Much depends on the future policies of the League and Five Star leaders, Matteo Salvini and Luigi di Maio. But, for now at least, investors see the higher coupon as adequate reward for the risk.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Marcus Ashworth is a Bloomberg Opinion columnist covering European markets. He spent three decades in the banking industry, most recently as chief markets strategist at Haitong Securities in London.

©2019 Bloomberg L.P.